What are the three financial statements required by GAAP?

Why is a cash flow statement important in GAAP?

Why was GAAP created?

When did GAAP start?

What is cash flow statement?

See 2 more

About this website

Are comparative financial statements required under GAAP?

Comparative financial statements are not required; however, SEC requirements specify that most registrants provide two years of comparatives for all statements except for the balance sheet, which requires only one comparative year.

Which financial statements are required by GAAP?

The following three major financial statements are required under GAAP: The income statement. The balance sheet. The cash flow statement.

How many years of comparative financial statements are required under current GAAP?

3 years of previous GAAP annual financial statements, and previous GAAP interim statements for the current and comparable prior period, all with reconciliation to U.S. GAAP; 2 years of IFRS annual financial statements and IFRS interim statements for the current and comparable prior period; or.

Are comparative financial statements required by IFRS?

It requires an entity to present a complete set of financial statements at least annually, with comparative amounts for the preceding year (including comparative amounts in the notes).

What are the 4 principles of GAAP?

Four Constraints The four basic constraints associated with GAAP include objectivity, materiality, consistency and prudence.

How is US GAAP different from IFRS?

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. This disconnect manifests itself in specific details and interpretations. Basically, IFRS guidelines provide much less overall detail than GAAP.

Does GAAP require consolidated financial statements?

Consolidation Rules Under GAAP The general rule requires consolidation of financial statements when one company's ownership interest in a business provides it with a majority of the voting power -- meaning it controls more than 50 percent of the voting shares.

What is a GAAP checklist?

The International GAAP® checklist: Shows the disclosures required by the standards. Includes the IASB's encouraged and suggested disclosure requirements under IFRS. Summarizes relevant IFRS guidance regarding the scope and interpretation of certain disclosure requirements.

What ratio is required by GAAP?

Financial Ratios (a) The Company shall at all times maintain, on a consolidated basis, a Total Debt to Capitalization Ratio of not more than 0.65 to 1.00.

Does US GAAP have OCI?

Like IFRS Standards, US GAAP makes no distinction between ordinary and extraordinary activities. The presentation, disclosure or characterisation of items of income and expense as 'extraordinary items' in the statement of profit or loss and OCI or in the notes to the financial statements is prohibited.

Why are GAAP generally accepted?

GAAP aims to improve the clarity, consistency, and comparability of the communication of financial information. GAAP helps govern the world of accounting according to general rules and guidelines. It attempts to standardize and regulate the definitions, assumptions, and methods used in accounting across all industries.

Which financial statement are prepared under IFRS?

Financial statements under IFRSNormal nameUnder IAS-1Balance SheetStatement of Financial Position (SOFP)Profit & Loss AccountStatement of Comprehensive income (SOCI) Statement of Changes in equity (SOCIE)Cash flow statementStatement of Cash flows (SOCF)NotesOct 3, 2015

Does GAAP require consolidated financial statements?

Consolidation Rules Under GAAP The general rule requires consolidation of financial statements when one company's ownership interest in a business provides it with a majority of the voting power -- meaning it controls more than 50 percent of the voting shares.

What is a GAAP checklist?

The International GAAP® checklist: Shows the disclosures required by the standards. Includes the IASB's encouraged and suggested disclosure requirements under IFRS. Summarizes relevant IFRS guidance regarding the scope and interpretation of certain disclosure requirements.

What are the three parts of the GAAP financial accounting framework?

As a result, many private companies adhere to it.Three components of GAAP. ... Principle of Regularity. ... Principle of Consistency. ... Principle of Sincerity. ... Principle of Permanence of Methods. ... Principle of Non-Compensation. ... Principle of Prudence. ... Principle of Continuity.More items...

Why must accounting reports be prepared according to specific procedures GAAP?

This is because GAAP ensures consistency in reporting in all businesses, making the financial reports that are produced complete and comparable. This is especially important in publicly traded companies or in companies required to publicly release their financial statements.

What Are the Required Financial Statements Under GAAP & IFRS?

It does not matter if you are running a small, medium company or a large corporation, or organization, whether profitable or not for profit, you are required to prepare the financial statements to record all of the financial-related transactions that occur daily in your organization to accounting system so that you could establish the financial statements.

Financial Reporting Requirements - What is it? Definition, Examples and ...

Financial Reporting Requirements Definition. There are two types of financial reporting requirements: legal and regulatory. These relate to the provisions of legislation and those regulations produced by standard-setters (Lee, 2007).

US GAAP financial statements: Balance sheet and P&L ... - ReadyRatios

US GAAP financial reports: all assets, liabilities and equity (official taxonomy 2013-2022) Balance sheet (Statement of financial position)

GAAP Reporting Requirements - Office of the Washington State Auditor

3.1.1.10 The following principles of accounting and financial reporting are based on those set forth in the Governmental Accounting Standards Board’s (GASB) Codification of Governmental Accounting and Financial Reporting Standards.The BARS manual permits accounting and financial reporting that conforms to these principles in all respects and requires GAAP municipalities to account and report ...

Chapter 5: Financial Reporting Requirements and Accounting ... - Treasury

Institutional framework Australia has a differential disclosure regime under which financial reporting requirements are set according to the type of entity, principally on the basis of the level of public interest in the entity. The types of entities can be classified as:

What is GAAP financial statement?

Generally Accepted Accounting Principles or GAAP are basically the set of ten accounting standards set by the United States Financial Accounting Standards Board (FASB ). First established by FASB in 1973, the GAAP principles are now accepted by the Securities Exchange Commission (SEC) ...

What are the most important financial statements in GAAP?

To report these things, the most important GAAP financial statements are – Balance Sheet, Income Statement, Shareholder’s Equity, and Cash Flow Statement. Balance Sheet talks about assets and liabilities ...

What is the difference between a balance sheet and a cash flow statement?

Balance Sheet talks about assets and liabilities of the company, while the Shareholder’s Equity detail the available equity in the company. The income statement details the revenue earned by the company and the corresponding expenses. The Cash Flow statement, as the name suggests, is simply the cash record of the company. Cash flow becomes important because both the income statement and balance sheet reveal the financial health of the company on the accrual basis, and therefore, do not talk about the real financial position.

Why is cash flow important?

Cash flow becomes important because both the income statement and balance sheet reveal the financial health of the company on the accrual basis, and therefore, do not talk about the real financial position. Let’s understand each of the GAAP financial statements ...

Why is GAAP important?

GAAP is helpful in creating consistency because all the financial statements follow the same set of principles. Businesses that follow and maintain their financial statements as per GAAP have an upper hand as they offer the best information to run business.

What is stockholder equity statement?

This statement shows the changes in the equity (in the balance sheet) during an accounting period. Or, we can say, it reports the events that lead to an increase or decrease in the owner’s equity over a given period. Stockholders’ Equity statement in a corporation consists of:

Why is cash important in a company?

Cash is essential to keep the business running and meet the day-to-day expenses of the company. Therefore, understanding the sources of cash in a company becomes very crucial. For a given period, the cash flow statement should include the following information: Source of Cash. Uses of Cash.

What are the 4 types of financial statements?

Under US GAAP or IFRS accounting standard, your organization needs to prepare 4 types of financial statements including income statement, balance sheet, statement of changes in equity, statement of cash flow with the noted to financial statements.

Why do organizations need financial statements?

These statements provide all the organization’s financial transactions and give full information about the performance of the company during the financial period so that all of the stakeholders could use that information to help them make the right decision.

What is a cash base statement?

A cash base statement which shows the changes in the balance sheet and Income statement that affect cash & cash equivalents. Or the statement which shows the total cash inflow and outflow of an Organization is termed as cash flow statement.

What is the statement that shows the total cash inflow and outflow of an organization?

Or the statement which shows the total cash inflow and outflow of an Organization is termed as cash flow statement.

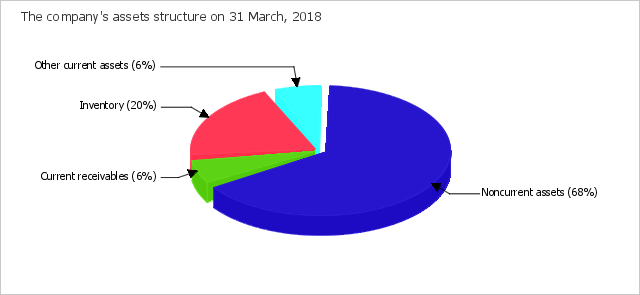

How many parts are there in the asset side of the balance sheet?

If you analyze the asset side of the balance sheet you will see that it is divided into two parts. In the non-current section, we add all those items which are capital in nature and have a useful life of more than one year while the current assets have a useful life of less than one year.

Which side of the balance sheet is the same logic?

The same logic is applied to the liabilities side of the balance sheet.

Who is the important stakeholders who use the company's financial information?

Employees and management are of the company is also the important stakeholders who use the company’s financial information.

How many years of comparatives are required for financial statements?

One year of comparatives is required for all numerical information in the financial statements, with limited exceptions in disclosures.

What is IFRS in accounting?

IFRS specifies the periods for which comparative financial information is required, which differs from both US GAAP and SEC requirements.

How many years of comparatives are required for financial statements?

One year of comparatives is required for all numerical information in the financial statements, with limited exceptions in disclosures. In limited note disclosures and the statement of equity, more than one year of comparative information is required.

What are the similarities between IFRS and GAAP?

Under both sets of standards, the components of a complete set of financial statements include: a statement of financial position, a statement of profit and loss (i.e., income statement) and a statement of comprehensive income (either a single continuous statement or two consecutive statements), a statement of cash flows and accompanying notes to the financial statements.

How does IFRS differ from GAAp?

IFRS differs significantly from US GAAp mainly because IFRS are used in over 140 countries all over the world and the more principle based nature of IFRS: IFRS uses functional currency and presentation currency, based on the context of a business (national or international).

What is a general accepted accounting principle?

Generally accepted accounting principles are a set of thousands of U.S. GAAP pronouncements (accounting standards and guidelines) created and maintained by the U.S. Financial Accounting Standards Board (FASB). In 2008 the FASB issued the FASB Accounting Standards Codification which reorganized these U.S. GAAP pronouncements into roughly 90 accounting topics

What is accrual basis accounting?

In accrual accounting, revenue and expenses are reported in the period in which a sale is made or an expense is incurred regardless of when money is received or the expense is paid.

When did GAAP start?

Since the FASB established GAAP guidelines in 1973, the U.S. Securities and Exchange Commission and the American Institute of Certified Public Accountants have adopted GAAP as official standards of financial accounting.

Is there a requirement for GAAP to be presented?

There is no general requirements within US GAAP address the presentation of specific performance measures. SEC regulations define certain key measures and require the presentation of certain headings and subtotals.

When was IFRS 6120.5 incorporated into GAAP?

6120.5 With respect to Canadian registrants, IFRS has been incorporated into Canadian GAAP for publicly accountable enterprises for fiscal years beginning on or after January 1, 2011. (Last updated: 10/30/2020)

When are financial statements required for S-X 3 05?

Financial statements of acquired and to be acquired foreign businesses required under S-X 3-05 must comply with the age of financial statement requirements at the time the registration statement is declared effective. For a calendar year-end entity, this means that if a registration statement were to become effective prior to October 1, 20XX, financial statements for any interim period would not be required under S-X 3-05 for a foreign business.

How long does a foreign company have to have a registration statement?

Under the rule, a registration statement of a foreign private issuer may become effective with audited financial statements as old as 15 months, with the most recent interim statements as old as nine months. If interim statements are required, they must cover a period of at least six months.

How long do foreign companies have to file financial statements?

6220.1 Financial statements of a foreign private issuer must be as of a date within nine months of the effective date of a registration statement. Audited financial statements for the most recently completed fiscal year must be included in registration statements declared effective three months or more after fiscal year-end. Under the rule, a registration statement of a foreign private issuer may become effective with audited financial statements as old as 15 months, with the most recent interim statements as old as nine months. If interim statements are required, they must cover a period of at least six months.

How long can a company use a combination of annual and interim periods?

Registrants are permitted to use combinations of periods that involve overlaps or gaps in the information of the target company of up to 93 days, provided that the resulting annual and interim periods are of the same length required for the registrant, and there are no overlaps or gaps in the registrant’s information.

Do foreign companies have to file the same forms as domestic companies?

Answer: Yes. However, if it elects to do so, it must comply with all of the requirements of the “domestic company” forms. 6120.2 A foreign issuer - other than a foreign government - that does not meet the definition of a foreign private issuer must use the same registration and reporting forms as a domestic registrant.

Do foreign companies have to file S-K 402?

6120.10 Foreign private issuers that file on Form 20-F and foreign private issuers who voluntarily file on Form 10-K are not subject to executive compensation disclosures required by S-K 402, and may, instead, follow Form 20-F executive compensation disclosures. However, a foreign-domiciled registrant that does not meet the foreign private issuer definition must file on 10-K and is required to comply with S-K 402.

What are the three financial statements required by GAAP?

The following three major financial statements are required under GAAP: the income statement, the balance sheet, and the cash flow statement. 1 . A company's balance sheet summarizes assets and sets them equal to liabilities and shareholder's equity. These three categories highlight what a company owns and how it finances its operations.

Why is a cash flow statement important in GAAP?

The cash flow statement is crucial because the income statement and balance sheet are constructed using the accrual basis of accounting, which largely ignores real cash flow.

Why was GAAP created?

GAAP was ultimately created in response to the Stock Market Crash of 1929 and the subsequent Great Depression. 3 Many economists believe that these historical events were at least partially the result of questionable reporting practices by some publicly-traded companies. After the federal government started consulting with accounting groups to develop standards and practices for accurate and consistent financial reporting mechanisms GAAP began emerging with legislative measures like the Securities Act of 1933 and the Securities Exchange Act of 1934. 2

When did GAAP start?

After the federal government started consulting with accounting groups to develop standards and practices for accurate and consistent financial reporting mechanisms GAAP began emerging with legislative measures like the Securities Act of 1933 and the Securities Exchange Act of 1934. 2.

What is cash flow statement?

The cash flow statement. 1. The income statement recaps the revenue earned by a company during the reporting period, along with any corresponding expenses. This includes revenue from operating and non-operating activities, allowing auditors, market analysts, investors, lenders, regulators, and any other stakeholders, ...

Reporting Requirements Under GAAP

GAAP Financial Statements

- Balance Sheet

The balance sheetprimarily consists of Assets and Liabilities. Assets include both current and non-current assets, and so are the liabilities. All the assets that a company can easily convert into cash are known as current assets. On the other hand, the assets that can’t be converted into cas… - Statement of Owner’s Equity

This statement shows the changes in the equity (in the balance sheet) during an accounting period. Or, we can say it reports the events that lead to an increase or decrease in the owner’s equity over a given period. Stockholders’ Equity statementin a corporation consists of: Common …

Guidelines For GAAP Financial Statements

- All financial statements under GAAP are affected by three basic assumptions. These are the monetary unit for financial reporting, “going concern” assumption, and reporting period options. All the financial statements must display data in a common currency, such as the US dollar. If, for any reason, a transaction does not have a monetary unit, an accountant must not include it in th…

Benefits of Using GAAP Financial Statements

- GAAP helps create consistency because all financial statements follow the same set of principles. Businesses that follow and maintain their financial statements as per GAAP have the upper hand as they offer the best information to run a business. Also, since all the organizations, financial institutions, banks, and authorities accept GAAP principles, it becomes easier for the companie…