Is it hard to buy a house if you have student loans?

You can still buy a home with student debt if you have a solid, reliable income and a handle on your payments. However, unreliable income or payments may make up a large amount of your total monthly budget, and you might have trouble finding a loan.

Should I pay off my student loans first before buying a house?

If the amount of money you bring in monthly or yearly is almost the same as the amount of money you pay out in debts — like student and car loans or credit cards — it may be best to pay down your debt before buying a house.

Is it better to save for a house or pay off student loans?

That's because student loans have longer repayment terms and typically feature lower interest rates. Since your down payment will lower the overall cost of your mortgage, it may be more advantageous to save up money for a home than to pay off a low-interest student loan.

Do mortgage lenders look at student loans?

Student loan debt can make it harder — but not impossible — for you to get a mortgage. Lenders consider student loan debt as a part of your total debt-to-income (DTI) ratio, which is a vital indicator of whether you'll be able to make your future mortgage payments.

Should I aggressively pay off student loans?

Pay less over the life of the loan: Because your student loan, like most other debt, accrues interest when you carry a balance, it's cheaper if you pay off the loan earlier. It gives the debt less time to accumulate interest, which means that you'll pay less money in the long run.

Is 50k in student loans a lot?

Is $50,000 in student loan debt a lot? The resounding answer is yes, $50,000 is a lot of student loan debt. But when you consider the cost to attend college and that most students take four to five years to graduate, that figure isn't a surprise.

How much money should you save to buy a house?

If you're getting a mortgage, a smart way to buy a house is to save up at least 25% of its sale price in cash to cover a down payment, closing costs and moving fees. So, if you buy a home for $250,000, you might pay more than $60,000 to cover all of the different buying expenses.

What is the average amount of student loan debt?

Though 2021 college graduates who borrowed to pay for school took out, on average, $208 less in loans compared with the prior year, the average total student debt continues to hover around $30,000, according to U.S. News data.

Should I pay off car or mortgage first?

If you're trying to diminish the total sum owed, you should use your extra cash to pay off your debt with the highest interest rate first. For example, if your mortgage has a high interest rate, it might behoove you to pay off this loan first, even if your auto loan has a smaller balance.

Do student loans get forgiven?

You qualify to have up to $10,000 forgiven if your loan is held by the Department of Education and you make less than $125,000 individually or $250,000 for a family. If you received Pell grants, which are reserved for undergraduates with the most significant financial need, you can have up to $20,000 forgiven.

Can I negotiate my student loan debt?

Student loan settlement is possible, but you're at the mercy of your lender to accept less than you owe. Don't expect to negotiate a settlement unless: Your loans are in or near default. Your loan holder would make more money by settling than by pursuing the debt.

What is a good debt-to-income ratio?

What do lenders consider a good debt-to-income ratio? A general rule of thumb is to keep your overall debt-to-income ratio at or below 43%.

When Might You Consider Buying a House While You Still Have Student Debt?

After weighing the pros and cons, if you are still unsure whether purchasing a home while you have student loan debt is a good decision for you, check out these scenarios where buying a home may be better fit:

What happens if you default on a student loan?

If you have any student loans in default, you will need to rehabilitate the loan before you will be able to obtain a mortgage so that the default will not remain on your credit history. Having a federal student loan in default will prevent you from qualifying for an FHA mortgage, which is typically easier to qualify for since it requires a lower down payment and has easier credit guidelines to meet.

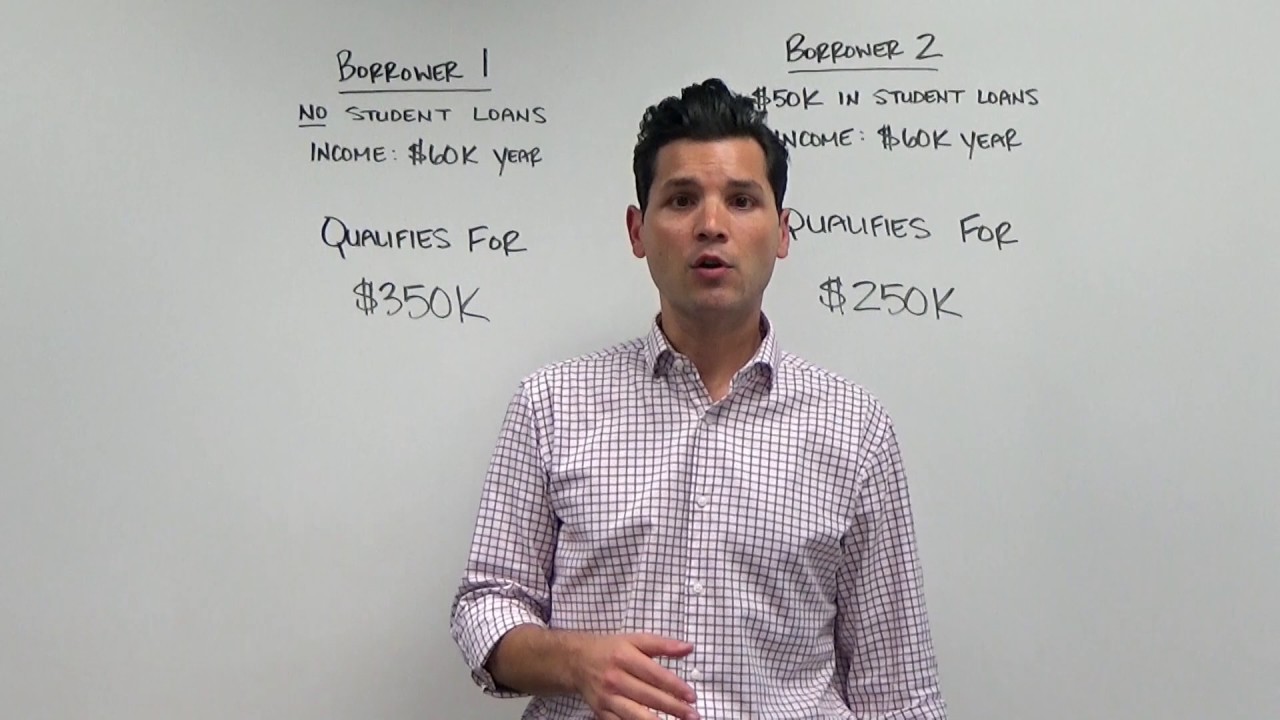

Can student loan debt be too high for a mortgage?

If you have a large amount of student loan debt your debt-to-income ratio may be too high to qualify for a mortgage or may qualify you for a less than stellar interest rate or mortgage type. This could cause you to end up paying even more in interest for the mortgage.

Can you use extra money to pay off student loans?

If you are saving for a down payment or purchase a house and then have to pay for maintenance and upkeep, you may be using extra funds that could have been put towards your student debt. This could slow down your student loan repayment process, and cause you to pay more in interest over time.

Can my home increase in value?

If you make a wise financial purchase, it’s possible that your home could increase in value, especially if you improve upon it while living there. If you wait until your student debt is paid off, you may miss out on a wealth-building asset.

Is it better to buy a house with student loan debt or a lot of inventory?

If you are able to take advantage of a buyer’s market, that’s a plus, even if you still have student loan debt. Buying a house when there is a lot of inventory gives you more choices and possibly allows you to buy a house for less than the median price.

Can I get a mortgage with student loans in deferment?

If you are attempting to purchase a home with student loans in deferment you may find it difficult to qualify for a mortgage, especially a FHA mortgage. For a FHA mortgage, deferred loans are still included in your debt-to-income ratio. The FHA will calculate your DTI by taking 1% of the deferred student loan balance, which may be higher than what your actual payment may end up being. This can make it difficult to qualify for the mortgage based on a high DTI ratio.

What happens when you apply for a mortgage?

When you apply for a mortgage, your lender will assess all of your existing monthly payment obligations, including student loans, to determine whether you would be able to manage the additional monthly payment. Depending on your situation, the lender will decide whether you qualify for the new loan, and if so at what interest rate. [.

How to check your credit score before applying for a mortgage?

You can check your credit score before applying for a mortgage through your bank or at AnnualCreditReport.com, which is monitored by the Federal Trade Commission and the Consumer Financial Protection Bureau. If you have a low credit score, consistently making your student loan payments on time is a great way to build and improve your credit and to get a mortgage – with a good interest rate.

How does a lender calculate your debt to income ratio?

The lender calculates your debt-to-income ratio by adding up all your existing monthly debt payments and your expected mortgage amount.

Why do lenders use credit score?

Lenders use your credit score to help decide whether you qualify for a mortgage, as well as to determine the loan's interest rate. Borrowers with higher credit scores are usually eligible for lower interest rates, while interest rates increase for borrowers with lower credit scores.

What is the minimum debt to income ratio for a mortgage?

Most lenders will not approve a mortgage if an applicant's debt-to-income ratio exceeds 43%. Ideally, it should be at or under 36%, with the maximum for monthly mortgage-related payments under 28%, experts say.

Can student loan debt affect home buying?

How Student Loan Debt Affects Homebuying. While too much existing debt is likely to affect your interest rate, in most cases you can still consider buying a home if you are ready. (Getty Stock) With current mortgage rates at historic lows, you may want to consider buying a home soon if you are ready to take that step.

Can you lower your student loan payment?

Just keep in mind that lowering your monthly payment on student loans could increase the amount that you will pay over time if you pay the loan for a longer period of time and accrue more interest.

How to refinance student loans?

Refinancing turns multiple loans into one, at an interest rate based on your financial history. To qualify, you’ll need a credit score in the high 600s or above, solid income and a history of on-time debt payments.

How much of your income should you spend on necessities?

If you feel defeated, try making a budget using the 50/30/20 plan, which encourages you to spend 50% of your income on necessities, 30% or less on wants and 20% or more on savings. That will give you a framework for saving and help you determine how long it will take.

What is the most important thing to consider when buying a home?

Disposable income that can go towards home expenses like new appliances, repairs and renovations is an important factor of homeownership. If your budget allows for these things, you should consider buying a home.

What happens if you default on a mortgage?

Defaulting on your loans has a severe negative impact on your credit score, which tells lenders that you’re a bigger risk to take on. Work on improving your credit score before shopping for a mortgage.

What happens after college?

After college, life moves fast . You get your first big job, move out of your parents’ house and start a whole new life on your own. For most people, this also means paying off student loan debt from your college tuition. Having this debt may make big milestones like buying a house seem far off, but there are ways to make ...

Can student loans prevent you from getting a mortgage?

Typically, student loan debt doesn’t prevent you from getting a mortgage. The biggest thing to note is that student loan debt does influence your debt-to-income ratio, which is a factor lenders consider before giving you a loan. It can also affect the interest rate you pay on your mortgage.

Can you get a mortgage if you defer your student loan?

If you’ve deferred your student loans, this usually won’t affect your chances of getting a mortgage. Just be sure to consider how the future estimated payments will factor your debt-to-income ratio. Some types of mortgages may reject applicants with deferred loans, so do your research on the different types of mortgages before shopping.

Is it good to have enough money to pay down on a house?

You’ve saved for a down payment. Having enough money in your savings to cover a decent down payment on a home is a good indicator that you’re ready to be a homeowner. And if you have the income to handle closing costs and fees, you’re even better equipped to buy a home.

Should You Pay Off Student Loans Before Buying a House?

But if you have enough income to handle the payments for both, you may want to consider investing in your first home.

Why is it important to get a preapproval for a student loan?

It’s important to get a preapproval because it helps you shop for homes within your budget.

What do underwriters look for in a loan?

Underwriters will look at your: 1 Current debt 2 Credit score 3 Income 4 Unusual activity in your recent bank account transactions 5 Other assets you have

Should I pay more than my minimum mortgage?

In this situation, you should pay more than your minimum and focus on paying off your loans first before you take on more debt with a mortgage. However, now is likely a good time to buy a home if you have an emergency fund, your DTI is low, you’re contributing to your retirement and you’re on a solid repayment plan.

Should I wait to buy a home before I buy a home?

You may want to hold off until you build up a fund if you have a reasonable DTI ratio but you don’t have an emergency fund. In the same vein, if your student loan payment is standing in the way of retirement contributions, wait to buy a home until you pay down more of your debt. Also bear in mind that most mortgages require a down payment when you purchase a home.

Do you have to be 100% debt free to get a student loan?

How Student Loans Are Viewed By Lenders. You don’t need to be 100% debt- free to buy a home or qualify for a mortgage. However, one of the most important things that lenders look at when they consider you for a loan is your current debt, including any associated with your student loan.

Should You Pay Down Your Student Loans Before Buying A House?

You can still buy a home with student debt if you have a solid, reliable income and a handle on your payments. However, unreliable income or payments may make up a large amount of your total monthly budget, and you might have trouble finding a loan. Focus on paying down your loans before you buy a home if your DTI is more than 50% .

How Student Loans Affect Your Ability to Buy a House

When you have a student loan balance, it can affect your debt-to-income ratio (DTI), which is one of the most important factors that lenders consider. DTI is your monthly debt payments, including your future mortgage payments, divided by your monthly gross income.

Pros of Refinancing Your Student Loans

There are several reasons why refinancing student loans before buying a house makes sense.

Cons of Refinancing Your Student Loans

There are also some downsides to refinancing your student loans. Here’s what you should be aware of.