How much are refinance fees?

What is included in refinancing closing costs?

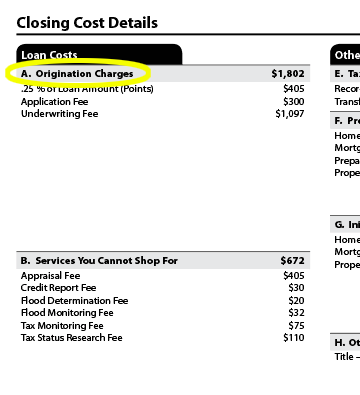

- Application and origination fees. Some lenders charge application fees of between $75 and $300. ...

- Credit report costs. Lenders will check your credit report to understand your borrowing history. ...

- Appraisal, survey, and inspection. ...

- Flood certification. ...

- Title search and title insurance. ...

- Closing costs. ...

- Early payoff. ...

- Discount points. ...

- Mortgage insurance premiums. ...

Can you deduct loan origination fees on your taxes?

While a loan origination fee is tax deductible, many other closing costs are not. These include appraisals, mortgage insurance, real estate commissions, legal fees, flood certification and the like. Aside from origination charges and loan discount fees, the only deductible items are property taxes and mortgage interest paid.

Does property tax increase when you refinance?

Refinancing won’t change your property taxes in itself, but if your tax rates are increasing anyway, your mortgage company may increase your monthly payment to cover the higher amount. Will Refinancing Affect Property Taxes?

How do I deduct loan origination fees?

- use the cash method

- have used the mortgage to purchase or build your main home

- have secured the mortgage loan with your main home

What is loan origination fee?

Technically, a loan origination fee is the fee the lender charges for loan processing. Points involve a loan discount fee. Every point, which is prepaid interest, is equal to 1 percent of the total loan.

How long can you deduct home loan fees?

Most homeowners, however, do not want to deduct these fees over 20 to 30 years if they can do it all at once.

What are deductible items for a mortgage?

Aside from origination charges and loan discount fees, the only deductible items are property taxes and mortgage interest paid.

What is the standard deduction for married filing jointly?

That means a married couple filing jointly has a standard deduction of $24,000. If your itemized deductions, including loan discount fees, are less than the standard deduction, you will likely opt not to itemize on your federal income tax form.

How many points do you have to deduct on a second home loan?

You cannot have paid more points than is usual in your area. Typically, buyers pay to two to three points on the loan, not five or six. You cannot take the deduction for points if they were paid in lieu of other fees, such as property taxes, legal fees, ...

Is loan origination fee deductible?

Loan origination fees and points are tax deductible, however, the IRS raised the standard deduction, making it more advantageous for some to take the standard rather than the itemized deduction.

Can you deduct points on HUD?

You cannot take the deduction for points if they were paid in lieu of other fees, such as property taxes, legal fees, title insurance and the like. Points charged must appear on Form HUD-1, the Uniform Settlement Statement. You can only deduct these costs if you itemize deductions on Form 1040, Schedule A.

What Are Loan Origination Fees?

A loan origination fee refers to the cost a borrower has to meet towards their application. The charges go to the lender for creating unique loan specifications. It’s also called the loan processing fee or money lending fee.

Why refinance a business loan?

Sometimes, you’ll refinance a business loan to get better terms like lower interest or longer repayment period. The approach will save you money in the long run, but won’t help in tax deductions.

What is the role of a lender in a business loan?

The lender must decide on the creditworthiness, loan amount, interest rates, and repayment terms.

What is prepaid interest?

Prepaid interest refers to upfront interest payable before the first payable installment. When you have a mortgage on the business property, you’ll have to prepay interest as part of closing costs. For taxation purposes, such interest is expensed over the loan duration.

What are the issues with a business loan?

Besides, there is also loan origination fees you must meet. All these factors, coupled with tax deductions, might make your loan very expensive in the long run.

What is business line of credit?

A business line of credit lets you draw from a pre-approved amount of available funds. You will then repay the amount you withdraw within minimum repayment guidelines. You only attract payable interest on the amount you utilize, unlike what happens with a term loan.

When does interest on a business line of credit accumulate?

Interest on a business line of credit accumulates only when you withdraw from the fund. The amount of interest deduction hence depends on your usage of the funds. Refer to your business line of credit statements before filing your tax returns.

What does it mean to settle a mortgage refinance?

You "settle" or "close" your mortgage refinancing when you sign all the paperwork to officially take out the new loan and pay off the old one. A number of fees and charges may be applied at settlement. These closing costs can add up to hundreds or thousands of dollars and may include such things as: Appraisal fees.

How much is a point on a loan?

One point equals 1% of the loan amount, so if you paid 2 points on a $100,000 loan, for example, you would have paid $2,000. Points sometimes go by other names, including: Loan origination fee. Maximum loan charge. Discount points.

What is the 1098 form for mortgage?

When you use TurboTax, it helps you decide which option—itemizing or the standard deduction—will save you more money. At year's end, your mortgage lender sends you a statement, called Form 1098, explaining how much you paid in interest during the year.

What is a home loan?

The loan is for your primary residence or a second home that you do not rent out. The loan is secured by your home. This means your home serves as collateral for the loan; if you fail to make your payments, the lender can foreclose on the home.

Can you take tax deductions when refinancing a mortgage?

When refinancing a mortgage to get a lower interest rate or obtain more favorable loan terms, you're really just taking out a new loan and using the money to pay off your existing home loan. In general, the same tax deductions are available when you're refinancing a mortgage as when you're taking out a mortgage to buy a home.

Can you deduct mortgage interest on taxes?

With any mortgage—original or refinanced—the biggest tax deduction is usually the interest you pay on the loan. Generally, mortgage interest is tax deductible, meaning you can subtract it from your income, if the following applies: The loan is for your primary residence or a second home that you do not rent out.

Can you deduct points on a mortgage?

If you paid "points" when you refinanced your mortgage, you may be able to deduct them. Points are prepaid interest; you pay them upfront to get a lower interest rate during the period when you're repaying the loan. One point equals 1% of the loan amount, so if you paid 2 points on a $100,000 loan, for example, you would have paid $2,000. Points sometimes go by other names, including:

Is Your Loan Origination Fee Tax Deductible

One of the lesser known benefits of becoming a homeowner is the tax deductions you will receive. However, knowing what homebuyer costs qualify for a tax deduction can be confusing. You undoubtedly signed a mountain of paperwork at your closing, but do you really know what you signed?

What Is A Refinance Tax Deduction

A deduction is an expense that can lessen your tax burden. You reduce the overall amount of money that you need to pay taxes on when you take a deduction. For example, if you earn $50,000 a year before taxes and you have $5,000 worth of deductions, youd only pay taxes on $45,000 of your income.

Mortgage Refinance Tax Deductions On Rental Properties

As noted earlier, you may be able to tax deduct your closing costs on rental investment properties. You also may deduct the points that you paid up front. I may save you money to get the facts on investment property and second-home refinances. Some of the closing costs that you can deduct on your investment property include:

Refinancing : Are Refinance Costs Tax Deductible

Who couldnt use some extra cash? Refinancing your home is one of several smart ways to save money. You could end up with a lower monthly payment or pay less for your home in the long run. You may even be able to deduct some of your refinance expenses.

You May Be Able To Deduct Points

The one closing cost that you may be able to deduct is the points you pay. You may pay origination points or discount points. Origination points are usually closing costs in disguise. They are a way for the lender to make more money or to get away with certain fees that otherwise wouldnt be allowed if they were itemized.

Will You Take The Standard Deduction

Heres the biggest problem. Any of the above write-offs are legitimate, but only if you itemize your tax deductions. Up until 2018, itemizing was the common way to get write-offs, as many homeowners had many more deductions than the standard deduction allowed.

How Much Should I Pay In Closing Costs For A Home Refinance

With all of these different fees, you may wonder, how much are closing costs on a refinance? Your costs for refinancing depend on your outstanding principal on your current mortgage. You can expect to pay 2% to 5% of your outstanding principal for your closing costs.

Do you have to amortize origination fees on a refinance?

On a refinance, you may need to amortize an origina tion fee (if paid) over the life of the loan. TurboTax will walk you through this process.

Is mortgage insurance deductible for refinancing?

For a refinance, mortgage interest paid (including origination fee or "points"), real estate taxes, and private mortgage insurance (subject to limits) are the only deductible fees. Other costs are added to your basis in the property.

What do you use your loan for?

You use your loan to buy or build your main home.

What is a point on a mortgage?

The term points is used to describe certain charges paid to obtain a home mortgage. Points may also be called loan origination fees, maximum loan charges, loan discount, or discount points. Points are prepaid interest and may be deductible as home mortgage interest, if you itemize deductions on Schedule A (Form 1040), Itemized Deductions.

Can you deduct points paid by a buyer on a second home loan?

The buyer may deduct points paid by the seller, provided the buyer subtracts the amount from the basis or cost of the residence. You can only deduct points you pay on loans secured by your second home over the life of the loan.

Can you deduct points on a home loan?

You can also fully deduct (in the year paid) points paid on a loan to improve your main home if you meet tests one through six above.

Can you borrow money from a lender before closing?

The funds you provided at or before closing, including any points the seller paid, were at least as much as the points charged. You can't have borrowed the funds from your lender or mortgage broker in order to pay the points. You use your loan to buy or build your main home.

Can you deduct all of the points paid on a mortgage?

If you can deduct all of the interest on your mortgage, you may be able to deduct all of the points paid on the mortgage . If your home acquisition debt exceeds the limit for your filing status, you won’t be able to deduct all of the mortgage interest and points.