Should I Pay an Escrow Shortage in Full?

- Understanding Shortage Causes. The Real Estate Settlement Procedures Act, or RESPA, regulates escrow accounts. In...

- RESPA and Your Options. RESPA also requires the loan servicer to conduct an annual escrow analysis on each account, and...

- Picking Your Payment Plan. Your loan servicer will give you the option of paying an escrow...

What are my options for an escrow shortage?

What are my options for paying my escrow shortage? You have three options for paying a shortage: Option 1: Pay nothing and spread the shortage amount evenly across next year’s payments. Option 2: Pay the full shortage now. Please note, if your tax and/or insurance expenses have increased, your monthly mortgage payment may still go up, even if ...

What causes an escrow shortage on your mortgage?

What causes an escrow shortage on your mortgage? The most common reason for a shortage – or an increase in your payments – is an increase in your property taxes. In other words, an escrow shortage is the result of not having enough money in your escrow account to cover the actual amount needed to pay your bills.

Should I pay down the mortgage?

There’s also an incentive to pay down your mortgage if your rate is particularly high. The further above that 4.5% average your mortgage is, the better the case for paying it down. And if you have an adjustable rate mortgage, then paying down your mortgage helps blunt the impact of future rate increases.

Should I pay cash or get mortgage?

Paying cash for a home means you won't have to pay interest on a loan and any closing costs. A mortgage can provide tax benefits for some and means a buyer will likely have more cash in the bank to...

What do you do with an escrow shortage?

Pay off the shortage in full: You can make a one-time payment to your mortgage company that would cover paying back any existing deficiency and/or getting you back up to the required minimum balance based on your new monthly escrow payment. This lump sum payment is applied directly to your escrow account.

How can I avoid escrow shortage?

Again, the key to preventing escrow shortage and/or deficiencies is to keep an eye out for your property tax assessment, as well as your homeowner's insurance. The sooner you can catch the increase the less likely you will have a shortage and/or deficiency.

Is it worth paying escrow?

Pros of an escrow account Having your mortgage lender or servicer hold your property tax and homeowners insurance payments in escrow ensures that those bills are paid on time, automatically. In turn, you avoid penalties such as late fees or potential liens against your home.

Should I pay off my escrow balance?

Both the principal and your escrow account are important. It's a good idea to pay money into your escrow account each month, but if you want to pay down your mortgage, you will need to pay extra money on your principal. The more you pay on the principal, the faster your loan will be paid off.

How long does escrow shortage last?

12 monthsHow long will I have the extra amount in my mortgage payment for an escrow shortage? Escrow shortages are calculated to be paid back over 12 months. After 12 months this portion is automatically removed from your payment, and another analysis of the escrow account will occur.

Is it normal for escrow to increase every year?

Even with a fixed-rate loan, the property tax rate or insurance rate may change, resulting in a change in the escrow balance throughout the year. The lender sends an account analysis once a year, and you will end up paying more as costs increase.

Can you remove escrow from your mortgage?

Lenders also generally agree to delete an escrow account once you have sufficient equity in the house because it's in your self-interest to pay the taxes and insurance premiums. But if you don't pay the taxes and insurance, the lender can revoke its waiver.

How much money should you have in escrow?

To ensure there's enough cash in escrow, most lenders require a minimum of 2 months' worth of extra payments to be held in your account. Your lender or servicer will analyze your escrow account annually to make sure they're not collecting too much or too little.

What happens if I pay an extra $200 a month on my mortgage?

If you pay $200 extra a month towards principal, you can cut your loan term by more than 8 years and reduce the interest paid by more than $44,000. Another way to pay down your loan in less time is to make half-monthly payments every 2 weeks, instead of 1 full monthly payment.

Why is my escrow short every year?

This means your escrow account has insufficient funds to make all the necessary payments for property taxes and insurance. This can happen for a few reasons: An unanticipated increase in your property taxes or insurance.

Why does my escrow keep increasing?

The most common reason for a significant increase in a required payment into an escrow account is due to property taxes increasing or a miscalculation when you first got your mortgage. Property taxes go up (rarely down, but sometimes) and as property taxes go up, so will your required payment into your escrow account.

Should I pay off principal or escrow first?

If you're stuck between paying down the balance on the principal or escrow on your mortgage, always go with the principal first. By paying towards the principal on your mortgage, you're actually paying on the existing debt, which brings you closer to owning your home.

What causes an escrow shortage on your mortgage?

This means your escrow account has insufficient funds to make all the necessary payments for property taxes and insurance. This can happen for a few reasons: An unanticipated increase in your property taxes or insurance.

How do I keep my mortgage from going up?

Here are some different ways you can lower your monthly mortgage payment.Refinance your mortgage to a lower rate. ... Refinance to a longer term mortgage. ... Remove private mortgage insurance. ... Apply for mortgage forbearance. ... Request a mortgage recast. ... Shop for homeowners insurance. ... Apply for a mortgage loan modification.

Why did my mortgage payment go up 2022?

The answer to why your payment changed may simply be that your lender has added new fees to your monthly bill, increasing your payment. It's usually possible to avoid such servicing fees. To find out, check your monthly mortgage statement to see if any new items were added.

Why does my escrow keep increasing?

The most common reason for a significant increase in a required payment into an escrow account is due to property taxes increasing or a miscalculation when you first got your mortgage. Property taxes go up (rarely down, but sometimes) and as property taxes go up, so will your required payment into your escrow account.

How often do escrow analysts go out?

Escrow analyses are sent out to borrowers once per year. However, it’s possible for a lender or servicer to complete more than one analysis in a year if there are issues with the first one or if the borrower disputes their analysis. Typically, though, they’ll do just one escrow analysis each year.

How often do you need escrow analysis?

Escrow analyses are performed by your lender or servicer at least once per year. This analysis will tell you if you have a shortage and if your monthly payments will be increasing in the next year due to an increase in your taxes or insurance rate. In your escrow analysis, your servicer will project how much you’ll owe out ...

How is escrow funded?

Your escrow account is funded by your monthly mortgage payments. Let’s look at an example: You buy a home that has an annual property tax bill of $4,500 and costs $1,500 per year to cover with a homeowners insurance policy. Paying all of this in one lump sum, or even divided into semiannual payments, can be tough on your wallet.

How long does it take to pay escrow shortage?

Many lenders, including Rocket Mortgage®, allow borrowers to either pay their escrow shortage in one lump sum or to spread out the payment in equal monthly installments over a 12-month period.

What does it mean when you have an escrow deficiency?

If you have an escrow deficiency, that means that your escrow account has a negative balance. This can happen if your tax or insurance bills came due and you didn’t have enough money in your account to cover them, so your lender had to pay the remaining balance for you using their own funds.

What is it called when an escrow account doesn't have enough money?

When that account doesn’t have enough money in it to cover these costs, however, that’s called an escrow shortage . Why does this happen? Let’s take a look.

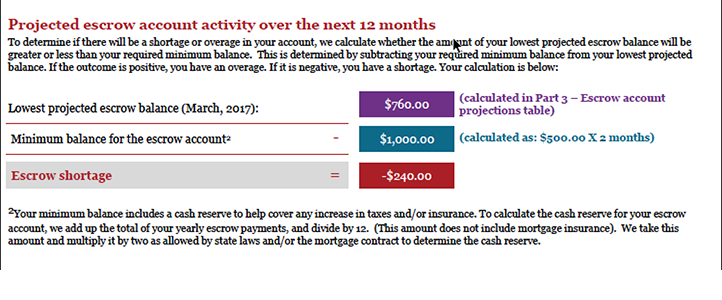

What is escrow shortage?

When you have a mortgage, your escrow account enables you to make payments toward your property taxes and insurance in more manageable, monthly increments, rather than having to cover these costs all in one big lump sum each year. When that account doesn’t have enough money in it to cover these costs, however, that’s called an escrow shortage.

Why Do Escrow Shortages Occur?

The money in these accounts comes directly from your monthly mortgage payment. However, it’s important to understand what you are paying for each month:

Should I Pay Off My Escrow Balance?

Escrow shortages are very common but do affect your mortgage payments. Still, there are ways you can avoid these problems in the future. Here are some tips for all homeowners that are dealing with escrow shortages and/or increases in their monthly payments:

How To Avoid Escrow Shortage?

The second thing you can do to avoid an escrow shortage or deficiency is to set aside money or make a special payment towards your escrow account so that you can avoid future issues.

Can I Reduce My Escrow Payment?

While it is possible to reduce escrow payments, it is important to keep in mind that escrow accounts are based on insurance premiums and your property tax. You should try to shop around for homeowners insurance policies before committing to one, as many insurance companies offer discounts when policies are bundled together. U.S. military members, including veterans and disabled veterans are sometimes offered discounts depending on the insurance company. You can also look into available tax exemptions that may reduce the amount of property taxes you owe.

What are the items included in an escrow account?

Items that are normally included are hazard, flood, and mortgage insurance, property taxes, ground rents, and special assessments.

Why are there property tax shortages?

Another common reason for shortages is an increase in your property taxes. With the latter, your monthly payments will increase as well. As an aside, property tax changes may also impact you at tax time; stick to one of the top online tax services to be sure your deductions are recorded properly.

Can you repay a mortgage in lump sum?

You can speak to your lender about repaying the deficit in lump sum. This will avoid future monthly mortgage payment hikes while getting you back on the right track. It can also help you manage and monitor your future payments – especially when it comes to escrow analysis. As always, ask your lender for detailed monthly or quarterly reports. This, too, is a great way to stay on track and avoid future problems.

What to do if your mortgage premium has increased?

Double check if your premium has increased. If you see that anything has changed plus/minus, you will want to call your servicer and ask for an escrow analysis. Should you be short then you know your mortgage payment will increase and this will then cover your shortage.

What is an escrow account?

Let’s start with a quick refresher, an escrow account is an account held with your servicer that holds the funds needed to pay your property taxes and homeowners insurance. An escrow account is set up at the time of your purchase and/or refinance. It is in your prepaid items (closing costs) on your loan.

What is escrow deficiency?

An escrow deficiency is when there is a negative balance in your escrow account. This happens when the investor/bank has had to advance funds in order to cover the disbursements. When this happens you will either have to pay the amount you are negative to bring to current or will have to divide your negative amount into a year and make a monthly payment in addition to your existing new escrow payment. For example; escrow payment $300/mo, negative balance $800, 800 divided by 12 = 66.67, so now your new escrow payment will be $366.67. Note: If the deficiency is less than one month’s escrow payment, you will have 30 days to repay the amount. If the amount exceeds one month’s escrow payment, you have 12 months to repay it.

Why is there an escrow shortage when buying a new home?

This can at many times cause an escrow shortage because the taxes used were estimated and typically are underestimated.

How long do you have to pay escrow if you have a property?

If the amount exceeds one month’s escrow payment, you have 12 months to repay it. Again, the key to preventing escrow shortage and/or deficiencies is to keep an eye out for your property tax assessment, as well as your homeowner’s insurance.

What happens if you adjust your mortgage?

If there is an increase in your taxes and/or insurance then you can end up with an escrow shortage.

How to repay escrow shortage?

Pay an amount that you can comfortably afford that meets the lender's minimum requirement. If you choose to repay the escrow shortage in one lump-sum payment, ensure that you are not dipping into essential reserves that might keep you from making your regular mortgage and escrow payments. Also, if you are making a one-time credit card payment ...

Why do banks have escrow accounts?

Escrow accounts are set up to collect funds for taxes and insurance premiums on property securing a loan. They protect the bank's interest in the property and safeguard the property owner against tax liens and insurance lapses. Your lender will increase the minimum escrow balance requirement if these expenses increase, resulting in a negative balance. Low or missed escrow payments can also cause an escrow deficit. You pay a negative escrow balance in lump sum or through higher escrow installments.

How long does escrow need to be?

Lenders usually require a reserve amount of no more than two months of these payments to ensure that the escrow funds can cover unexpected increases or missed escrow payments. If the actual annual tax bill or insurance premium exceeds the amount available in your escrow account, the lender may chip in to cover the bills.

How much down payment do you need for escrow?

In general, loans made with less than a 20 percent down payment require an escrow account for at least the first few years of the mortgage to ensure that property taxes and homeowners' insurance payments are made on time.

Can you make a one time payment for escrow shortage?

If you prefer to keep your monthly mortgage the same, including regular escrow payments, you can make a one-time payment for the full escrow shortage. You might have the option of repaying only a portion of the negative balance in lump sum and making monthly installments for the remainder of the escrow shortfall.

Does Aurora Financial Group add escrow to monthly payments?

Repayment Options. The lender may add an escrow shortage to your monthly housing payment until it is fully repaid. For example, Aurora Financial Group automatically spreads the negative balance over a 12-month period.

Can escrow be negative?

Your lender will increase the minimum escrow balance requirement if these expenses increase, resulting in a negative balance. Low or missed escrow payments can also cause an escrow deficit. You pay a negative escrow balance in lump sum or through higher escrow installments.