The following closing costs should be capitalized and added to your basis, but only if you paid them (not the seller), per IRS guidelines:

- Owner’s title insurance (not lender’s)

- Transfer taxes

- Legal and escrow fees

- Survey fees

- Recording fees

- Utility installation charges (these are not typical)

- Any seller owed items you agree to pay without being reimbursed (commissions,...

- Abstract fees (abstract of title fees)

- Charges for installing utility services.

- Legal fees (including fees for the title search and preparation of the sales contract and deed)

- Recording fees.

- Surveys.

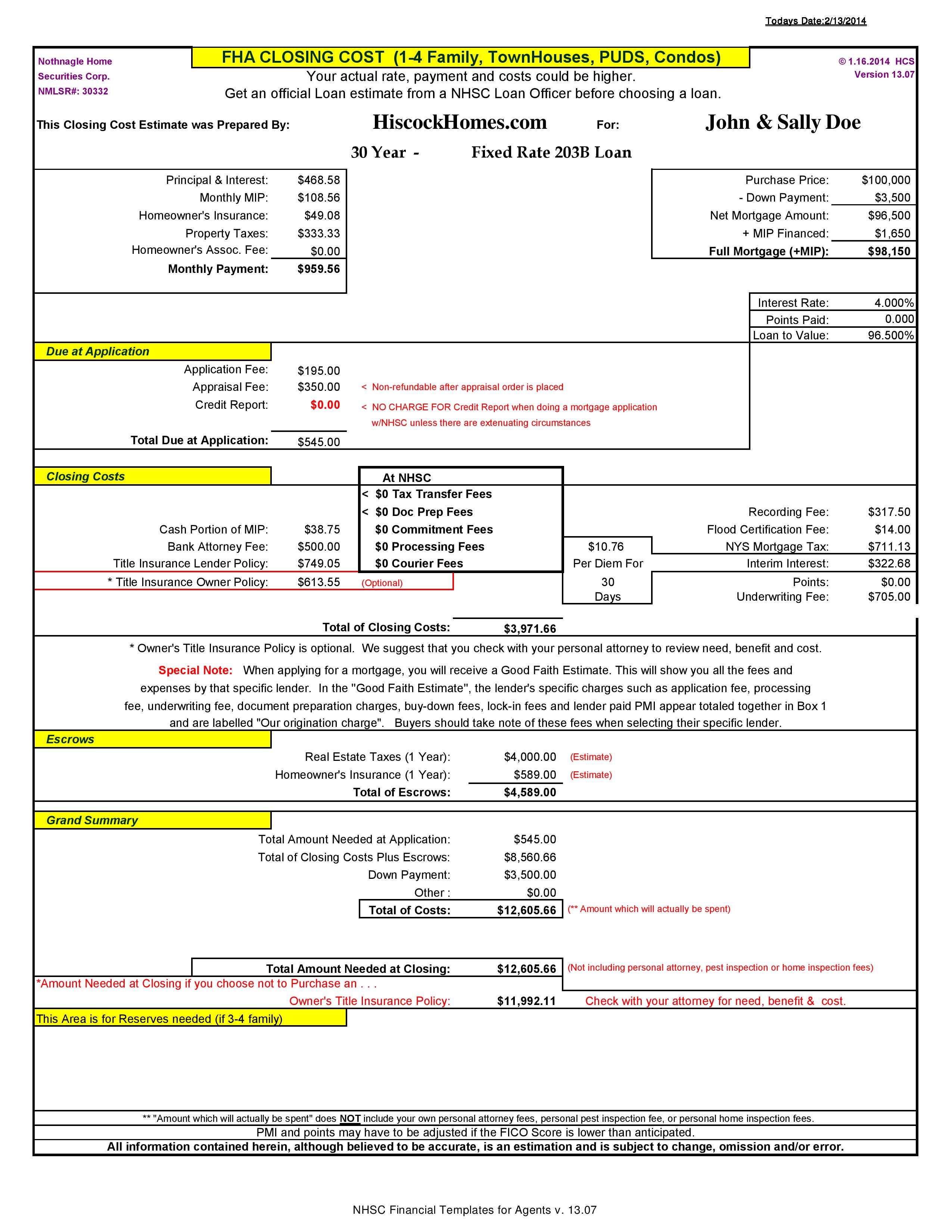

What fees are included with closing costs?

Closing costs may include fees related to the origination and underwriting of a mortgage loan, real estate commissions, taxes, and insurance premiums, as well as title and record filings. Closing costs must be disclosed in advance by law to buyers and sellers and agreed upon before a real estate deal can be completed.

How do they determine closing costs?

Method 2 Method 2 of 2: Calculating Typical Seller Closing Costs Download Article

- Calculate the real estate agent's fee, which is usually 6 to 7 percent of the sale price. ...

- Determine whether to offer a home warranty as part of your seller closing costs. ...

- Figure the amount of unpaid taxes that would be assessed on the property from the last paid bill until the closing date.

- Negotiate any other seller closing costs. ...

Are realtor fees included in closing costs?

As for who pays the closing costs, that’s where your negotiating skills (or your Realtor’s) come into play. There is no cut-and-dried rule about who—the seller or the buyer—pays the closing costs, but buyers usually cover the brunt of the costs (3% to 4% of the home’s price) compared with sellers (1% to 3%).

How do you determine closing costs?

So, if your home cost $150,000, you might pay between $3,000 and $7,500 in closing costs. On average, buyers pay roughly $3,700 in closing fees, according to a recent survey. Your lender will give you a Loan Estimate for your loan, which will include what the closing costs on your home will be, within three business days of receiving your completed loan application.

What closing costs can be added to cost basis?

The following items are some of the settle- ment fees or closing costs you can include in the basis of your property. of the sales contract and deed). agree to pay, such as back taxes or inter- est, recording or mortgage fees, charges for improvements or repairs, and sales commissions.

What costs can be added to the basis of a home?

Common improvements that might increase your cost basis include (but are not limited to) bathroom or kitchen upgrades, home additions, new roofing, the addition of a fence or desk, and various landscaping enhancements.

What part of closing costs are tax deductible?

Typically, the only closing costs that are tax deductible are payments toward mortgage interest, buying points or property taxes. Other closing costs are not. These include: Abstract fees.

Can appraisal fee be added to basis?

The remaining costs you incur to purchase a home are neither deductible nor eligible to be added to your home's basis. As far as taxes go, they are useless. These costs include all the costs you incur to obtain a home loan--for example: appraisal fees.

Can painting be added to basis of home?

Painting can be included as a selling cost, but some structural improvements may increase the cost basis used to determine if there was a gain or loss when the house was sold. If the improvements have a useful life of more than one year, then the amount of that improvement can be added to the cost basis of the house.

What is included in cost basis?

Simply put, your cost basis is what you paid for an investment, including brokerage fees, “loads,” and any other trading cost—and it can be adjusted for corporate actions such as mergers, stock splits and dividend payments.

Are appraisal fees tax deductible?

Generally, appraisal fees will be deductible on your Schedule C or Schedule E if the appraisal is conducted for business reasons. If you are buying or selling a personal property appraisal fees are not deductible.

Are closing costs capitalized or expensed?

A taxpayer may write off as deductible expenses some of the closing costs associated with the purchase of property or the acquisition of a loan. Others must be deducted proportionately over the term of the loan,so that if the loan is for 30 years,1/30 may be deducted each year.

Is PMI tax deductible 2021?

Taxpayers have been able to deduct PMI in the past, and the Consolidated Appropriations Act extended the deduction into 2020 and 2021. The deduction is subject to qualified taxpayers' AGI limits and begins phasing out at $100,000 and ends at those with an AGI of $109,000 (regardless of filing status).

Can appliances be added to basis of home?

Publication 523 also states that built-in appliances can increase the basis to the home. If you are simply replacing the washing machine or dryer during the time you live there, that installation may not count toward your basis.

Can title insurance be added to basis?

Mortgage-related items that can be added to the basis include recording fees, owner's title insurance, and more. The following are some of the settlement fees and closing costs that you can include in the original basis of your home.

What increases the basis of real property?

Increases to Basis Increase the basis of any property by all items properly added to a capital account. These include the cost of any improvements having a useful life of more than 1 year. Rehabilitation expenses also increase basis.

What is not included in cost basis?

It’s important to note that there are some commonly found amounts on settlement statements that cannot be included in your Cost Basis: Amounts placed in escrow for future payments (typically taxes and insurance) Casualty insurance premiums. Rent for occupancy of the property before closing.

What happens if you have higher starting basis?

The higher your starting basis, the closer your adjusted basis may be to your selling price on the backend, potentially decreasing the capital gain and taxes owed. The amount of taxes you’ll pay may be a deciding factor to sell the property or to re-invest.

What are legal fees?

Legal fees (including title search and preparation of the sales contract and deed). Recording fees. Surveys. Transfer taxes. Owner's title insurance. Any amounts the seller owes that you agree to pay, such as back taxes or interest, recording or mortgage fees, charges for improvements or repairs, and sales commissions.

What are points paid for refinancing?

Fees for refinancing a mortgage. Points - Points paid to obtain a loan are not included in the Cost Basis . Generally these amounts are deducted as expenses over the life of the loan. (Note that points paid for a mortgage on your primary residence are treated differently.) Assumption of mortgage - If you buy property and assume (or buy subject to) ...

Can you deduct closing costs on a settlement?

Settlement Costs - these settlement and closing costs are typically all included on your settlement ...

Can you deduct taxes paid on cost basis?

Additions to Cost Basis. Real Estate Taxes - if you pay real estate taxes that the seller owed on real estate that you purchased, and the seller did not reimburse you, the amounts are included in your Cost Basis. You cannot deduct them as taxes paid. Alternatively, if you reimburse the seller for taxes the seller paid for you, ...

What are the costs of buying a home?

The remaining costs you incur to purchase a home are neither deductible nor eligible to be added to your home's basis. As far as taxes go, they are useless. These costs include all the costs you incur to obtain a home loan--for example: 1 appraisal fees 2 mortgage broker's commissions 3 pest inspection fees 4 credit report fees 5 loan fees (not points) 6 commitment fees, and 7 in some years, mortgage insurance premiums (the law on this changes often; see Tax Deductions for Homeowners for more information).

What are the expenses to get a title to a home?

These expenses include: legal fees to obtain title to the home. title search fees.

Why does Robert agree to deduct the $4,000?

Robert agrees because he'll be able to deduct the $4,000 from his gain. Thus his gain is the same whether he pays the $4,000 or Roberta pays it. Roberta now has a home with a $504,000 basis instead of $500,000, which will reduce her profit by $4,000 when she sells her home.

What are the three categories of home purchases?

For tax purposes, these expenses fall into three categories: deductible expenses. expenses added to the home's tax basis, and. nondeductible expenses.

What expenses are included in a title search?

These expenses include: legal fees to obtain title to the home. title search fees. title insurance. title recording fees. transfer taxes, and. survey fees. You can also add to basis any expenses of the seller that you agree to pay, such as real estate broker commissions.

Can you deduct mortgage insurance premiums?

in some years, mortgage insurance premiums (the law on this changes often; see Tax Deductions for Homeowners for more information). You also can't deduct or add to your home's tax basis hazard insurance premiums, homeowners' association fees, or utility fees.

Is the cost of a home loan deductible?

The remaining costs you incur to purchase a home are neither deductible nor eligible to be added to your home's basis. As far as taxes go, they are useless. These costs include all the costs you incur to obtain a home loan--for example: appraisal fees. mortgage broker's commissions.

What is the difference between the selling price and the basis?

The difference between the selling price and the basis is your taxable profit, also known as the capital gain. The larger the gain, the more taxes that will be owed. The amount of taxes you’ll pay may be a deciding factor to sell the property or to re-invest.

What is used to reduce basis?

To the extent these amounts have been excluded from your income, they must be used to reduce your basis. Easements – any amounts you receive for granting an easement on your property are used to reduce your basis. Rebates – any rebates treated as an adjustment to the sales price at closing. Increases to Basis.

How does depreciation affect a 1031 exchange?

Once you sell the property, depreciation recapture taxes will kick in. Because of depreciation recapture, you’ll pay 25% in taxes on the entire amount of depreciation taken during the property holding period. Basically, the IRS is clawing back some of that annual depreciation benefit. Although, if you do another 1031 exchange, depreciation recapture taxes will be rolled into the acquired property. Keep in mind that once you deduct the land value, the remaining portion of the basis can be depreciated over the holding period.#N#Also, consider that the basis of any replacement property that you’re considering will be affected by the relinquished property’s improvements/depreciation . This will also affect your ability to claim depreciation going forward. Additionally, taking on additional property value in the replacement property (due to a lack of depreciable basis), will increase your basis.

Can you depreciate land on a 1031 exchange?

Although, if you do another 1031 exchange, depreciation recapture taxes will be rolled into the acquired property. Keep in mind that once you deduct the land value, the remaining portion of the basis can be depreciated over the holding period.

Does depreciation reduce basis?

Depreciation reduces your basis, creating a larger gap between your sales price and adjusted basis. Although depreciation taken over the hold period can reduce taxable income, resulting in more after-tax cash flow in your pocket, once you sell the property depreciation recapture taxes will kick in.

Can you deduct assessments for local improvements?

Do not deduct them as taxes paid.

Does adjusted basis include improvements?

But be aware that adjusted basis does not include the cost of improvements that were later removed. For example, if you built a deck on your property 15 years ago and then replaced it with a pool, the cost of the deck is no longer part of your home's adjusted basis.

What are closing costs?

Closing cost items you cannot add to your original cost basis include: 1 Insurance premiums for casualty (fire, hurricane, etc.) 2 Rent or utility charges for occupancy prior to closing 3 Property taxes 4 Loan and refinancing costs or fees (points, appraisal, etc.) 5 Pre-paid interest on your loan (s) 6 Lender’s title insurance 7 Amounts placed in escrow to cover future expenses

Why do capital expenses increase the cost basis?

Capital expenses increase your cost basis because they are considered long-term improvements that have become integral parts of the property. For example, if you spent $20,000 on a new master bathroom, you’ll simply add this amount to the $254,500 basis to arrive at an adjusted cost basis of $274,500.

What is pre-paid interest?

Pre-paid interest on your loan (s) Lender’s title insurance. Amounts placed in escrow to cover future expenses. The first three items on this list can be deducted as normal expenses for the year in which you acquired the property. Loan costs are not deducted but are instead amortized over the expected life of the loan.

What are utility installation charges?

Utility installation charges (these are not typical) Any seller owed items you agree to pay without being reimbursed (commissions, taxes, interest, improvements, etc.) Add costs associated with all items listed above to your original $250,000 purchase price to arrive at your original cost basis.

Does land depreciate?

Land doesn’t depreciate and some portion of your $250,000 purchase price must be allocated to land value. Assuming you did your bathroom renovation and rent preparation work in the same calendar year that you acquired the property, you can start with your $275,300 adjusted basis number.

Can closing costs be added to original cost basis?

Closing cost items you cannot add to your original cost basis include: Insurance premiums for casualty (fire, hurricane, etc.) Loan and refinancing costs or fees (points, appraisal, etc.) The first three items on this list can be deducted as normal expenses for the year in which you acquired the property.

Do you capitalize the preparation costs of a rental property?

If your rental property was not immediately placed into service after purchase, meaning it wasn’t already occupied or at least ready to be occupied by a tenant, you’ll also capitalize these preparation costs by adding them to your adjusted basis.

What is basis in property?

Basis is the amount of your investment in prop-erty for tax purposes. Use the basis of property to figure depreciation, amortization, depletion, and casualty losses. Also use it to figure gain or loss on the sale or other disposition of property. You must keep accurate records of all items that affect the basis of property so you can make these computations.

How to reduce the adjusted basis of a MACRS asset?

If you sell a portion of MACRS property MACRS asset), you must reduce the adjusted basis of the asset by the adjusted basis of the portion sold. Use your records to determine which portion of the asset was sold, the date the asset was placed in service, the unadjusted basis of the portion sold, and its adjusted basis. See the partial disposition rules in Regulations section 1.168(i)-8 for more detail. The adjusted basis of the portion sold is used to determine the gain or loss realized on the sale. Also see Pub. 544.

What is the basis of a property transfer?

The basis of property transferred to you or transferred in trust for your benefit by your spouse (or former spouse if the transfer is inci-dent to divorce) is the same as your spouse's adjusted basis . However, adjust your basis for any gain recognized by your spouse or former spouse on property transferred in trust. This rule applies only to a transfer of property in trust in which the liabilities assumed, plus the liabili-ties to which the property is subject, are more than the adjusted basis of the property transfer-red.

What is taxable exchange?

taxable exchange is one in which the gain is taxable or the loss is deductible. A taxable gain or deductible loss is also known as a recog-nized gain or loss. If you receive property in ex-change for other property in a taxable ex-change, the basis of property you receive is usually its FMV at the time of the exchange. A taxable exchange occurs when you receive cash or property not similar or related in use to the property exchanged.

What happens when you buy multiple assets?

If you buy multiple assets for a lump sum, you and the seller may agree to a specific allocation of the purchase price among the assets in the sales contract. If this allocation is based on the value of each asset and you and the seller have adverse tax interests, the allocation generally will be accepted. However, see Trade or Busi-ness Acquired next.

What is an intangible asset?

Intangible assets include goodwill , patents, copyrights , trademarks , trade names, and franchises. The basis of an intangible asset is usually the cost to buy or create it. If you ac-quire multiple assets, for example, an ongoing business for a lump sum, see Allocating the Ba-sis, later, to figure the basis of the individual as-sets. The basis of certain intangibles can be amortized. See chapter 8 of Pub. 535 for infor-mation on the amortization of these costs.

Can you include a canceled debt in your gross in-come?

If a debt you owe is canceled or forgiven, other than as a gift or bequest, you generally must in-clude the canceled amount in your gross in-come for tax purposes. A debt includes any in-debtedness for which you're liable or which attaches to property you hold.You can exclude canceled debt from in-come in the following situations.

What Is Cost Basis In Real Estate?

Cost basis is essentially defined as the amount that your property is worth from the standpoint of taxation. Upon the sale of a piece of real estate (for example, your single-family home residence) profit or loss is calculated by taking the property’s sales price and subtracting it from your cost basis on the date of sale.

What Can Be Included In The Cost Basis Of A Property?

According to accounting pros, it’s important to consider your cost basis and how it’s computed as you contemplate a potential sale of your property and how much money you might receive from it. Your cost basis typically includes:

How Cost Basis Changes

Numerous factors – like how you received or purchased a piece of property, whether or not the real estate was gifted, etc. – can impact your cost basis over time.

The Bottom Line

Cost basis is important because it serves as a starting point (or endpoint in the case of your adjusted basis) for determining any profits (aka capital gains) or losses on the sale of real estate assets. Capital gains tax must be paid on these gains unless steps have been taken to make them subject to exemption.

What expenses are included in a home purchase?

You add to the cost of your home expenses that you paid in connection with the purchase, including attorney’s fees, abstract fees, owner’s title insurance, recording fees and transfer taxes.

What is the exclusion amount for selling a home?

The law allows an exclusion from income for all or part of the gain realized on the sale of your home. The general exclusion limit is $250,000 ($500,000 for married taxpayers). You may feel the exclusion amount makes keeping track of the basis relatively unimportant.

How to prove your basis?

To prove the amount of your basis, keep accurate records of your purchase price, closing costs, and other expenses that increase your basis. Save receipts and other records for improvements and additions you make to the home. When you eventually sell, your basis will establish the amount of your gain. Keep the supporting documentation ...

What is the basis of a house?

Start with the purchase price. The main element in your home’s basis is the purchase price. This includes your down payment and any debt, such as a mortgage. It also includes certain settlement or closing costs. If you had your house built on land you own, your basis is the cost of the land plus certain costs to complete the house.

When will the housing market be in Central Texas in 2021?

May 6, 2021. If you live in Central Texas, you know how wild the housing market has been so far in 2021. This is similar to what is going on in the housing market in many parts of the country this spring. If you’re buying or selling a home, you should know how to determine your “basis.”.

Can you deduct mortgage interest on your taxes?

You can claim an itemized deduction on your tax return for real estate taxes and home mortgage interest. Most other home ownership costs can’ t be deducted currently. However, these costs may increase your home’s “basis” (your cost for tax purposes). And a higher basis can save taxes when you sell.

Can you add driveway paving to your basis?

Driveway paving. Home expenses that don’t add much to the value or the property’s life are considered repairs, not improvements. Therefore, you can’t add them to the property’s basis. Repairs include painting, fixing gutters, repairing leaks and replacing broken windows.