Is cash flow statement mandatory for a company?

Cash flow statement (CFS) is mandatory. As per Sec 2(40) for “financial statement” in relation to a company, includes— (i) a balance sheet as at the end of the financial year; (ii) a profit and loss account, or in the case of a company carrying on any activity not for profit, an income and expenditure account for the financial year; (iii)...

How often should I prepare a cash flow statement?

The frequency you choose should depend on how your business will use the statement and whether more regular reporting will provide a greater benefit. There are two main methods for preparing a cash flow statement to consider: the direct method and the indirect method.

What is the purpose of preparing statement of cash flows?

Statement of cash flows and the purpose of its preparation. The presentation of SCF is essential for the companies that are required to prepare and present their financial statements in accordance with international accounting standards (IASs) and international financial reporting standards (IFRSs).

Should you use the direct or indirect method to prepare cash flow statements?

That said, there are additional potential complexities to choosing the direct method to prepare cash flow statements. For one, since most companies use accrual basis accounting, the indirect method more naturally fits with their current accounting practices.

For which company it is compulsory to prepare cash flow statement?

Preparation of Cash Flows statements for all companies (except one person Company, Small Co and Dormant Co.) are mandatory as per Companies Act 2013. Earlier only listed companies covered under listing agreement of clause no 32 we required to prepare Cash Flow Statements.

Who are exempted from preparing cash flow statement?

Explanatory notesThus, cash flow statements are to be prepared by all companies but the act also specifies a certain category of companies which are exempted from preparing the same. Such companies are One Person Company (OPC), Small Company and Dormant Company.

Is statement of cash flows optional?

The statement of cash flows is an optional financial statement. The statement of cash flows shows the effects on cash of a company's operating, investing, and financing activities.

Why it is mandatory to prepare a statement of cash flow by a business organization?

Cash flow statement will assist the business to properly group it activities better, it will make it know whether an activity is either investing, financing or operating activity. With the cash flow preparation, the business is able to make future finance decision for proper running of the business activities.

Do small companies need a cash flow statement?

Entities that are classified as small under the Companies Act 2006 do not have to prepare a cash flow statement as part of their statutory financial statements; however, that does not mean to say that they are precluded from preparing such a statement, if the directors so wish.

Why cash flow statement is required?

Why is the Cash Flow Statement Important to Shareholders and Investors? The Cash Flow Statement (CFS) provides vital information about an entity. It shows the movement of money in and out of a company. It helps investors and shareholders understand how much money a company is making and spending.

Does IFRS require cash flow statement?

Under IFRS Standards, there are no scope exceptions and all companies must present a statement of cash flows in a complete set of financial statements.

When did cash flow statement become required?

The balance sheet and income statement have been required statements for years, but the cash flow statement has been formally required in the United States only since 1988.

What are the limitations of cash flow statement?

Here we detail about the six limitations of cash flow statement!(a) Fails to Present Net Income: ... (b) Fails to Assess the Liquidity and Solvency Position: ... (c) Neither a Substitute of Funds Flow Statement nor Income Statement: ... (d) Not to Assess Profitability: ... (e) Does not Conform with the Companies Act:More items...

What is a purpose of preparing a cash flow statement how is it prepared?

The statement of cash flows is one of the most important financial reports to understand because it provides detailed insights into how a company spends and makes its cash. By learning how to create and analyze cash flow statements, you can make better, more informed decisions, regardless of your position.

What are the four primary purposes of the statement of cash flows?

The primary purpose of the statement of cash flows is to provide information about cash receipts, cash payments, and the net change in cash resulting from the operating, investing, and financing activities of a company during the period.

Who prepare cash flow statement?

Alongside Balance Sheet and Income Statement, all registered companies are mandated to prepare a cash flow statement, according to the revised Accounting Standard – III (AS – III). It shall be noted that a cash flow statement is fundamentally distinct from a Balance Sheet or an Income Statement.

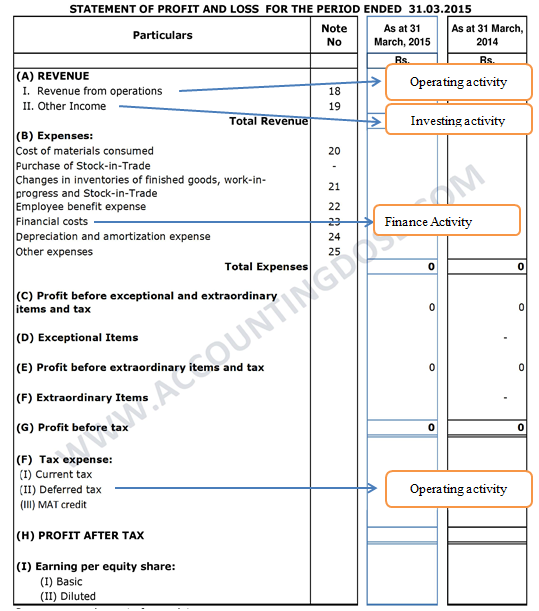

Three Main Sections of Statement of Cash Flows

1. Operating Activities: The principal revenue-generating activities of an organization and other activities that are not investing or financing; a...

How to Prepare A Statement of Cash Flows?

The operating section of the statement of cash flows can be shown through either the direct method or the indirect method. For either method, the i...

Direct Method vs Indirect Method of Presentation

There are two methods of producing a statement of cash flows, the direct method, and the indirect method.In the direct method, all individual insta...

What Can The Statement of Cash Flows Tell Us?

1. Cash from operating activities can be compared to the company’s net income to determine the quality of earnings. If cash from operating activiti...

What is the rule 7 of the Companies Act?

Rule 7 of the Companies (Accounts) Rules, 2014 provides that as a transition provision, the standards of accounting as specified under the Companies Act, 1956 (i. e. the Companies (Account ing Standards) Rules , 2006) shall be deemed to be the accounting standards until accounting standards are specified by the Central Government under Section 133.

Does AS 3 apply to cash flow statements?

Thus, under the Companies Act, 2013, non-listed companies will have a choice of either applying the direct or indirect method under AS 3 to prepare the cash flow statement. Due to the listing agreement requirement, that choice will not be available to listed companies.

Does the Company Act 1956 include cash flow statements?

Earlier, The Company act 1956 didn’t include cash flow statement in the Definition of Financial statement. The Applicability of Cash Flow Statements is governed by the Companies (Accounting Standards) Rules, 2006. However as per the company act 2013, the Cash flow statement shall to prepare and included in Financial Statements subject ...

Is a cash flow statement mandatory?

Please remember, it’s not a mandatory provision. Despite non Applicability of Cash Flow Statement If a small companies want then they can prepare their cash flow statements and file it with registrar of companies or ROC.

Do all companies have to include cash flow?

The inclusion of cash flow along with balance sheet and P&L for all companies is a new requirement. Earlier only listed companies under listing agreement clause no. 32 are required to prepare cash flow statement as per AS 3 of Accounting standards issued by the ICAI.

Is a cash flow statement applicable to all companies?

Simply, We can state that the cash flow statement is applicable for all companies ( including Private Company) however the certain exemption is provided to OPC, Dormant Companies and Small Companies in respect of Applicability of Cash Flow Statement.

Does a one person company include a cash flow statement?

Provided that the financial statement, with respect to One Person Company, small company and dormant company, may not include the cash flow statement

Does the Company Act 1956 include cash flow statement?

Earlier Company act 1956 didnt include cash flow statement in the Defination of Financial statement, However as per New Company Act 2013, the Cash flow statement shall to prepare.

Is a cash flow statement required for all companies?

Simply cash flow statement is SHALL prepared for all companies (including Private Company) however exemption is give to following three companies only

What is the statement of cash flows?

The statement of cash flows is part of the financial statements, of which the other two main statements are the income statement and balance sheet. The statement of cash flows is closely examined by financial statement users, since its detailed reporting of cash flows can yield insights into the financial health of a business.

What is the most commonly used format for the statement of cash flows?

The most commonly used format for the statement of cash flows is called the indirect method. The general layout of an indirect method statement of cash flows is shown below, along with an explanation of the source of the information in the statement.

Why is cash flow important?

It is one of the important principles of Accounting. The information about daily inflow and outflow of cash and historic changes in the same is very important for every business. To take any decisions, cash flow statements help to evaluate the capacity of an enterprise to generate cash and cash equivalents, the timing and their certainty ...

What is cash inflow statement?

It is a statement that provides detailed analysis by which enterprises can determine the capacity of an organisation to generate cash and cash equivalents and planning on utilising such available cash into the business. The enterprises regularly evaluate cash inflows and outflows for effective decision making on utilising funds.

What is financial statement?

The definition of financial statements states that the Financial Statements in relation to Company include: a balance sheet as at the end of the financial year; a profit and loss account, or in the case of a company carrying on any activity, not for profit, an income and expenditure account for the financial year; ...

Do all public companies have to include cash flow statement?

Therefore, apart from the above-mentioned companies, all public limited companies, listed companies and private limited companies are required to include cash flow statement in their financial statements.

Is a cash flow statement applicable to a private company?

Yes, Cash Flow statement is applicable to all private limited companies except: One Person Company. Small Company. Dormant Company and. A Private Limited company recognised as a start-up in accordance with the notification issued by Industrial Policy and Promotion, Ministry of Commerce and Industry.

What is the best way to prepare a cash flow statement?

There are two main methods for preparing a cash flow statement to consider: the direct method and the indirect method. While the indirect method is more common, the better choice between the two will depend on how much detail you need to include in your statement and how much time you are willing to devote to the process in order to improve your long term decision making. (See below for a further discussion about choosing the right method for your financial reports.)

Why is a cash flow statement important?

It can help you and other stakeholders clearly see how your business earns or spends cash, and it can provide valuable insight into your company financials . It also can help you spot business trends that can improve your overall business decision-making and make better use of your profits. A cash flow statement breaks down the various types ...

Why does the direct method take more time?

The direct method generally takes more time and number-crunching because you are subtracting actual cash outflows from inflows rather than simply adjusting the net income. Common line items using the direct method include:

What is indirect method in cash flow?

For the operating activities section of the cash flow statement, the indirect method involves first showing the company’s net income (which should be found easily on your company income statement). You then show any noncash inflow or outflow adjustments that need to be made in order to calculate the total operating activities cash flow. Common adjustments, for example, include:

Why do we use direct method?

Most accounting standard-setting entities (including FASB) prefer the direct method, though, because of the higher level of insight it provides. If you choose to go the direct method route, you’ll want to start regularly tracking your cash inflows and outflows in the way you’ll be reporting it—so that putting together the cash flow statement won’t be too much of a burden.

What is cash flow from operations?

Cash flows from operations are integral to your cash flow statement. Investing activities cash flow. This is the money spent on and generated from market securities, long term assets, and other financial instruments over the reporting period.

What is indirect accounting?

The indirect method is based on accrual basis accounting—which means revenues and expenses are counted when they are incurred, not when money actually changes hands. Most companies use the accrual basis of accounting method, which is partly why this method is so popular.

What is a cash flow statement?

The statement of cash flows (SCF) is an important financial statement that shows the details of the company’s cash flows for an accounting period. It tells us how much cash has been received or paid by a business during its accounting period.

What is a statement of cash flows?

Statement of cash flows and the purpose of its preparation. The term cash flows refers to the receipts and payments of cash. Companies periodically disclose the cash flows arising from its various activities in the form of a statement. This statement is known as statement of cash flows (or cash flow statement).

What is non-cash investing?

Companies also engage in various investing and financing activities that do not require the use of cash. Such activities are known as non-cash investing and financing activities. Sometime these activities have a significant impact on the future cash flows of the entity and therefore their disclosure to the users of financial statements becomes necessary. For this purpose, a company that performs any significant non-cash investing and financing activity during the accounting period must disclose it either in the statement of cash flows or in the footnotes to the financial statements.

What are the three types of cash flows?

To properly report these three types of cash flows, the statement of cash flows is divided into three sections – operating activities section, investing activities section, and financing activities section. (Read ‘three sections of the statement of cash flows ’ article).

What is SCF in accounting?

The presentation of SCF is essential for the companies that are required to prepare and present their financial statements in accordance with international accounting standards (IASs) and international financial reporting standards (IFRSs).

Do companies have to prepare financial statements?

In some countries, the companies are legally required to prepare and present financial statements in accordance with international financial reporting standards (IFRSs). As the statement of cash flows (SCF) is one of the basic components of financial statements, its presentation is legally required in some countries.