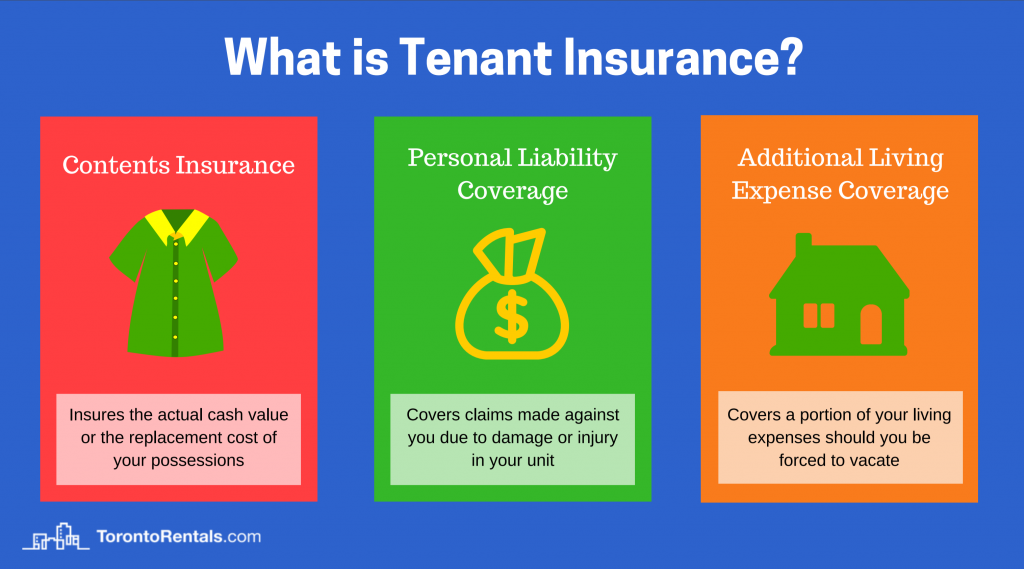

What does renters insurance cover?

- Personal property. A key part of renters insurance is that it protects your personal property. ...

- Personal liability coverage and medical expenses. Renters insurance covers personal liability coverage. ...

- Loss of use coverage. ...

- Additional living expenses. ...

How should I insure my rental property?

- Property protection: Typically the calculated replacement cost or cash value

- General liability: Usually two to four times the property coverage limit to protect against things like personal injuries

- Personal property: Usually a nominal value to cover things like appliances or landlord equipment stored on-site

What does renters insurance cover and how does it work?

- Loss of use insurance covers the living expenses you incur if your rental home becomes uninhabitable.

- Loss of use insurance is temporary and only certain types of loss are covered.

- Similarly, only certain expenses are covered under loss of use.

- This type of insurance coverage generally has an end date, meaning it is only a temporary solution.

Do I need homeowners insurance for a rental property?

You only need rental property insurance if you have tenants who you rent out your home to on a long-term or full-time basis, like for months or years. Normal homeowners insurance excludes coverage for business property, and a rental property would technically fall under that category since you make an income off of it.

What is the average cost of rental property insurance?

To understand these differences, we gathered data on the average cost for renters insurance in each state. Depending on the state you live in, the average cost of renters insurance can vary between $12 and $37 per month (or $139 to $442 per year).

What are the three things covered by renters insurance?

Renters insurance typically includes three types of coverage: Personal property, liability and additional living expenses.

What are some of the things that property insurance covers?

Standard Homeowners Insurance Coverage. A standard homeowners insurance policy provides coverage to repair or replace your home and its contents in the event of damage. That usually includes damage resulting from fire, smoke, theft or vandalism, or damage caused by a weather event such as lightning, wind, or hail.

What are 3 things that renters insurance typically does not cover?

Renters insurance does not cover:Floods.Earthquakes.Sinkholes.Bed bugs and other pests.Damage to your car.Your roommate's possessions.

What is not covered by property insurance?

Many things that aren't covered under your standard policy typically result from neglect and a failure to properly maintain the property. Termites and insect damage, bird or rodent damage, rust, rot, mold, and general wear and tear are not covered.

What are the six categories typically covered by homeowners insurance?

Generally, a homeowners insurance policy includes at least six different coverage parts. The names of the parts may vary by insurance company, but they typically are referred to as Dwelling, Other Structures, Personal Property, Loss of Use, Personal Liability and Medical Payments coverages.

Does insurance cover water damage?

Water damage to your property is usually covered as a standard feature in your buildings insurance policy. Often referred to as 'escape of water' by insurers, it can be caused by several issues, from burst pipes due to freezing temperatures, to a leaking dishwasher or an overflowing blocked toilet.

What are 5 things you should know about renters insurance?

What renters insurance will coverTheft and disasters. This is the thing that most people are concerned with. ... Your expensive collection. ... Accidents that are your fault. ... Hotel stays during repairs. ... Incidents that happen when you're not home. ... Floods and earthquakes. ... Pests. ... Your car.More items...

Which of the following would typically not be covered under renter's insurance?

For example, fire, theft, wind, hail, lightning and even volcanic eruption are typically covered. However, renters insurance does not cover floods, earthquakes, sinkholes or other earth movements. Instead, you have to purchase separate or additional coverage to protect your belongings from these threats.

Does renters insurance cover accidental damage?

Renters insurance only covers damage to the policyholder's personal property and damage they accidentally cause to someone else's property, including a house or belongings. To be covered, the property damage must have been caused by a covered peril.

What are the 7 basic types of coverage needed?

Best Covid-19 Travel Insurance PlansLife Insurance. There are a wide variety of life insurance policies. ... Disability Insurance. ... Long-Term Care Insurance. ... Homeowners And Renters Insurance. ... Liability Insurance. ... Automobile Insurance.

What are typical exclusions in an insurance policy?

Lightning, fire, and theft are all examples of perils are found under the exclusions section of every standard homeowners insurance policy. This means if your house or another structure on your property is damaged due to any of the following, your home insurance company won't cover the cost of repairs.

Which area is not protected by the most homeowners insurance?

The main areas that are not covered by homeowners insurance include:Damage caused by earth movements such as sinkholes and earthquakes.Issues caused by neglect or improper maintenance of the property.Damage caused by termites and other insects.

1. Rental Property Insurance: How It Works

Landlord insurance covers many of the same things as your regular home insurance but offers further protections since tenants will be occupying your property. Typical policies cover the property, rental income and liability.

2. How Much is Rental Property Insurance?

Rental property insurance costs are in the range of 15-25% more than your average homeowner’s insurance. If the average cost of home insurance in the USA is $1585/year, you can anticipate paying between $1,823 and $1,982/year for rental property insurance.

Our Final Thoughts: Rental Property insurance

If you’re a landlord or intend to rent out a property you own, rental property insurance is essential. Landlord insurance protects not only your property, but also those who live in and visit it. With different tiers of policies and endorsements available, you can be certain that you can find an insurance quote that works within your budget.

Renters Insurance Replacement Cost

A renters insurance replacement cost policy provides extra compensation if you file a claim for stolen or damaged personal possessions. Specifically, it enables you to replace your old items with new equivalents, rather than compensating you for your items’ depreciated value, which generally won’t provide enough money to replace them outright.

Why You Can Trust Us: 15 Renters Insurance Companies Researched

At U.S. News & World Report, we rank the Best Hospitals, Best Colleges, and Best Cars to guide readers through some of life’s most complicated decisions. Our 360 Reviews team draws on this same unbiased approach to rate the products that you use every day.

What is rental property insurance?

Rental property insurance – more commonly referred to as landlord insurance – protects non-owner-occupied commercial and residential rental properties. To qualify for a landlord insurance policy, the owner must live offsite. A landlord policy can cover a building rented to commercial tenants or to families and individuals.

What type of insurance do I need for a commercial rental property?

To protect your assets, your property and its tenants, you need adequate rental property insurance. This type of coverage can offer more than property protection.

How to protect personal property?

To protect personal property, a landlord needs to add an endorsement to the rental property insurance policy. When determining the amount of personal property coverage, calculate how much it will cost to replace the items you want to cover.

What is landlord insurance?

A landlord policy can cover a building rented to commercial tenants or to families and individuals. Residential properties covered by a landlord insurance policy can include an apartment complex, condo, house or vacation property. These flexible policies can provide different levels of property and liability protection.

How to maintain consistent rental income?

Maintaining a consistent rental income means making smart business decisions. To cut back on costs, consider raising your landlord insurance deductible to lower your premium. Take advantage of multi-policy and bundling discounts by purchasing your auto, homeowners and landlord policies from the same carrier.

How long can you rent a house with home insurance?

If you rent your home to a tenant for 62 days per year or less , you can add short-term rental coverage to your existing home insurance policy. Your homeowners insurance will protect your home’s structure at any time and cover your personal belongings while you’re occupying the residence.

What is equipment breakdown coverage?

Equipment breakdown coverage can help a landlord repair or replace damaged equipment.

What is rental property insurance?

Our rental property insurance policies include dwelling coverage, landlords’ personal property coverage, liability coverage, and loss of rent coverage. This type of insurance is especially important if you rent out a vacation home or other investment property. You never know what types of risks you may face when you decide to become a landlord.

What is landlord insurance?

Having this protection in place can shield you from liability and costly damages. Various factors can also affect the cost of this policy. Here is a close analysis of these two types of coverage and of other types of incidents that rental property insurance covers.

What is loss of rent insurance?

Loss Of Rent Coverage. Loss of rent coverage can help you by reimbursing you for any lost rent if this loss occurs as a result of a covered claim. This type of coverage may be especially beneficial in the event that your rental property becomes damaged or destroyed because of a storm, fire, or any other similar natural disaster ...

What is dwelling coverage?

Dwelling Coverage. This form of coverage protects you against physical loss (accidental or intentional) to your rental unit and all personal property found inside of it. Should your property’s physical structure become damaged as a result of a hazard that is covered by your insurance, your policy can help pay for certain reconstruction costs. ...

How to avoid personal property claims?

One effective way to avoid filing personal property claims is to keep your rental unit clean and organized. Objects such as a bicycle or a Blu-ray player in the dwelling unit you decide to rent out are typically not covered under personal property policies.

Does insurance affect credit score?

An insurance quote does not impact your credit score . When you become the owner of a rental property, you want to make sure that you are adequately protected from certain risks. If any type of event or accident befalls you and your property, you will want to minimize your financial losses. Fortunately, an effective form ...

Can you get rent insurance if you refuse to pay rent?

Loss of rent coverage typically can’t repay you if your tenant refuses to pay rent for any reason.

What Rental Property Insurance Covers

Insurance for rental property, whether it is a condo rental insurance policy or a single-family home rental property insurance policy, covers some familiar ground: liability coverage for any medical expenses from injuries occurring in the rental property, dwelling coverage in the case of perils that could cause property damage, and coverage for your own personal belongings that are stored on the premises..

What Are the Different Types of Rental Property Insurance?

Most forms of rental property insurance fall under one of three types, known as a Dwelling Policy 1, 2, or 3. These policies offer different types and levels of coverage, particularly when it relates to the kinds of disasters and perils that could trigger a claim, but each can provide unique benefits for a property owner.

Special Additions for Rental Property Insurance

Depending on the insurance provider or insurance company you choose to work with, you may have access to additional coverage in your standard policy. You also may be able to request additional coverage or receive special discounts on your insurance for rental property. Here are some of the available coverages:

The Differences Between Homeowners Insurance and Rental Property Insurance

Homeowners insurance and rental property insurance coverage can vary in several ways, but there are two main differences to be aware of.

Average Cost of Rental Property Insuranc e

While the price can vary, many rental property insurance policies cost 15-25% more than a homeowners policy for a similar property. The Insurance Information Institute reported the average cost for homeowners insurance in 2018 was $1,249. With this number in mind, rental property insurance is likely to cost between $1,436 and $1,561 on average.

Rental Property Insurance FAQs

Costs vary, but for the average rental property in the United States, rental insurance may cost between $1,436 and $1,561 based on data from the Insurance Information Institute .

What does landlord insurance cover?

A landlord policy covers the rental property itself as well as certain types of personal property if it's damaged or stolen. Landlord insurance also covers legal or medical fees if someone gets hurt on your rental property.

What is the difference between landlord and homeowners insurance?

The main difference between the two is that homeowners insurance is designed for people who live in their residence, and landlord insurance is catered towards those who rent out their homes for long periods of time. If you have a rental property that you rent out long term , you’ll need to get a landlord insurance policy.

What is loss of income insurance?

Loss of income insurance. Landlord insurance may reimburse you for loss of income if your rental property becomes temporarily uninhabitable due to a covered loss, like fire damage. This coverage only protects you for a certain amount of time, depending on your policy limits and how long it takes to rebuild or repair your rental property.

What happens if you rent out your home?

Owning a home comes with a certain amount of risk, and if you rent it out, you’re potentially piling on even more risk. Tenants could damage your personal property, or someone could get injured while on the property and you’d be liable. Like homeowners insurance, landlord insurance is designed to financially protect you ...

What happens if a tenant falls down the stairs?

For example, if your tenant slips and falls down the stairs, and a court rules that your stairwell was not up to code, your landlord liability coverage could help pay for a lawyer. If your tenant breaks their leg, liability coverage can help reimburse their medical expenses.

What is property protection?

Property protection typically includes three different types of coverage: Dwelling : Helps pay for damage to your rental property, including damage from fire, smoke, windstorm, hail, and more. Other structures : Covers damage to the detached structures on your rental property, like a detached garage.

Do you need landlord insurance for a rental property?

If you have a rental property that you rent out long term, you’ll need to get a landlord insurance policy. If the home isn’t your primary residence and you use it exclusively as a rental property, you likely won’t be covered by standard homeowners insurance.