How should inherent risks be measured?

It can be measured by two factors – impact and likelihood. Inherent impact measures the impact of an event on a company or organization when it occurs as there are no mitigation actions. Inherent likelihood measures the possibility for an event to take place in the absence of risk control.

What are inherent risks examples?

Non-routine accounts or transactions can present some inherent risk. For example, accounting for fire damage or acquiring another company is uncommon enough that auditors run the risk of focusing too much or too little on the unique event.

What is meant by inherent risks?

Inherent risk is the amount of risk that exists when some threat goes untreated or unaddressed. This also means that the less an organization tries to manage risk, the more inherent risk it has.

What is inherent risk in an audit?

Inherent risk, which refers to the susceptibility of an assertion to a misstatement, due to error or fraud, that could be material, individually or in combination with other misstatements, before consideration of any related controls.

What factors affect inherent risk?

What Factors Can Increase Inherent Risk? Factors that can increase inherent risk include subjective estimates, non-routine transactions, and the use of complex financial instruments. Generally, the more complicated a company's business model and transactions are, the higher the inherent risk is.

What are the 9 inherent risk factors?

Inherent Risk FactorsSusceptibility to theft or fraudulent reporting.Complex accounting or calculations.Accounting personnel's knowledge and experience.Need for judgment.Difficulty in creating disclosures.Size and volume of accounts balance or transactions.Susceptibility to obsolescence.Prior year period adjustments.

What are some example of inherent?

existing as a natural or basic part of something: There are dangers/risks inherent in almost every sport. I have an inherent distrust of lawyers.

How do you mitigate inherent risks?

Transactions between related entities could also increase the level of inherent risk. That's because there's a chance that the value of the asset involved in any financial deal between the related parties might be overstated or understated. A company can mitigate inherent risk by implementing internal controls.

What is inherent risk questionnaire?

Inherent Risk Questionnaire (IRQ) is a questionnaire designed to support the HITRUST Risk Triage Model that is part of the HITRUST Third Party Risk Management Program.

What are the 3 types of audit risk?

There are three primary types of audit risks, namely inherent risks, detection risks, and control risks.

Why is inherent risk important?

Why is Inherent Risk Important? Understanding inherent risk and inherent impact is important because it helps security teams understand the current level of risk and the set of controls required to successfully address all risk factors.

What are the 5 audit assertions?

There are generally five accounting assertions that the preparers of financial statements make. They are accuracy and valuation, existence, completeness, rights and obligations, and presentation and disclosure.

What are the 3 types of audit risk?

There are three primary types of audit risks, namely inherent risks, detection risks, and control risks.

Why is inherent risk important?

Why is Inherent Risk Important? Understanding inherent risk and inherent impact is important because it helps security teams understand the current level of risk and the set of controls required to successfully address all risk factors.

What is the difference between inherent risk control risk and detection risk?

Inherent and control risk are the risks of material misstatement arising in the financial statements. These types of audit risk are dependent on the business, transactions and internal control system that the client has in place. On the other hand, detection risk is the risk that is dependent entirely on the auditors.

What is an example of residual risk?

An example of residual risk is given by the use of automotive seat-belts. Installation and use of seat-belts reduces the overall severity and probability of injury in an automotive accident; however, probability of injury remains when in use, that is, a remainder of residual risk.

How to calculate inherent risk?

The calculation of inherent risk can be bifurcated under various broad qualitative parameters. Another method to determine the IR may involve in bifurcating the activities happening in the organization into low risk, moderate and high risk, with each risk having some threshold number and then multiplying the risk levels together to arrive at the IR score. The IR is always inversely proportional to the detection risk. Hence methods should be developed that computes detection risk.

What is inherent risk?

Inherent risk is defined as the variant of enterprise-level risk wherein the probability of loss is derived from the organization’s type and complexity without any potential modifications to the prevalent environment. It is basically one of the major components of audit risk. The audit risk comprises of inherent risk, detection risk, and control risk.

What is the risk of material misstatements?

The risk of material misstatements corresponds to the risks beared by the unaudited financial statements. To curb the material misstatements, audits of the financials become absolutely critical.

What is the risk of management that is not proactive?

The management that is fairly ignorant towards their subordinates and daily activities can give rise to the levels of inherent risk. If not being proactive, the management can always miss out on material misstatements arising out in the general nature of the business, which in turn gives rise to IR.

What is control risk?

Control risk is defined as the risk which tends to surface when the internal controls in place have failed, and the financial statements have missed highlighting the failures of internal controls. The audit risk corresponds to the risk that arises when there is material misstatements on the financial statements, whereas audit opinions present a fair picture. The detection risk corresponds to the risk where the auditor displays an inability to catch material misstatements.

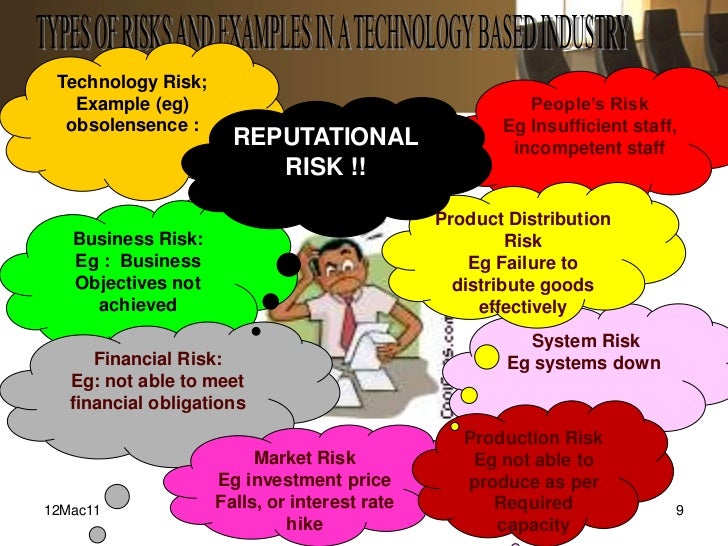

What are some examples of inherent risk?

A very broad example of inherent risk can be illustrated by highlighting the nature of the technology business. The technology business operates under a dynamic and everchanging environment. The lifecycles of products developed by them always remain short.

What is audit risk?

It is basically one of the major components of audit risk. The audit risk comprises of inherent risk, detection risk, and control risk.

What is inherent risk?

What is inherent risk? The susceptibility of an assertion about a class of transaction, account balance, or disclosure to a misstatement that could be material, either individually or when aggregated with other misstatements, before consideration of any related controls.

What is an example of a low inherent risk?

An example of a low inherent risk is the existence assertion for payables. If experienced payables personnel accrue payables, then the existence assertion might be assessed at low. (The directional risk of payables is an understatement, not an overstatement.) The lower risk assessment for existence allows the auditor to perform little if any procedures in relation to this assertion.

Why is a material misstatement a risky or complex transaction?

A material misstatement may develop within the company because the transaction is risky or complex. Then, controls may not be sufficient to detect and correct the misstatement. If the auditor fails to detect the material misstatement, audit failure occurs.

What is the only factor that can lower your risk of material misstatement?

If control risk is high, then inherent risk is the only factor that can lower your risk of material misstatement. For example, a high control risk and a low inherent risk results in a moderate risk of material misstatement. Why is this important? Lower RMMs provide the basis for less substantive work.

What are the inherent risk factors in the draft?

See paragraph .12 for the definition. Inherent risk factors include uncertainty, change, and fraud risk (and more). The draft also introduces the concept of a spectrum of inherent risk which is the degree that inherent risk varies.

Is completeness assertion for accounts payable a risk?

Conversely, the completeness assertion for accounts payable is commonly a high inherent risk. Businesses can inflate their profits by accruing fewer payables. Fraudulent reporting of period-end payables is possible. Therefore, the risk of completeness for payables is often high. That's why auditors perform a search for unrecorded liabilities.

Do audit standards require a separate assessment of inherent risk?

While audit standards don't require a separate assessment on inherent risk (IR) and control risk (CR), it's wise to do so. Why? So you know what drives the risk of material misstatement (RMM). Many auditors assess control risk at high (after performing their risk assessment procedures). Why?

How is inherent risk assessed?

Inherent risk is assessed primarily by the auditor's knowledge and judgment regarding the industry, the types of transactions occurring at a particular company and the assets that the company owns. Usually, an auditor assesses each audit area as either low, medium or high in inherent risk.

What is inherent risk?

Inherent risk is one factor, along with control risk, that an auditor uses to assess the risk of material misstatement associated with a particular financial statement line item or audit area.

What is the risk of a company that has improperly reported a particular balance in the past?

A company that has improperly reported a particular balance in the past may be inherently more likely to misstate it again. These are the types of factors that auditors consider as they assess inherent risk. Assessing inherent risk tends to be a more subjective process than other components of the audit.

Is inherent risk subjective?

Assessing inherent risk tends to be a more subjective process than other components of the audit. However, there are often clear and observable factors to consider, such as the economy, the industry and previously known misstatements that help the auditor arrive at an assessed level of inherent risk for each audit area.

How is inherent risk measured?

Inherent risk is measured using two criteria―impact and likelihood. Inherent impact is the impact that an event would have on an organization should it occur and is measured in terms of magnitude, from the negligible to the extreme. Inherent likelihood speaks to the probability of the risk occurring in the absence of controls.

What is inherent risk?

Inherent risk is the level of untreated risk that an organization faces. It is defined as the magnitude of risk in the absence of any risk controls or mitigants. Inherent risk is difficult to conceptualize because it’s challenging to envision a scenario with absolutely no risk controls―most organizations have some level of controls already in place. To help clarify things, the FAIR Institute has proposed an alternate definition for inherent risk as “the current risk level given the existing set of controls rather than the hypothetical notion of an absence of any controls.”

What is residual risk?

The risk remaining after controls have been enacted is called residual risk. This residual risk, when measured against your organization’s risk appetite and risk thresholds, will help guide future planning and investment.

Why is residual risk scoring important?

Inherent and residual risk scoring is essential to the audit process. Assessments typically analyze the risks inherent in a given business line or process, the impact and efficacy of the mitigating controls, and the resulting residual risk exposure to the organization.

What is the role of organizations that operate with a clear eye view of what risks they face?

Organizations that operate with a clear-eyed view of what risks they face are better prepared to address evolving market dynamics, use risk as a strategic advantage, and build resilience.

Why is it important to define inherent risk?

Defining inherent risk is an important conceptual exercise but where it has the most impact is in its relationship to residual risk. Residual risk scoring is an important process to gauge the efficacy and strength of your organization’s controls. Controls can not reduce the impact of an inherent risk but they can reduce the probability ...

Is inherent risk considered residual risk?

Regardless of which definition is used, inherent risk is best understood when considered with residual risk. After identifying an inherent risk and introducing mitigating controls or processes, an organization is subject to a reduced level of risk.

How to Identify Risks

Risk identification is step #2 in a four-part risk management process which is introduced here. Step #1 is to set your risk threshold. Step 2 is identifying risks and this post is all about how to identify risks.

How to Identify Risks: Climate Change

The following is going to take you through a simplified risk identification process for a very complex thing, climate change. We’re going to do a very small part of a large view risk assessment for climate change and the United States, looking at it from the lens of one individual [I’ll use myself as the guinea pig].

How to Identify Risks: Primary Threats

Climate change. That’s the overhanging term for a thing that leads to a whole bunch of potential scenarios. Depending on scenario and geography it brings with it a whole host of threats.

How to Identify Risks: Vulnerabilities

Not all threats are going to impact all individuals or communities in the same way. There are a lot of factors involved – where those individuals and communities are, what their make-up is, etc.

Likelihood & Impact

Now here’s where it gets tricky. Well, not tricky so much as very specific. Normally when you do a risk assessment you want to make the thing you are evaluating as specific as possible. Say, I was evaluating for myself working in Harare, Zimbabwe. I have to drive there. I don’t know the place. I don’t know the roads. Those are vulnerabilities.

Conclusion

That’s it. You identify the threats, the vulnerabilities, the likelihood, and the impact given the current state of things. That is how one identifies the inherent risk in anything.

How to identify risks?

As you identify risks, you will need to write and capture risk statements in your risk register. One simple and powerful way to do this is to use the If-Then Risk Statements. The metalanguage is: If [Event], Then [Consequences]. For example: If the electrical system is not installed per the specifications, then there may be additional cost and an adverse impact to the schedule.

How many risk identification techniques are there?

Bonus: I will send you a sequence of emails where I describe each of the seven risk identification techniques in detail. You will also receive my weekly blog updates.

How to have an unengaged team?

Variety is the spice of life. One sure way to have an unengaged team is to use the same risk identification technique repeatedly. Additionally, mixing it up occasionally will help your team think in new ways and improve the identification process.

How much of all risks can be eliminated or greatly reduced through basic risk management?

Ninety percent of all risks can be eliminated or greatly reduced through basic risk management. Take note of these risk identification mistakes: The failure to recognize risks early when it is less expensive to address. Not identifying risks in an iterative fashion.

What is not identified with appropriate stakeholders?

Risks are not identified with appropriate stakeholders. Not using a combination of risk identification techniques. Risks are not captured in one location. The failure to make the risks visible and easily accessible. Risks are not captured in a consistent format (e.g., Cause -> Risk -> Impact).

Why is uncertainty high in project management?

The risk exposure is greatest at the beginning of projects. The uncertainty is high because there is less information in the beginning of projects. Wise project managers start identifying risks early in their projects. Additionally, capture your top risks in your project charter. Want to know how to improve your risk identification?

Why use cause and effect diagrams?

Cause and Effect Diagrams. Cause and Effect diagrams are powerful. Project managers can use this simple method to help identify causes--facts that give rise to risks. And if we address the causes, we can reduce or eliminate the risks.

Inherent Risk Formula

Important Points

- The inherent risk is directly related to the volume and the complexity of transactions performed by the business.

- If the volume and complexity achieved are adverse and high, then this can give birth to high IR.

- They are additionally prone to subjective estimates with zero groundwork.

- It also rises with the quick changes in the accounting policies within a short span of time.

Conclusion

- The audit risk model is composed of three broad risks, namely inherent risk, control risk, and detection risk. It is the responsibility of the auditor to assess the past audited results, perform investigations and have comprehensive discussions with the management at all levels of the organization to understand the nature of the business and results being achieved by the organiz…

Recommended Articles

- This is a guide to Inherent Risk. Here we discuss the Introduction and Examples of IR along with Components of Inherent Risk. You can also go through our other suggested articles to learn more – 1. Risk Assessment Example 2. Risk Management in Banks – Introducing Awesome Theory 3. Risk Management Process 4. Equity Ratio