What happens if you pay off a personal loan early?

What are the pros of paying off a personal loan early?

- You might save money on interest The sooner you pay off your loan, the less you’ll have to pay in total interest. ...

- It can lower your debt-to-income ratio Early loan payments can affect your credit score in a variety of ways. ...

- You’ll have fewer monthly payments Paying off your loan early gives you one less monthly payment to worry about. ...

Are there any penalties for paying my loan off early?

You may be charged a certain percentage of your remaining balance if you pay your loan off early. The longer you’ve had the loan, the lower the penalty will be. This type of penalty is not legal in every state or for every loan, and it must be disclosed in the loan documents.

Do you save money if you pay off loans early?

The most obvious reason you might want to consider paying off a loan early is that it saves you money on the amount of interest you pay. It’s important to note that this only applies if you are paying a simple and not precomputed interest rate.

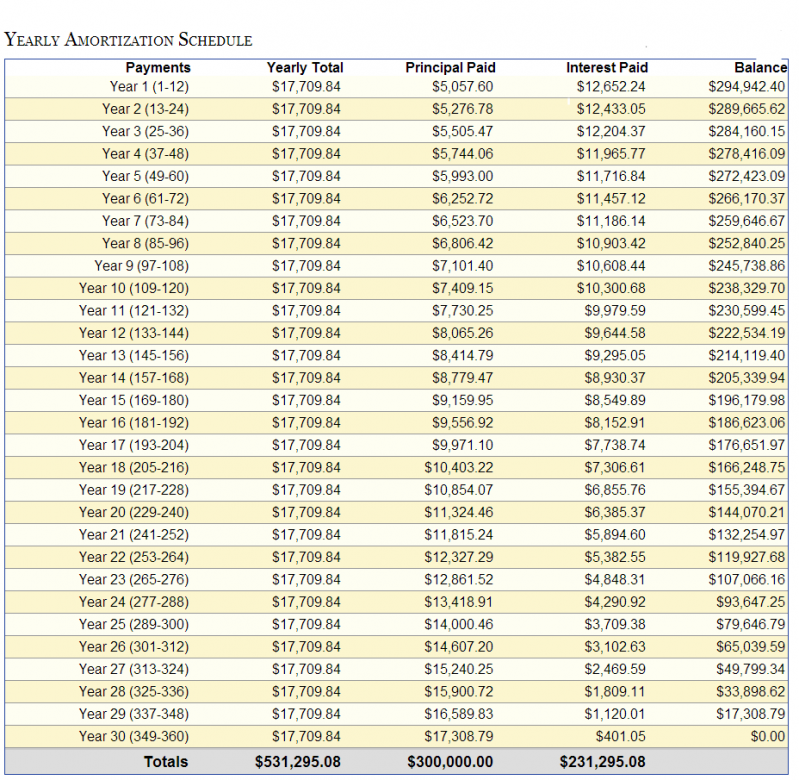

How do you calculate early mortgage payoff?

Early Mortgage Payoff Calculator The following calculator makes it easy for homeowners to see how quickly they will pay off their house by making additional monthly payments on their loan. Simply enter the original loan term, how many years you have remaining on the loan, the original mortgage amount, the interest rate charged on the loan & the ...

Is paying off a loan early worth it?

The biggest advantage of speeding up loan payoff is that it can save you money. "In many cases, paying off a personal loan early will save the borrower money in interest," says Thomas Nitzsche, financial educator at Money Management International, a nonprofit credit counseling agency.

Can you pay a loan off early and avoid interest?

Yes. By paying off your personal loans early you're bringing an end to monthly payments, which means no more interest charges. Less interest equals more money saved.

What happens when I pay off my loan early?

Paying off the loan early can put you in a situation where you must pay a prepayment penalty, potentially undoing any money you'd save on interest, and it can also impact your credit history.

Can you get penalized for paying off a loan early?

What Is A Prepayment Penalty? A mortgage prepayment penalty is a fee that some lenders charge when you pay all or part of your mortgage loan off early. The penalty fee is an incentive for borrowers to pay back their principal slowly over a longer term, allowing mortgage lenders to collect interest.

Can paying off a loan early hurt credit?

Personal loans sometimes come with prepayment penalties. And while paying off a personal loan ahead of schedule certainly won't ruin your credit, it can set your credit back a tick if you're working on building a credit history.

What is the fastest way to pay off a high interest loan?

How to Pay Off Debt FasterPay more than the minimum. ... Pay more than once a month. ... Pay off your most expensive loan first. ... Consider the snowball method of paying off debt. ... Keep track of bills and pay them in less time. ... Shorten the length of your loan. ... Consolidate multiple debts.

Can you pay off a 72 month car loan early?

Some lenders charge a penalty for paying off a car loan early. The lender makes money from the interest you pay on your loan each month. Repaying a loan early usually means you won't pay any more interest, but there could be an early prepayment fee.

What is a good credit score?

670 to 739Although ranges vary depending on the credit scoring model, generally credit scores from 580 to 669 are considered fair; 670 to 739 are considered good; 740 to 799 are considered very good; and 800 and up are considered excellent.

Why does your credit score drop when you pay off a car loan?

If the loan you paid off was your only installment account, you might lose some points because you no longer have a mix of different types of open accounts. It was your only account with a low balance: The balances on your open accounts can also impact your credit scores.

What does no penalty for early payoff mean?

You can partially or fully prepay your loan at any time with absolutely no prepayment penalty or fee. Any payments made in addition to your contractual monthly payment will be applied towards a reduction in the principal balance of your loan.

How much will my credit score increase if I pay off my car?

Once you pay off a car loan, you may actually see a small drop in your credit score. However, it's normally temporary if your credit history is in decent shape – it bounces back eventually. The reason your credit score takes a temporary hit in points is that you ended an active credit account.

How can I avoid paying interest on a loan?

Pay your monthly statement in full and on time: Paying the full amount will help you avoid any interest charges. If you can't pay your statement balance off completely, try to make a smaller payment (not less than the minimum payment).

Is it better to pay off a loan in full or make payments?

The end goal is the same: to pay off as much as you can as quickly as possible. Although making timely payments is always a good idea, you don't want to overlook the benefits of paying off bigger chunks of debt — or all of your debt in full — to improve your credit score.

Do you save interest by paying off a car loan early?

Save money The most obvious reason you might want to consider paying off a loan early is that it saves you money on the amount of interest you pay. It's important to note that this only applies if you are paying a simple and not precomputed interest rate.

What is a good interest rate on a personal loan?

What is considered a good interest rate on a personal loan? A good interest rate on a personal loan can be different for everyone. Considering that the average borrower qualifies for average loan interest rates between 10 percent and 28 percent, any rate below that threshold should be considered “good.”

How to find out if you have to pay off a loan early?

Checking your credit agreement is the best way to find out whether you will have to pay a fee for paying off your loan early, either before or after you have taken out a loan. The agreement sets out the terms for the borrower and lender to abide by. It should detail what happens if you decide to pay off your loan early.

How long do you have to pay back a loan?

Of course, you will have to repay all the money you have been loaned within 30 days, and the lender is legally allowed to charge you interest until they receive the loan back.

How do I know which lenders charge a fee?

This is due to some lenders counting the ability to charge for additional interest as an ERC and therefore not advertising that they will charge you when you pay off a loan early.

How much could I save with early repayment?

The amount you can save from paying back your loan early will depend upon the size of your original loan, the interest rate on the loan, and the length of time left on the loan term.

What is it called when you only pay part of your loan?

If you only wish to make early repayment for part of your loan this is known as overpayment . Overpayments allow you to make your monthly repayments cheaper by lowering the amount of interest you’ll have to pay on the amount you owe. If you wish to make an overpayment , then you should follow these steps:

How to get an early settlement on a mortgage?

Contact your lender – get in touch with your lender and request an ‘early settlement amount’ for your loan.

How many days can you add to your mortgage?

If you have more than 12 months left on your repayment plan, lenders can add an extra 30 days (or one calendar month).

What happens if you pay off a loan early?

Depending on the dollar amount of any penalties, the savings in accrued interest may not be beneficial in the end. Sometimes these loans can have very steep early payoff penalties added on. You have to read the fine print or contact the lender and ask them specifically about any penalties or added fees if you were to pay off the loan now instead of waiting.

Is it easy to pay off debt early?

Paying off a debt early may appear to be an easy decision to make. After all, avoiding additional accrual of interest would seem to save money in the long run. However, there are a number of factors that should be taken into consideration before requesting a payoff quote from a lender. We’re going to take a closer look at what it takes to pay ...

Is student loan interest deductible?

Some loans, such as federal student loans and mortgages, have tax advantages that would be lost if they were to be paid off early. The interest paid on these loans may be tax deductible and the borrower should talk to their tax advisor about what the tax implications would be before paying off these types of loans.

Is it better to pay off a loan early?

Although there are many benefits to paying off a loan early, there are potential drawbacks as well. Say you have a lump sum that you would like to use to eliminate a loan that is hanging over your head. Yes, if you pay it off, the loan will be gone – but so will all of the cash you put towards eliminating it. Once that money is gone, you cannot get it back, no matter how badly you may need it. And in today’s unstable economy, it is wise to have money set aside as an emergency fund in the event of an unexpected event such as illness or job loss. It is important to remember that in the unfortunate event you do become unemployed; you will not have the income necessary to qualify for a loan no matter how badly you may need it. It becomes a vicious cycle: it becomes harder to get cash when you end up needing it the most.

Does interest accrue on auto loans?

By paying off the loan in its entirety, or even by increasing your monthly payments, that interest will no longer accrue.

Does paying off a car loan early improve your credit score?

However, sometimes paying off an auto loan early won’t save you anything. ...

Personal Loan Prepayment Penalty

If you take out a $6,000 personal loan to turn your guest room into a pet portrait studio and agree to pay your lender back $125 per month for five years, the term of that loan is five years. Although your loan term says it cant take you more than five years to pay it off, some lenders also require that you dont pay it off in less than five years.

Can You Pay Off A Personal Loan Early

If you have enough money to make an extra payment or two, then you may be able to pay off a personal loan earlier than planned.

Can You Pay Off A Loan Early

Say you took out a $5,000 personal loan three years ago. Youve been paying it off for three years, and you have two more years before the loan term ends. Recently you received a financial windfall and you want to use that money to pay off your personal loan early.

How Long Do I Have To Pay Off My Loan

Many people start paying down personal loans early so they can avoid paying additional interest later on. While this is a sound strategy, its important to consider factors such as your loan period and payment amount before making any final decisions.

When Is It The Right Choice To Pay Off A Loan Early

There are many situations in which paying off your loan early can be beneficial, such as the following:

Can I Pay Off My Personal Loan Early

Can I pay off my personal loan early?Personal loans can be a practical and efficient way to achieve a goal.

Should You Consolidate Your Debts

Some loans are specifically advertised as debt consolidation loans these allow you to merge several credit commitments into one.

How to pay off a loan early?

If you want to pay off a loan early, under the Consumer Credit Act you should get a refund of any interest and charges you’ve already paid. Just write to your lender and ask them for an ‘Early Settlement Amount’ for your loan – this should be any fees minus any reimbursements you’re owed.

Why pay off a loan faster than required?

Whether it’s a personal loan, home loan, cash loan, car loan, student loan or mortgage, if you pay off your debt faster than required, you’ll benefit from lower total interest charges and, obviously, spend less time in debt.

What is early repayment?

Early repayment (or resettlement) is where you clear your debt before you’re legally obliged to. Many banks and lenders charge penalties for repaying loans early. There’s no standard figure, but the average is approximately the equivalent of 1-2 months’ interest.

Do you have to pay off a loan at once?

You don’t have to pay the full amount of your loan off at once – you could always opt for a partial repayment option. In this instance, you may be able to negotiate with your lender to decrease your monthly instalments.

Do all loans penalise early repayment?

Not all loans penalise for early repayment, and it’s a good idea to explore the market and compare the deals on offer. Always weigh up the repayment fees to establish which course of action will save you the most money.

Is early repayment penalty the same as redemption fee?

Different lenders often don’t speak the same lingo, so don’t be confused if you see phrases like early repayment charge, early repayment penalty, early redemption fee, redemption charge or financial penalty – they’re all the same thing.

How long do you have to pay off a 401(k) loan?

The IRS requires that borrowers must pay off the 401 (k) loan within five years from the time they took the loan. The loan should be repaid in “substantially equal payments” spread over the term of the loan.

When is 401(k) loan due?

With the enactment of the new law, 401 (k) participants have until the tax due date for the year when the distribution is made to repay the outstanding 401 (k) loan. For example, if you left your job in January 2021, you will have until April 15, 2022, to fully repay the loan. Once you have settled the outstanding 401 (k) balance, you will not be required to pay tax or penalty on the distribution.

Is a 401(k) loan taxable?

Unless you come up with a sufficient amount and put it back into the qualifying 401 (k) account within the required period, the distribution will be taxable. This means that the participant will be taxed as if the outstanding loan were a cash distribution or withdrawal. The employer will issue you with IRS Form 1099-R, and a copy of this form will be sent to the IRS. If you are under 59 ½ when you leave your job, you will also pay a 10% early withdrawal penalty over and above the income taxes.

Can you borrow from a 401(k) if you owe taxes?

If a 401 (k) loan is at risk of being reported as a withdrawal, you can opt to borrow from another source to avoid tax liability. Depending on how much you owe, borrowing a loan could make sense if the potential tax liability is higher than the interest you would pay on the new loan.

Can you pay off a 401(k) early?

401 (k) s do not charge early repayment penalties to participants who pay off the loan early. The loan statement will show the additional credits to the loan account, and the remaining 401 (k) loan principal balance.

Can you defer 401(k) loan payments for 5 years?

An exemption to the 5 years rule is if you took a coronavirus-related loan under the CARES Act. The new act allowed 401 (k) participants an extra year to repay the loan subject to the approval of the plan administrator. The act allows borrowers to defer loan payments for an extra year after the lapse of the regular 5-year period. However, the interest on the loan still accrues in the extra year.

Do people graduate college with debt?

Many people graduate college with debt and struggle to keep up with their student loan payments once they have a degree in hand.

Does a high student loan balance hurt your credit score?

Provided you make your monthly payments on time, a high student loan balance won't actually hurt your credit. On the contrary -- those timely payments will be factored into your payment history, thereby bringing up your credit score.