The conforming loan limit is the dollar cap on the size of a mortgage that Freddie Mac and Fannie Mae are willing to buy or guarantee. Mortgages that meet the support requirements by the two agencies are known as conforming loans. The limit is set by the Federal Housing Finance Agency

Federal Housing Finance Agency

The Federal Housing Finance Agency is an independent federal agency created as the successor regulatory agency of the Federal Housing Finance Board, the Office of Federal Housing Enterprise Oversight, and the U.S. Department of Housing and Urban Development …

Federal Housing Finance Agency

The Federal Housing Finance Agency is an independent federal agency created as the successor regulatory agency of the Federal Housing Finance Board, the Office of Federal Housing Enterprise Oversight, and the U.S. Department of Housing and Urban Development …

What is a conforming loan limit?

Conforming loan limit is the limit on the size of a mortgage that Fannie Mae and Freddie Mac will purchase and/or guarantee.

What are conforming and nonconforming loans?

The conforming loan limits act as guidelines for the mortgages most mainstream lenders offer. In fact, some financial institutions will only deal with conforming loans that meet the agencies' criteria. Mortgages that exceed the conforming loan limit are known as nonconforming or jumbo mortgages.

What are the 2022 conforming loan limits by County?

This website provides 2022 conforming loan limits by county, as well as FHA limits. In 2022, the baseline loan limit for most counties across the U.S. will be $647,200. That’s an increase of nearly $100,000 from the 2021 cap of $548,250.

Can I get a conforming loan in Los Angeles County?

Since you’re within the limit for that county, you’d be able to get a regular, conforming loan. You’d also be able to get a conforming loan for this property in Los Angeles County, where the conforming loan limit is at the loan limit ceiling of $822,375.

What is meant by conforming limits?

Conforming loan limits are the maximum amount of cash that a homebuyer can borrow from a lender using a conventional loan. These limits are set by the FHFA every year to determine exactly how much a buyer can borrow without what's known as a Jumbo Loan.

What is the difference between a conforming and non conforming loan?

A conforming loan meets the guidelines to be sold to either Fannie Mae or Freddie Mac, two of the largest mortgage buyers in the U.S. Non-conforming loans, on the other hand, are those that fall outside those guidelines, so they can't be sold to Fannie Mae or Freddie Mac.

What does it mean when a loan is conforming?

A conforming loan is a mortgage with terms and conditions that meet the funding criteria of Fannie Mae and Freddie Mac. Conforming loans cannot exceed a certain dollar limit, which changes from year to year. In 2022, the limit is $647,200 for most parts of the U.S. but is higher in some more expensive areas.

What is conforming mortgage limit?

The baseline conforming loan limit for 2022 is $647,200 – up from $548,250 in 2021. The limit is higher in areas where the median house cost exceeds this number, so borrowers in high-cost areas can get conforming loans of up to $970,800 depending on the limit in their individual county.

What is the advantage of a conforming loan?

Conforming loans are beneficial because it helps buyers to qualify for the lowest possible interest rates and therefore lower monthly payments. Choice of lender. If a lender has the option to sell your mortgage to Fannie Mae or Freddie Mac, it's a safer investment for them.

What credit score do you need for a conforming loan?

620Conventional Loans A conventional loan is a mortgage that's not insured by a government agency. Most conventional loans are backed by mortgage companies Fannie Mae and Freddie Mac. Fannie Mae says that conventional loans typically require a minimum credit score of 620.

What is the difference between a conforming and a conventional mortgage?

A conventional loan doesn't have to be guaranteed or insured by the federal government, but it does adhere to Fannie Mae and Freddie Mac guidelines in most cases. A conforming loan, on the other hand, describes a certain set of characteristics, mainly loan amount, contained within a home loan.

What does 30-year fixed conforming mean?

Conforming loan definition A common example of a conforming loan is a mortgage with a 20 percent down payment, a 15- or 30-year term, monthly principal and interest payments, no prepayment penalty, no balloon payment and no private mortgage insurance.

Why does the conforming loan limit matter?

Traditional lenders widely prefer to work with mortgages that meet the conforming loan limits because they are insured and easier to sell. Mortgages that exceed the conforming loan limit are known as nonconforming or jumbo mortgages.

Will conforming loan limits increase in 2022?

The Federal Housing Finance Agency (FHFA) recently announced the 2022 conforming loan limits and, to no one's surprise, loan limits have increased significantly to $647,200 in most areas of the country. The 18% increase is the largest year-over-year jump in loan limits in recent history.

What is the difference between a conforming and FHA loan?

FHA loans are issued through the Federal Housing Administration, and the insurance covers the loan if you stop paying on it. A conforming loan is a conventional loan that “conforms” to the limits set by Fannie Mae and Freddie Mac.

What is the difference between jumbo and conforming loans?

Jumbo loans live up to their name by offering a limit much higher than that placed on conforming loans. While conforming loans are created for the average homebuyer, jumbo loans are designed for high-income earners looking to purchase more expensive properties.

What makes a loan non conforming?

A nonconforming mortgage is a home loan that does not adhere to government-sponsored enterprises (GSE) guidelines and, therefore, cannot be resold to agencies such as Fannie Mae or Freddie Mac. These loans often carry higher interest rates than conforming mortgages.

Do conforming loans have better interest rates?

Conforming loan pros Costs less: Because there is a larger secondary market for conforming loans, they often have lower interest rates than nonconforming loans — and that means lower monthly payments and less money spent over the life of the loan. Conforming loans also typically have lower down payment requirements.

What does 30 year fixed conforming mean?

Conforming loan definition A common example of a conforming loan is a mortgage with a 20 percent down payment, a 15- or 30-year term, monthly principal and interest payments, no prepayment penalty, no balloon payment and no private mortgage insurance.

Do nonconforming loans have higher interest rates?

The good news is that jumbo loans don't usually have higher interest rates compared to conforming conventional loans. However, jumbo loans often have stricter qualification criteria. You'll need a lower debt-to-income (DTI) ratio and a higher credit score to qualify for one.

Update: Conforming Loan Limits Increased For 2018

On November 28, 2017, the Federal Housing Finance Agency (FHFA) announced that it would raise the baseline conforming loan limit for 2018, for most...

What Is A Conforming Loan?

A conforming home loan is one that meets, or “conforms” to, certain guidelines set forth by Freddie Mac and Fannie Mae.Freddie and Fannie are the t...

‘Jumbo’ Mortgages Are Still Widely Available

Borrowers who wish to obtain a mortgage loan in an amount that exceeds the 2018 conforming limits still have options. When a home loan exceeds the...

What Is The Conforming Loan Limit?

The FHFA sets conforming loan limits for Fannie Mae and Freddie Mac, the two government-sponsored enterprises that it regulates.

What is the limit for conforming loan in Los Angeles County?

You’d also be able to get a conforming loan for this property in Los Angeles County, where the conforming loan limit is at the loan limit ceiling of $822,375.

What is the FHFA loan limit for San Bernardino County?

If you were to buy that house in San Bernardino County, which isn’t an FHFA high-cost area, you’d likely need to take out a jumbo loan, since you’d be exceeding the $548,250 baseline loan limit.

What is the limit for conforming loans in 2021?

The baseline conforming loan limit for 2021 is $548,250 – up from $510,400 in 2020. The limit is higher in areas where the median house cost exceeds this number, so borrowers in high-cost areas can get conforming loans of up to $822,375, depending on the limit in their individual county.

What are the requirements for a Freddie Mac loan?

Both Fannie Mae and Freddie Mac have additional criteria for the loans they purchase, including minimum credit scores, minimum down payments and maximum debt-to-income ratios (DTI). But in general, when people talk about conforming loan standards, they’re talking about loan limits.

Can inventory exceed high cost loan ceiling?

This is especially important to consider in high-cost areas. Even with higher loan limits, much of the local inventory could still exceed the high-cost loan ceiling.

What are conforming loan limits?

Conforming loan limits are the Fannie and Freddie limits discussed above, and these limits are not the same all over the United States; there are low-cost areas and high-cost areas which have their own limits established by Fannie and Freddie.

Why is it easier to get a conforming loan?

A conforming loan is easier to qualify for because of lower FICO score requirements and other factors; non-conforming loans, also known as Jumbo Loans are harder to financially qualify to get as they require higher down payments and higher FICO scores. Non-conforming loans carry a higher risk to the lender.

Is a FHA loan a conforming loan?

FHA home loans have limits that are set by county just like the Fannie and Freddie conforming loan limits. An FHA conforming loan would be at or under the FHA loan limit for that area. Furthermore, FHA home loan limits are influenced by the limits set by Fannie Mae and Freddie Mac. In late 2018, the Federal Housing Finance Agency (FHFA) ...

Will the Freddie loan limit increase in 2019?

In late 2018, the Federal Housing Finance Agency (FHFA) announced that Fannie and Freddie loan limits would increase in 2019 similar to the increases announced in the previous year.

Do FHA loan limits change every year?

Borrowers should know that FHA mortgage loan limits for conforming loans do not change every year, but the potential for such change is always there. ------------------------------. RELATED VIDEOS: Home Equity Can Secure Your Second Mortgage. Consider the Advantages of Discount Points.

What is the conforming loan limit for a county?

In most cases, the conforming loan limit for a particular county is set at 115% of the median home value for the area. It cannot, however, be more than 50% above the baseline mentioned at the top of this page.

What Is a Conforming Loan?

A conforming home loan is one that meets, or “conforms” to , certain guidelines set forth by Freddie Mac and Fannie Mae.

What is the maximum amount of a jumbo mortgage?

More expensive markets, such as New York City and San Francisco, have conforming loan limits as high as $822,375. Anything above these maximum amounts would be considered a “jumbo” mortgage.

What is conventional mortgage?

A “conventional” mortgage loan is one that does not receive any kind of government insurance, guarantee or backing. This distinguishes them from the government-backed home loan programs like FHA, VA and USDA.

Why did the federal housing baseline increase?

This marks the fifth year in a row that federal housing officials have raised the baseline, in order to keep up with rising home values.

Does Freddie Mac have a conforming mortgage?

But the size of the loan is one of the most important criteria, from a borrower’s perspective. Freddie Mac and Fannie Mae will only purchase loans up to a certain amount. These maximum amounts, or limits, vary by county and are updated every year.

Which states have baseline conforming limits?

The default baseline conforming limits apply to all other counties in all states, along with Puerto Rico and the islands which make up the Northern Mariana Islands (Northern Island, Saipan & Tinian).

What is the conforming loan limit for 2021?

On November 24, 2020 the Federal Housing Finance Agency (FHFA) raised the 2021 conforming loan limit on single family homes from $510,400 to $548,250 - an increase of $37,850 or 7.42%. That rate is the baseline limit for areas of the country where homes are fairly affordable.

What is the maximum amount of HECM reverse mortgage?

The HECM reverse mortgage maximum claim amount is set to $822,375, which is the 150% of the baseline conforming mortgage limit.

What is the FHFA map?

The FHFA offers an interactive map of conforming limits by county. A static version of the map is included below, followed by state-by-state tables of county-level data

Did the FOMC lower the Fed Funds Rate?

The FOMC lowered the Fed Funds Rate & yields on other Treasuries fell in the face of the COVID-19 crisis. Mortgage rates also fell sharply (reaching all time lows) dramatically lowering monthly loan payments.

What is the maximum conforming loan amount for a mortgage?

In most of the U.S., the 2021 maximum conforming loan limit (CLL) for one-unit properties will be $548,250, an increase from $510,400 in 2020.

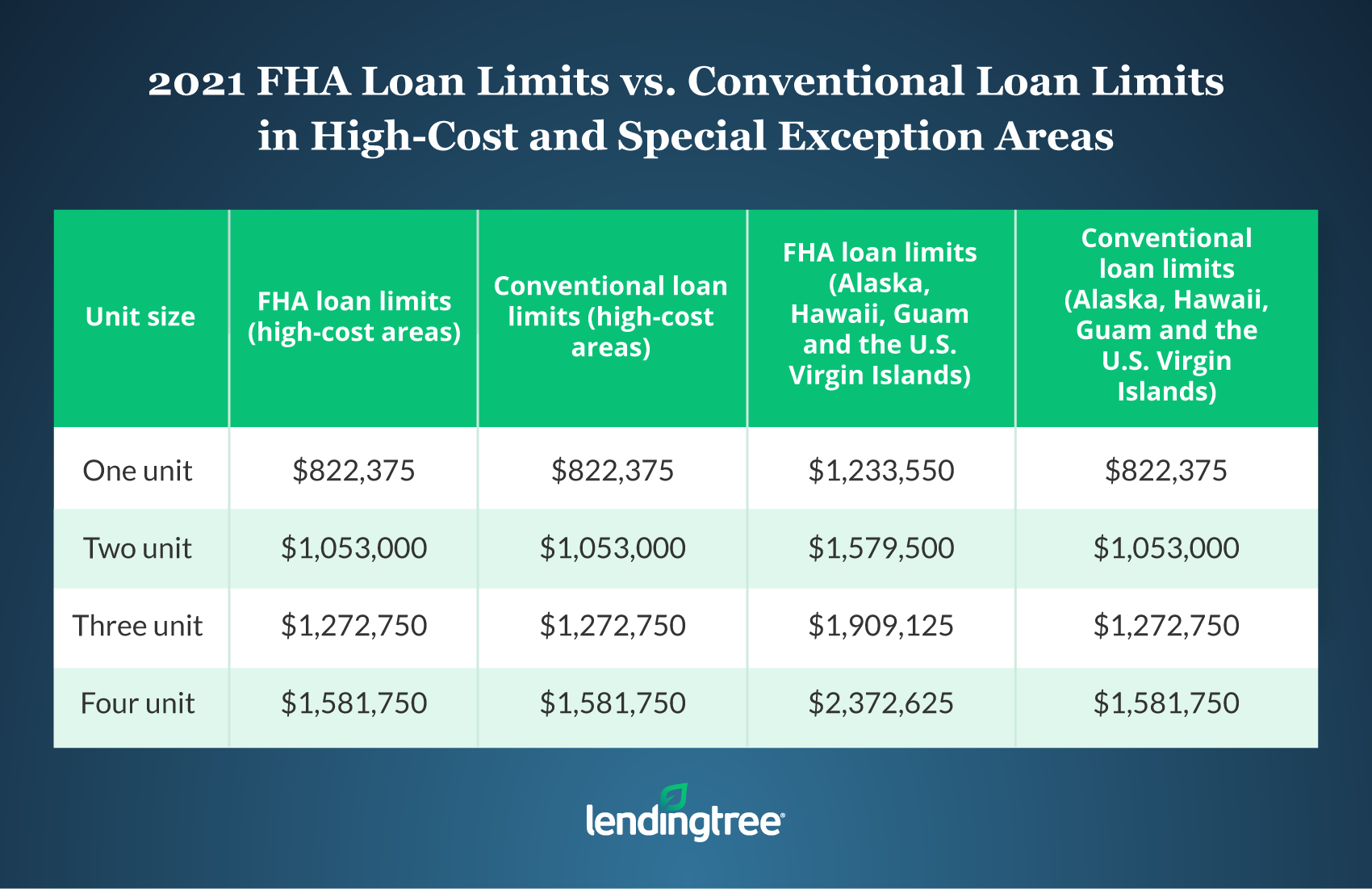

What is the new ceiling loan limit?

The new ceiling loan limit for one-unit properties in most high-cost areas will be $822,375 — or 150 percent of $548,250. Special statutory provisions establish different loan limit calculations for Alaska, Hawaii, Guam, and the U.S. Virgin Islands.

What is the minimum credit score required for a conforming loan?

Conforming loans typically require: A credit score of at least 620. A debt-to-income ratio below 43%.

Which states have the maximum conforming loan limits?

Areas such as Alameda County, California, Arlington, Virginia, and Jackson, Wyoming enjoy the maximum conforming loan limits, while cities like Seattle, Washington and Baltimore, Maryland fall between the “floor” and the “ceiling.”. In Alaska, Hawaii, Guam, and the U.S. Virgin Islands — which follow their own loan limit rules — ...

What is a mortgage loan limit?

A loan limit is the maximum amount you can borrow under certain mortgage programs.

What if my loan is over the conventional limit?

Remember that the conforming loan limit applies to the loan amount, not the home price.

What is the maximum amount of a single family loan?

And the single-family loan limit is over $822,000 in high-cost areas.

Do jumbo loans have a limit?

That means the lenders offering jumbo loans are free to set their own criteria, including loan limits.

Do Freddie and Fannie have conforming requirements?

Exact conforming loan requirements can vary by lender, but they all have to meet the minimum guidelines set by Fannie and Freddie.