The three primary methods in which fraud can be detected are:

- Tips

- Internal audit

- Management review

How to detect accounting frauds?

– One of the most obvious signs of accounting fraud is deposits or even checks that have not been included in the bank reconciliations. Keep a close eye out for deposits that are missing. Precluding a financial error, the chances are high that someone either absconded with the funds in question or made bogus payments of one sort or another.

What are the methods of detecting fraud?

The three primary methods in which fraud can be detected are:

- Tips

- Internal audit

- Management review

How to detect and prevent financial statement fraud?

- Corporate responsibility

- Increased criminal punishment

- Accounting regulation

- New protections

How to prevent accounting fraud?

- Managers performing clerical duties

- Purchasing agents that pick up vendor payments rather than having them mailed

- Staff that rewrites records under the pretense of neatness

- People that behave differently with their peers than they do with management or have abrupt mood swings and displays of highly emotional behavior (“Complainers”)

How is fraud usually detected?

Fraud is most commonly detected through employee tips, followed by internal audit, management review and then accidental discovery; external audit is the eighth most common way that occupational frauds are initially detected.

How do businesses detect fraud?

An anonymous tip line (or website or hotline) is one of the most effective ways to detect fraud in organizations. In fact, tips are by far the most common method of initial fraud detection (40% of cases), according to the Association of Certified Fraud Examiners (ACFE) 2018 Report to the Nations.

How is fraud detected and prevented?

The four most crucial steps in the fraud prevention and detection process include: Capture and unify all manner of data types from every channel and incorporate them into the analytical process. Continually monitor all transactions and employ behavioral analytics to facilitate real-time decisions.

Do auditors need to detect fraud?

82 clarifies, but does not increase, the auditors responsibility to detect fraud. The auditors responsibility is still framed by the key concepts of materiality and reasonable assurance.

How do auditors detect fraud?

Journal Entry Testing. Because committing material financial statement fraud often requires adjustments to the company's financial records, auditors will test the company's journal entries for any signs of manipulation.

What data is used in fraud detection?

The main AI techniques used for fraud detection include: Data mining to classify, cluster, and segment the data and automatically find associations and rules in the data that may signify interesting patterns, including those related to fraud. Expert systems to encode expertise for detecting fraud in the form of rules.

How do banks measure fraud?

Bank Fraud DetectionCash Transaction Monitoring. Identify cash transactions just below regulatory reporting thresholds. Identify a series of cash disbursements by customer number that together exceed regulatory reporting threshold. ... Billing. Identify unusually large number of waived fee by branch or by employee.

How does financial statements find fraud?

Tell-tale signs of accounting fraud include growing revenues without a corresponding growth in cash flows, consistent sales growth while competitors are struggling, and a significant surge in a company's performance within the final reporting period of the fiscal year.

How is cash fraud detected?

If your organization handles large amounts of cash at a time, purchasing a two-in-one bill counter, which also detects counterfeit currency, may serve as a solution to help detect counterfeit currency. Cash larceny is the removal of cash from the system after it has been recorded.

Do external auditors find fraud?

ACFE's Report to the Nations points out the fact that auditors rarely find fraud—internal audit detects fraud 15% of the time, while external audit merely 4% of the time. One reason auditors rarely find fraud is that audits are not designed to detect and/or prevent a fraud from occurring.

Fraud Prevention Plan

ACFE reasons that "fraud can flourish when employees believe they won't be caught." Thus transparency about anti-fraud controls and evidence of active detection through audits and monitoring software send a message to would-be criminals that they will be caught.

Create a Culture of Integrity

In conjunction with a documented plan, senior management need a zero fraud-tolerance culture. Expectations for ethics and accountability must come from the top and be promoted with broad reach and high frequency. Because employees take cues from their superiors (all the way to the C-suite), lack of integrity trickles down through the ranks.

Code of Conduct

This measure was shown to reduce the cost of fraud by 56% — the greatest reduction generated with any fraud controls studied in the Report to the Nations. Employees must know that they will meet high standards, which include ironclad avoidance of fraud.

Specific Detection Controls and Personnel

Transparency in detection controls is a highly effective deterrent. Controls may include software that monitors emails and financial activities, unplanned audits and surprise fraud assessments.

Ongoing Employee Training

Organizations that conducted fraud training saw a 41% reduction in money lost per case and a 50% reduction in duration of fraud campaigns before discovery. Employees should be trained in red flags and what constitutes fraud, and they must be encouraged to report suspicious activity without fear of retribution.

Training Starts in the MAcc Program

The Emporia State University Master of Accountancy online program includes an elective, Fraud Examination, that explores forensic accounting-related fraud, asset theft and financial statement misstatements. Topics include the nature of fraud, fraud prevention, detection methods, investigation procedure and types of fraud.

Top 5 Worst Accountants List

Let’s start things off with some of the worst accountants in the business. Unfortunately, there is an exhaustive list of horrible people posing as financial advocates. These guys make the cut on our list because they are examples of preventable accounting fraud discussed further in the article.

1. Andrew Fastow, Chief Financial Officer At Enron

He spearheaded a plan to hide liabilities in subsidiary holdings. The subsidiary holdings concealed losses attributed to shady mark-to-market (MTM) accounting tactics.

2. Arthur Andersen Of Arthur Andersen LLP

Arthur Andersen, a high-profile accountant, gets credit twice on this list. As the head of a top auditing firm in the country, he helped Enron avoid scrutiny from governing bodies. He would sign off on phony corporate statements, certifying their accounting as accurate.

3. Edward Cooper Of Jonesboro Accounting

He forged payments to himself from his client Roach Manufacturing. Edward accumulated $9 million in checks from 1996-2018, never reporting more than $70,000 in annual taxes. He and his wife enjoyed the money, splurging on the finer things: travel, jewelry, furs, and a $2 million cabin.

4. Andrew Munton Personal Accountant To The Stars

This accountant defrauded his celebrity clientele, including Rita Ora, out of 3.5 million euros. He falsified bank documents under client names to obtain credit. Then invested the money in lucrative football and star wars memorabilia. As well as funded his healthy gambling habit.

What Is Accounting Fraud?

Accounting fraud is the deliberate manipulation of accounting procedures and financial documents. It is an effort by an accountant, or employee at an organization, to fabricate a story of prosperous financial health. Such misinformation twists tax and business laws to influence investments from public and private sectors.

Creative Accounting vs Accounting Fraud

Creative accounting, aka aggressive accounting, is a lesser form of accounting fraud. In the financial industry it is the exploitation of generally accepted accounting standards; a reinterpretation of accounting policies that push the boundaries of true reporting.

What Is Financial Statement Fraud?

The Association of Certified Fraud Examiners (ACFE) defines accounting fraud as "deception or misrepresentation that an individual or entity makes knowing that the misrepresentation could result in some unauthorized benefit to the individual or to the entity or some other party." Put simply, financial statement fraud occurs when a company alters the figures on its financial statements to make it appear more profitable than it actually is, which is what happened in the case of Enron..

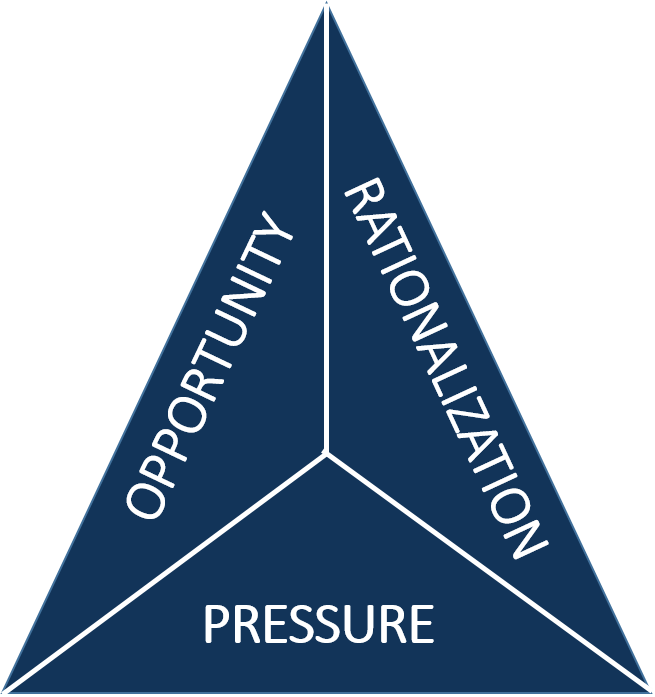

Financial Statement Fraud Red Flags

Financial statement red flags can signal potentially fraudulent practices. The most common warning signs include:

Financial Statement Fraud Detection Methods

While spotting red flags is difficult, vertical and horizontal financial statement analysis introduces a straightforward approach to fraud detection. Vertical analysis involves taking every item in the income statement as a percentage of revenue and comparing the year-over-year trends that could be a potential flag cause of concern.

The Bottom Line

Federal authorities have put laws in place that make sure companies report their financials truthfully while protecting the best interests of investors. But while there are protections in place, it also helps that investors know what they need to look out for when reviewing a company's financial statements.

Why is there no accounting fraud?

No accounting fraud has taken place because the errors were not deliberate. Now suppose the CEO of a publicly-traded company knowingly makes false statements about the firm's prospects. The Securities and Exchange Commission ( SEC) may well charge that CEO with fraud. However, it is not accounting fraud because no financial records were falsified.

What are some examples of accounting fraud?

Overstating revenue, failing to record expenses, and misstating assets and liabilities are all ways to commit accounting fraud. The Enron scandal is one of the most famous examples of accounting fraud in history.

How can a company falsify its financial statements?

A company can falsify its financial statements by overstating its revenue, not recording expenses, and misstating assets and liabilities.

Why did Enron use off balance sheet entities?

Enron used off-balance-sheet entities to hide the company's debts from investors and creditors. Although using such entities was not illegal in itself, Enron's failure to disclose the necessary details of its dealings constituted accounting fraud.

Can a company commit accounting fraud?

A company can commit accounting fraud if it overstates its revenue. Suppose company ABC is actually operating at a loss and not generating enough revenue. To cover up this situation, the firm might claim to be producing more income on financial statements than it does in reality. On its statements, the company's profits would be inflated. If the company overstates its revenues, it would drive up the firm's share price and create a false image of financial health.

What is accounting fraud?

Accounting Fraud. An employee who manipulates a company’s accounts to cover up theft or uses the company’s accounts payable and receivable to steal commits accounting fraud. Employees involved in these types of fraud are generally those in positions that have access to a company’s accounts with little or no oversight.

What are the challenges of detecting fraud?

Types of Fraud and Theft. One of the biggest challenges of detecting, investigating and preventing employee fraud is the fact that there are so many types of fraud and theft that require different methods for discovery. Every department presents opportunities for employees to steal, although it’s been widely reported that a disproportionate ...

How long does payroll fraud last?

It’s one of the most common types of employee fraud – according to the ACFE it occurs in 27 per cent of businesses and lasts for an average of 36 months.

What is trade secret theft?

Data or theft or theft of trade secrets in one type of employee fraud that can be devastating to a company that relies on its intellectual property for its product or service.

What is asset misappropriation?

Asset misappropriation is a broad term that describes a vast number of employee fraud schemes. Simply, it’s the theft of company assets by an employee, also known as insider fraud. Asset misappropriation schemes include:

How does a billing scheme work?

In a billing scheme, an employee generates false payments to himself/herself using the company’s vendor payment system either by creating a fictitious vendor (shell company) or by manipulating the account of an existing vendor.

What is check kilting?

Check Kiting. An employee writes checks on an account that doesn’t have sufficient funds with the expectation that the funds will be in the account before the check clears. This type of fraud scheme is less common nowadays, with faster check clearing times.

Fraud Prevention Plan

Create A Culture of Integrity

- In conjunction with a documented plan, senior management need a zero fraud-tolerance culture. Expectations for ethics and accountability must come from the top and be promoted with broad reach and high frequency. Because employees take cues from their superiors (all the way to the C-suite), lack of integrity trickles down through the ranks. For this reason, an open door policy that …

Code of Conduct

- This measure was shown to reduce the cost of fraud by 56% — the greatest reduction generated with any fraud controls studied in the Report to the Nations. Employees must know that they will meet high standards, which include ironclad avoidance of fraud.

Specific Detection Controls and Personnel

- Transparency in detection controls is a highly effective deterrent. Controls may include software that monitors emails and financial activities, unplanned audits and surprise fraud assessments. Employing experts in fraud control furthers the perception that getting away with wrongdoing will be impossible. Publishing information on LinkedIn, as well...

Ongoing Employee Training

- Organizations that conducted fraud training saw a 41%reduction in money lost per case and a 50% reduction in duration of fraud campaigns before discovery. Employees should be trained in red flags and what constitutes fraud, and they must be encouraged to report suspicious activity without fear of retribution. Also, someone within the organization, or perhaps a contracted third …

Training Starts in The Macc Program

- The Emporia State University Master of Accountancy online program includes an elective, Fraud Examination, that explores forensic accounting-related fraud, asset theft and financial statement misstatements. Topics include the nature of fraud, fraud prevention, detection methods, investigation procedure and types of fraud. Given the high cost of fraud in financial loss and ruin…