The following are the different types of risk in insurance:

- #1 – Pure Risk.

- #2 – Speculative Risk.

- #3 – Financial Risk.

- #4 – Non-Financial Risk.

- #5 – Particular Risk.

- #6 – Fundamental Risk.

- #7 – Static Risk.

- #8 – Dynamic Risk.

Which type of risk is most likely to be insurable?

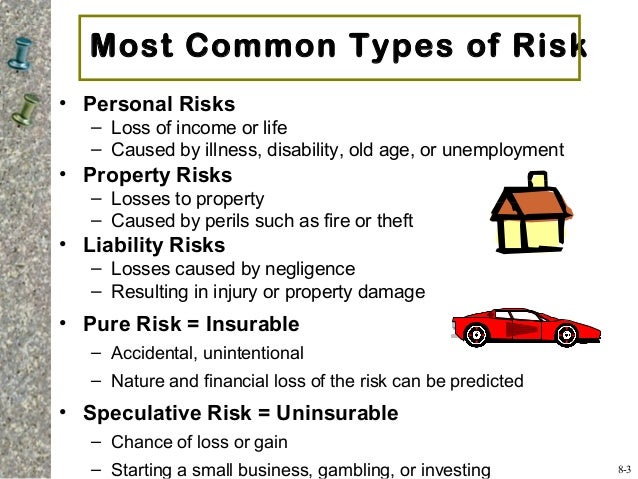

Nov 15, 2021 · The three types of risk are: Personal risk – Loss of income or life due to. illness, disability, old age, or unemployment. Property risk – Losses to property caused by. perils, i.e. fire, theft, hazards. Liability risk – Losses caused by negligence that.

What are some examples of Uninsurable risks?

Feb 22, 2020 · Insurable Types of Risk There are generally 3 types of risk that can be covered by insurance: personal risk, property risk, and liability risk. Personal risk is any risk that can affect the health or safety of an individual, such as being injured by an accident or suffering from an illness. Click to see full answer.

What's an example of an insurable risk?

Apr 17, 2022 · Insurable risks have previous statistics which are used as a basis for estimating the premium. It holds out the prospect of loss but not gain. The risks can be forecast and measured e.g. motor insurance, marine insurance, life insurance etc.

What is the difference between insurable and uninsurable risk?

What are the kinds of insurable risks? 1) Personal risks – life or health risks 2) Property risks – loss or damage to property 3) Liability risks – involve liability of the insured for an injury caused to the person or property of another

What are the insurable risks?

Insurable risks are risks that insurance companies will cover. These include a wide range of losses, including those from fire, theft, or lawsuits. When you buy commercial insurance, you pay premiums to your insurance company. In return, the company agrees to pay you in the event you suffer a covered loss.

Which of the following type of risk is insurable?

Pure risk is the only type of risk that is insurable because there is only the chance of loss. The Law of Large Numbers allows the probability of loss to become more predictable.

What are the characteristics of insurable risk?

Characteristics of insurable risksLarge number of similar exposure units. ... Definite Loss. ... Accidental Loss. ... Large Loss. ... Affordable Premium. ... Calculable Loss. ... Limited risk of catastrophically large losses.

What is risk and type of risk in insurance?

3 Types of Risk in Insurance are Financial and Non-Financial Risks, Pure and Speculative Risks, and Fundamental and Particular Risks. Financial risks can be measured in monetary terms. Pure risks are a loss only or at best a break-even situation. Fundamental risks are the risks mostly emanating from nature.

What are non-insurable risks?

Non-insurable risks are risks which insurance companies cannot insure because the potential losses or claims cannot be calculated. Thus, a potential loss cannot be calculated so a premium cannot be established. A non-insurable risk is also known as an uninsurable risk.

What are the essential requirements of a insurable risk?

Characteristics of an Ideally Insurable RiskThere must be a large number of exposure units.The loss must be accidental and unintentional.The loss must be determinable and measurable.The loss should not be catastrophic.The chance of loss must be calculable.The premium must be economically feasible.

What are the components of risk?

There are at least five crucial components that must be considered when creating a risk management framework. They include risk identification; risk measurement and assessment; risk mitigation; risk reporting and monitoring; and risk governance.

What are the elements of risk?

Given this clarification, a more complete definition is: "Risk consists of three parts: an uncertain situation, the likelihood of occurrence of the situation, and the effect (positive or negative) that the occurrence would have on project success."Aug 13, 2014

What are the essential elements of insurance contract?

In general, an insurance contract must meet four conditions in order to be legally valid: it must be for a legal purpose; the parties must have a legal capacity to contract; there must be evidence of a meeting of minds between the insurer and the insured; and there must be a payment or consideration.

What are the 4 types of risk?

The main four types of risk are:strategic risk - eg a competitor coming on to the market.compliance and regulatory risk - eg introduction of new rules or legislation.financial risk - eg interest rate rise on your business loan or a non-paying customer.operational risk - eg the breakdown or theft of key equipment.

What are different types of risks?

Within these two types, there are certain specific types of risk, which every investor must know.Credit Risk (also known as Default Risk) ... Country Risk. ... Political Risk. ... Reinvestment Risk. ... Interest Rate Risk. ... Foreign Exchange Risk. ... Inflationary Risk. ... Market Risk.Apr 2, 2012

What are the two major types of risk?

Every saving and investment action involves different risks and returns. In general, financial theory classifies investment risks affecting asset values into two categories: systematic risk and unsystematic risk. Broadly speaking, investors are exposed to both systematic and unsystematic risks.

What are the different types of risk in insurance?

3 Types of Risk in Insurance are Financial and Non-Financial Risks, Pure and Speculative Risks, and Fundamental and Particular Risks. Financial risks can be measured in monetary terms. Pure risks are a loss only or at best a break-even situation. Fundamental risks are the risks mostly emanating from nature.

What is fundamental risk?

Fundamental risks are the risks mostly emanating from nature. Having dealt with the meaning of risk we shall now attempt to divert our attention to another aspect of the nature of risk which we shall call as Classification of risk.

What is non financial risk?

Non-Financial risks are the risks the outcome of which cannot be measured in monetary terms. There may be a wrong choice or a wrong decision giving rise to possible discomfort or disliking or embarrassment but not being capable of valuation in money terms. Examples can be: Choice of a car, its brand, color, etc.

What are the crimes that occur in a ship?

Burglary, housebreaking, larceny, and theft, Stranding, Sinking, Capsizing, Collision in case of a ship, including cargo loss, Machinery breakdown and deterioration of stock due to machinery breakdown, Motor accidents including death and bodily injuries, Industrial accidents, The collapse of bridges, Derailments.

What is loss of profit in a business due to fire damage?

Loss of profit of a business due to fire damage the material property. Personal injuries due to the industrial, road or other accidents resulting in medical costs, Court awards, etc. Death of a breadwinner in a family leading to corresponding financial hardship.

What are some examples of losses?

The losses can be assessed and a proper money value can be given to those losses. The common examples are: Material damage to property arising out of an event. We may consider the damage to a ship due to a cyclone or even sinking of a ship due to the cyclone.

What is damage to a motor car?

Damage to the motor car due to a road accident which may be of partial or total nature. Damage to stock or machinery etc. Theft of a property which may be a motorcycle, motor car, machinery, items of household use or even cash. Loss of profit of a business due to fire damage the material property.

What are the elements of insurable risk?

These elements are "due to chance," definiteness and measurability, statistical predictability, lack of catastrophic exposure, random selection, and large loss exposure.

What is pure risk insurance?

Insurance companies normally only indemnify against pure risks, otherwise known as event risks. A pure risk includes any uncertain situation where the opportunity for loss is present and the opportunity for financial gain is absent.

What is catastrophic risk?

For an insurance company, catastrophic risk is simply any severe loss deemed too expensive, pervasive, or unpredictable for the insurance company to reasonably cover.

What is due to chance in insurance?

An insurable risk must have the prospect of accidental loss, meaning that the loss must be the result of an unintended action and must be unexpected in its exact timing and impact. The insurance industry normally refers to this as "due to chance.".

What is speculative risk?

Speculative risks are those that might produce a profit or loss, namely business ventures or gambling transactions. Speculative risks lack the core elements of insurability and are almost never insured.

What is the proof of loss?

For a loss to be covered , the policyholder must be able to demonstrate a definite proof of loss, normally in the form of bills in a measurable amount. If the extent of the loss cannot be calculated or cannot be fully identified, then it is not insured. Without this information, an insurance company can neither produce a reasonable benefit amount or premium cost.

What is insurance game?

Insurance is a game of statistics, and insurance providers must be able to estimate how often a loss might occur and the severity of the loss. Life and health insurance providers, for example, rely on actuarial science and mortality and morbidity tables to project losses across populations.

What is risk in insurance?

There are many definitions, but for our insurance purposes, risk predominantly means two things: uncertainty arising from the possible occurrence of an event (s) and the potential for injury or damage to persons or property to which an insurance policy relates. Just like your business, insurance companies need to turn a profit in order to survive.

What is insurable risk for a startup?

When choosing an insurance program for your startup, it’s important to understand that even the most comprehensive insurance policies do not provide a guarantee that all risks associated with your business are going to be covered.

What is pure risk vs speculative risk?

Pure Risk vs. Speculative Risk. Insurance companies typically cover pure risks. Pure risks are risks that have no possibility of a positive outcome— something bad will happen or nothing at all will occur. The most common examples are key property damage risks, such as floods, fires, earthquakes, and hurricanes.

What is catastrophic risk?

In short, a catastrophic risk for an insurance company is any type of loss that is so pervasive, expensive, or unpredictable that it would not be reasonable to offer coverage for it.

What happens if an insurer cannot predict expected losses?

If an insurer cannot predict expected losses, then they cannot properly quantify potential losses. Insurers, their actuaries, really, prefer a predictable loss in order to be able to determine premiums. If a loss rate is not predictable, it’s less likely to be in that insurer’s “appetite,” meaning they won’t want to take on that type of risk. ...

When buying business insurance, do you need to be aware of the risks?

The takeaway: when you are buying business insurance, you need to be very aware of the risks to your company, the limitations of your coverage that apply, and how you manage risk that may or may not be insured.

Can a business transfer risks to an insurance company?

That said, the risks that a business can transfer to an insurance company or more appropriately, chooses to transfer, are generally those that could result in significant loss to the business. Now, let’s take a closer look at how those risks are considered and classified.

Financial and Non-Financial Risks

Pure Risk and Speculative Risks

- Pure risks are those risks where the outcome shall result in loss only or at best a break-even situation. We cannot think about a gain-gain situation. The result is always unfavorable, or maybe the same situation (as existed before the event) has remained without giving birth to a profit (or loss). As opposed to this, speculative risks are those ri...

Fundamental Risk and Particular Risks

- Now coming to the last stage of classification of risk we may consider the subject from the viewpoint of the cause of risk and its effect. We call such classifications as fundamental risks and particular risks. Fundamental risks are the risks mostly emanating from nature. These are the risks that arise from causes that are beyond the control of an individual or group of individuals. …

Frequency & Severity

- As has been indicated in the extended example above, an insurer and risk bearer no doubt we are interested in loss (event) frequency, but at the same time, we are also interested in the severity (cost) of loss. This is so because ultimately we shall have to pay a loss and our premium generation should be such that would enable us to pay all such claims insured. Therefore, a corr…

Pure Risk vs. Speculative Risk

Due to Chance

Definiteness and Measurability

Statistically Predictable

Not Catastrophic

Randomly Selected and Large Loss Exposure

- All insurance schemes operate based on the law of large numbers. This law states there must be a sufficient large number of homogeneous exposures to any specific event in order to make a reasonable prediction about the loss related to an event. A second related rule is that the number of exposure units, or policyholders, must also be large enough t...

The Bottom Line