Several factors affect the preliminary judgment about materiality and are as follows:

- 1. Materiality is a relative rather than an absolute concept.

- 2. Bases are needed for evaluating materiality.

- 3. Qualitative factors affect materiality decisions.

- 4. Expected distribution of the financial statements will affect the preliminary judgment of materiality. ...

What do you mean by preliminary materiality judgment?

This is known as preliminary materiality judgment. List and discuss two of the three main factors that affect an auditor's preliminary judgment about materiality. Answer: The three main factors that affect an auditor's judgment about materiality are: • Materiality is a relative rather than an absolute concept.

How to assess materiality in auditing?

Qualitative and Quantitative Factors of Materiality Concept When assessing the materiality, auditors usually need to consider what type of information, they are dealing with; and how much the amount is involved.

What qualitative factors might significantly affect an auditor's materiality judgment?

Identify one qualitative factor that might significantly affect an auditor's materiality judgment, and give an example of each. Answer: Qualitative factors that affect an auditor's materiality judgment include: • Amounts involving fraud.

What are the factors that affect materiality?

• Qualitative factors also affect materiality. Certain types of misstatements are likely to be more important to users than others, even if the dollar amounts are the same, such as misstatements involving frauds.

What factors affect an auditor's preliminary judgment about materiality?

Expected distribution of the financial statements will affect the preliminary judgment of materiality. If the financial statements are widely distributed to users, the preliminary judgment of materiality will probably be set lower than if the financial statements are not expected to be widely distributed.

What factors affect materiality judgment?

Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances. The size or nature of the item, or a combination of both, could be the determining factor. '

What qualitative factors may affect the preliminary materiality judgement?

Answer: Qualitative factors that affect an auditor's materiality judgment include: Amounts involving fraud. Amounts involving fraud are usually considered more important than unintentional errors of equal dollar amounts because fraud reflects on the honesty and reliability of the management or other personnel involved.

What conditions will affect the auditors determination of materiality?

The determination of materiality necessitates the company auditor to focus on various conditions factors such as projected misstatements, individual judgment, and the forecasted rules of the thumb.

What influences the materiality of the company being audited?

Judgements about materiality are made in the light of surrounding circumstances. They are affected by auditors' perceptions of the financial information needs of users of the financial statements, and by the size or nature (or both) of a misstatement. The concept of materiality is therefore fundamental to the audit.

What are the 3 types of materiality?

Table of contents#1 – Overall Materiality.#2 – Overall Performance Materiality.#3 – Specific Materiality.

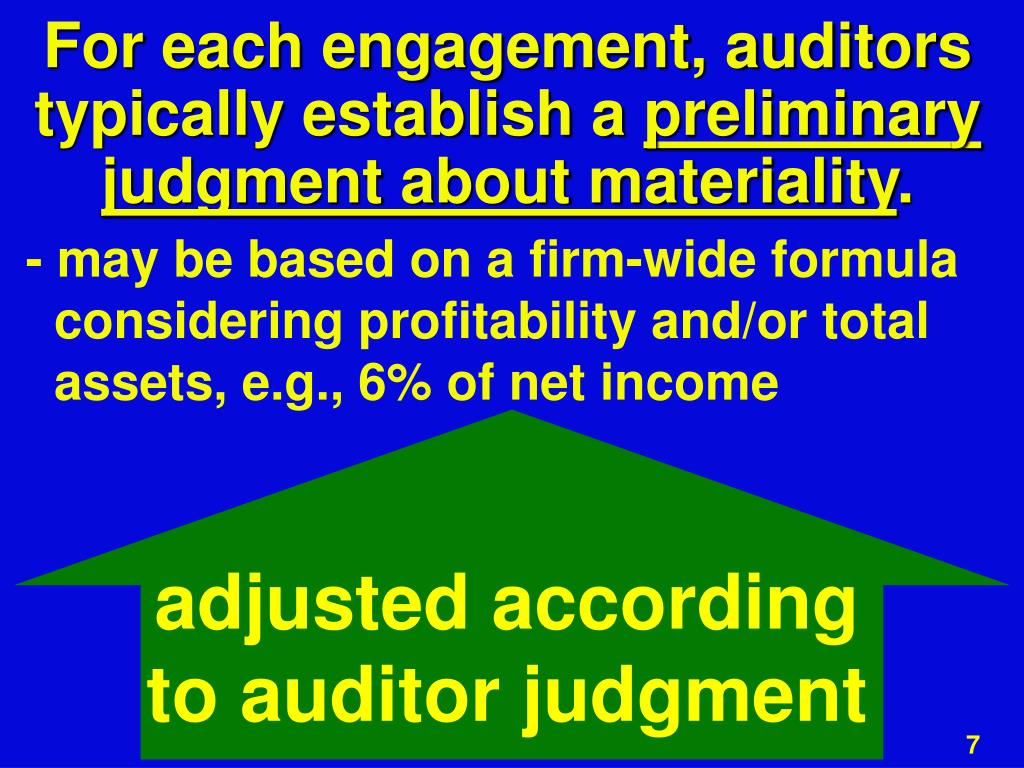

How does an auditor set the preliminary judgment of materiality?

The auditor establishes a preliminary judgment about materiality by choosing a base, or bases, which is multiplied by a percentage factor to determine the initial quantitative judgment about materiality. This amount can be adjusted for qualitative factors that may be relevant for the engagement.

When setting a preliminary judgment what is materiality?

When setting a preliminary judgment about materiality: more evidence is required for a low dollar amount than for a high dollar amount. When auditors allocate the preliminary judgment about materiality to account balances, the materiality allocated to any given account balance is referred to as: tolerable misstatement.

What are the qualitative and quantitative factors of determining materiality?

Quantitative consideration is simply about the relative size of the items in the financial statements. On the other hand, qualitative factors usually include the nature of information, the circumstance and possible cumulative effects of error or omission of such information.

What are factors to consider when determining performance materiality?

Expected total amount of factual and judgmental and projected misstatements (based on past significant misstatements and other factors). A greater number of misstatements. A lesser number of misstatements. The allowance for undetected misstatements is typically greater when more misstatements are identified.

Which characteristics would concern an auditor about the risk of material?

In risk assessment, auditors consider the following risks:Fraud risk. ... Economic, accounting risk, or other developmental risks. ... Complex transactions. ... Significant transactions with related parties. ... Degree of subjectivity in measurement.Non-routine transactions.

How does materiality affect an audit?

The materiality threshold in audits refers to the benchmark used to obtain reasonable assurance that an audit does not detect any material misstatement that can significantly impact the usability of financial statements.

What factors affect materiality?

Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances. The size or nature of the item, or a combination of both, could be the determining factor.

What is meant by setting a preliminary judgment about materiality identify the most important factors affecting the preliminary judgment?

What is meant by setting a preliminary judgment about materiality? The preliminary judgement about materiality is the maximum amount by which the auditor believes the financial statements could be misstated and still not affect the decisions of reasonable users.

Which of the following is a qualitative factor we consider when establishing materiality?

Qualitative factors to consider in the auditor's evaluation of the materiality of uncorrected misstatements, if relevant, include the following: The potential effect of the misstatement on trends, especially trends in profitability. A misstatement that changes a loss into income or vice versa.

How does an auditor set the preliminary judgment of materiality?

The auditor establishes a preliminary judgment about materiality by choosing a base, or bases, which is multiplied by a percentage factor to determine the initial quantitative judgment about materiality. This amount can be adjusted for qualitative factors that may be relevant for the engagement.

What is materiality in accounting?

Materiality has traditionally been defined through the lens of financial reporting where it involves determining the importance of the disclosure of an item of information (or its omission) to users. Prior scholarship has explored what materiality is, how it is operationalised in financial audit, and the factors influencing management, auditors' and users' judgements (Estes and Reames 1988, Blokdijk et al. 2003, Messier et al. 2005, DeZoort et al. 2006, Ng and Tan 2007, Eccles et al. 2012, Keune and Johnstone 2012. The concept has, however, persistently evaded precise codification (Power 1997b, Edgley 2014, with numerous definitions produced by professional accounting bodies, common law and statute, but none achieving complete agreement (Brennan andGray 2005, Edgley 2014). ...

What is the literature on auditing?

... The literature of auditing is focused on certain areas where it has been prove there is a relationship between audit and these issues. Thus, there are many studies which analyse the auditing from theoretical perspective to practical one, discussing the effectiveness of various audit practices (Heckman, 1979;Asare and Wright, 2001; Blokdijk et al., 2003; Nikkinene and Sahalstrom, 2004). Others many papers are dedicated to audit fees ( Davis et al., 1993;Jubb et al., 1996;Cobbin, 2002;Ireland and Lennox, 2002;Hay et al., 2006;Gonthier-Besacier and Schatt, 2007;Kealey et al., 2007;Van Caneghem, 2010). ...

What happens after the balance sheet date?

Events that occur after the balance sheet date but before the audit report is signed and dated (subsequent events) may have a material effect on the financial statements and their users . New SEC reporting requirements reduce the time between the balance sheet and report dates, limiting the availability of subsequent event evidence. Professional groups, including the Canadian Institute of Chartered Accountants (CICA) and the American Institute of Certified Public Accountants (AICPA), question whether sufficient evidence will exist if subsequent event information is not available. They fear that decreased availability of subsequent event evidence may lower the quality of both audit judgments and financial reporting. Scant prior research examines auditors' perceptions about subsequent events. Our study examines how auditors search for and discover subsequent event evidence and factors that influence this process. Responses from auditors representing all Big 4 firms and one national firm suggest that subsequent event evidence is important. Auditors generally follow procedures recommended by audit standards; however, recommended procedures uncover subsequent event evidence with low frequency. Implications for future research are discussed.

What is materiality list?

The materiality list is a subjective compilation by the auditor of unadjusted differences such as misstatements, omissions and rounding calculations that on an individual basis would not be considered material. Our survey results show that users agree with the disclosure of materiality lists and do not believe that a materiality list will expose preparers and auditors to litigation risks; users believe that a materiality list will reduce the risk of litigation, facilitate investment in stocks, reduce the cost of capital and usher in financial stability. On the other hand, we find that auditors disagree with users of financial statements with respect to disclosure and risk of litigation. In addition, we find that the perception of auditors, preparers and users is not influenced by factors such as gender and work experience. These results come from a sample set of a total of 501 survey questionnaires sent to bank, industry and accounting firms across Canada with 167 returned responses. These findings indicate a disconnect between users and the preparers and auditors of financial statements that should be fixed. That is, investors and analysts (among the users) of financial reports need to know how materiality is being defined and are not satisfied with the status quo currently defined by accounting and securities regulators. Preparers and auditors could achieve greater clarity in financial reports by articulating what it takes for a transaction to be classified as material. This materiality standard may best be accomplished by the creation of a materiality list.

What is the purpose of the social closure theory?

Research purpose: Drawing on social closure theory, the aim of this study is to develop a model to inform the flexible exercise of judgement regarding the types, extent and combinations of audit procedures implemented to gather sufficient appropriate audit evidence to respond to the assessed risks of material misstatement. Motivation for the study: The exercise of considerable judgements by auditors may mean that little consistency is achieved regarding the quantity and quality of the audit evidence obtained, especially in the public sectors of developing countries (which are often plagued by corruption), and where auditors and auditees have limited skills and experience. Research approach, design and method: The study employs a theory-building approach to develop a model intended to guide public sector auditors (following an audit risk approach), to exercise planning judgements for a class of transactions, account balance and/or disclosure. Main findings: The model clarifies the audit evidence decision-making sequences, interrelationships and contingent dependencies of the different audit procedures, and quantifies the compensatory inter-relationships between the types of audit procedures to be performed and the overall levels of assurance desired in response to the assessed risks of material misstatement. Practical and managerial implications: The model could aid public sector auditors to reduce uncertainty, ambiguity and judgement errors during their planning decision-making. Contribution or value-add: The model has been incorporated into the audit methodology of the Auditor-General of South Africa, and has been assessed for compliance with the International Standards on Auditing by the Independent Regulatory Board for Auditors in South Africa.

Why do auditors need to review materiality?

If there is any unexpected event that arises during the audit work, materiality may need to be changed so that it reflects the risks that auditors face. So, auditors may need to review overall materiality throughout the whole audit process and revise if they think it is necessary.

What are some examples of circumstances that require auditors to exercise more care when deciding materiality in audit engagements?

Examples of such circumstances include: those involving a lot of uncertainties of future events, those involved with public interest such as listed companies,

Why is misstatement not detected?

This is due to auditors cannot perform the audit tests on all the transactions and balances in the client’s accounts.

What is overall materiality?

Overall materiality is the materiality that auditors estimate and determine for the whole financial statements in the planning stage of the audit by using their professional judgment. Auditors then use this materiality in developing the overall audit strategy in order to perform the audit work in an effective and efficient manner.

What percentage of materiality is used in audit?

Auditors may use a range of the percentages and benchmarks as a basis for quantitative factors of materiality as follow: 0.5% to 1% total revenues or expenses. 1% to 2% total assets.

What is the term for the materiality of financial statements?

In the audit work, auditors must calculate materiality for financial statements as a whole, which is known as overall materiality, and performance materiality in order to use as guidance in performing the audit.

What is performance materiality?

While overall materiality is set for financial statements as a whole, performance materiality is set for particular classes of transactions, account balances, or disclosures. Auditors will need to use performance materiality throughout their audit work in the engagement in order to perform audit procedures on various transactions and balances ...

What are the factors that affect an auditor's judgment about materiality?

The three main factors that affect an auditor’s judgment about materiality are: Materiality is a relative rather than an absolute concept. A misstatement of a given size might be material for a small company, whereas the same dollar misstatement could be immaterial for a larger one. Bases are needed for evaluating materiality.

What are the factors that affect an audit firm's business risk?

Discuss three of these factors. Business risk and acceptable audit risk are affected by: The degree to which external users will rely on the statements.

What is planned detection risk?

Planned detection risk is a measure of the risk that audit evidence for an account will fail to detect misstatements exceeding a tolerable amount, should such misstatements exist. Planned detection risk determines the amount of substantive evidence that the auditor plans to accumulate.

Why do income statement misstatements have an equal effect on the balance sheet?

Most income statement misstatements have an equal effect on the balance sheet because of the double-entry bookkeeping system. Because there are fewer balance sheet accounts than income statement accounts in most audits and most audit procedures focus on balance sheet accounts, allocating materiality to balance sheet accounts is the most appropriate alternative.

What is acceptable audit risk?

Acceptable audit risk is a measure of how willing the auditor is to accept that the financial statements may be materially misstated after the audit is completed and an unqualified opinion has been issued. It is influenced primarily by the degree to which external users will rely on the statements, the likelihood that a client will have financial difficulties after the audit report is issued, and the auditor’s evaluation of management’s integrity.

How many steps are there in materiality?

Discuss each of the five steps in applying materiality in an audit, and identify the audit phase(s) in which each step is performed. List these steps in the order in which they occur.

Why is fraud more important than unintentional errors?

Amounts involving fraud are usually considered more important than unintentional errors of equal dollar amounts because fraud reflects on the honesty and reliability of the management or other personnel involved. For example, an intentional misstatement of inventory would be more important to users than a clerical error in inventory of the same amount.

Introduction

- Materiality concept in auditing referred to the concept that the information is important or significant enough to affect the decisions making of users of financial statements if such information is removed or change how it is presented. It helps auditors to focus their attention on the areas where the material errors or omission may occur. In audi...

Qualitative and Quantitative Factors of Materiality Concept

- When assessing the materiality, auditors usually need to consider what type of information, they are dealing with; and how much the amount is involved. For the materiality concept in auditing, these are usually referred to as qualitative and quantitative factors of the materiality concept. Quantitative consideration is simply about the relative size of the items in the financial statement…

Materiality Concept of Different Users

- Different users of information may have different preferences when applying the materiality concept in auditing. Hence, it is very important for accountants or auditors to define who is the primary user of financial information. For example, investors or lenders usually want the information that can help them make the decision in funding the company. These would help the…

Conclusion

- Materiality concept in auditing involves a lot of professional judgment. Hence, it is important to understand the types of information and amount involved as well as who are the primary users of particular information when exercising judgment to determine materiality.