What is an Audit Deficiency? A deficiency occurs when the design or operation of a control does not perform as it’s intended. There are a series of steps and considerations when evaluating an internal control deficiency.

What are significant deficiencies in auditing?

These deficiencies relate to a misstatement occurring or the likelihood of it happening in the future and its potential effects. Therefore, significant deficiencies may exist even if auditors cannot identify any deficiencies within an audit engagement.

What are control deficiencies in accounting?

Control deficiencies occur when the controls in place are insufficient or ineffective or when there is a lack of control that contributes to the problem. The entities should take the necessary measures to minimise these deficiencies. What Are Value for Money Audits and Why is It So Important to the Company?

What does significant deficiency mean in accounting?

A significant deficiency is a single weakness or a combination of weaknesses in the internal controls associated with financial reporting, that is less severe than a material control weakness and yet is sufficient to merit the scrutiny of those responsible for administering an entity's financial reporting.

What does the PCAOB say about audit deficiencies?

In other cases, the PCAOB has disclosed audit deficiencies related to roll-forward of controls tested at an interim date. The board noted instances where firms did not perform any testing or used inquiry alone for assessing the effectiveness of roll-forward procedures, despite high inherent or fraud risks associated with these controls.

What are deficiencies in auditing?

The three most common deficiencies all reflect engagement management problems affecting many areas of the audit: a failure to gather sufficient, competent evidence, lack of due care and lack of professional skepticism.

What are types of control deficiencies?

Examples of control deficiencies include:Lack of timeliness of cash deposits and account reconciliation.Lack of review and reconciliation of departmental expenditures.Lack of overdraft funds monitoring.Lack of physical inventory.

What is deficiency in financial accounting?

A deficiency is the numerical difference between the amount of tax that a taxpayer, or taxpaying entity, reports on a tax return and the amount that the Internal Revenue Service (IRS) determines is actually owed. The term only applies to shortfalls and not to surpluses.

What are internal control deficiencies?

A deficiency in internal control exists when a control does not allow management or employees to prevent, or detect and correct, misstatements on a timely basis.

What is meant by the term deficiency?

Definition of deficiency 1 : the quality or state of being defective or of lacking some necessary quality or element : the quality or state of being deficient : inadequacy suffers from a deficiency of critical thinking. 2 : an amount that is lacking or inadequate : shortage staffing deficiencies : such as.

What is the difference between significant deficiency and material weakness?

A significant deficiency is less severe than a material weakness in that it is unlikely to have a material impact on financial statements, but it is, “important enough to merit attention by those responsible for oversight of the company's financial reporting,” according to the PCAOB.

Why do you prepare a deficiency account?

A deficiency account is created to show the balance sheet or financial statement of a financially unstable enterprises or company. It usually has the values associated with the total value of the assets. It also indicates and shows the cause of the difficulty and net losses that the enterprises has.

What are the 5 internal controls in auditing?

There are five interrelated components of an internal control framework: control environment, risk assessment, control activities, information and communication, and monitoring.

What are the two main reasons for control deficiency?

A deficiency in design exists when (a) a control necessary to meet the control objective is missing or (b) an existing control is not properly designed so that, even if the control operates as designed, the control objective is not always met.

What are the 4 types of internal controls?

Preventive Controls Separation of duties. Pre-approval of actions and transactions (such as a Travel Authorization) Access controls (such as passwords and Gatorlink authentication) Physical control over assets (i.e. locks on doors or a safe for cash/checks)

What is a material deficiency?

Material Deficiency means an inadequacy or omission of an owner's or operator's risk management program that reduces the effectiveness of the risk management program.

What are the 4 types of internal controls?

Preventive Controls Separation of duties. Pre-approval of actions and transactions (such as a Travel Authorization) Access controls (such as passwords and Gatorlink authentication) Physical control over assets (i.e. locks on doors or a safe for cash/checks)

What are control weaknesses?

A control weakness is a failure in the implementation or effectiveness of internal controls. Malicious actors can leverage internal control weakness to circumvent even the most robust security measures.

What are some internal control weaknesses?

There are four major internal control weaknesses that put your data at risk:Technical Control Weaknesses. Technical security control focuses on hardware and software. ... Operational Control Weaknesses. ... Administrative Control Weaknesses. ... Architectural Control Weaknesses.

What are operational deficiencies?

Operational deficiency occurs when: A control that is well-designed doesn't work as intended, or. The person charged with performing the control is not able to do so in a manner that permits the control to operate properly.

What is audit deficiency?

Audit Deficiency means in respect of any Person, any deficiency in any written report, statement or audit provided by or on behalf of such Person under the Program Documents.

What is a significant deficiency?

Significant deficiency means a shortcoming in the system that materially affects the ability of officials of the Department of Defense to rely upon information produced by the system that is needed for management purposes.

What happens if a vendor fails to respond to a billing audit?

If Attorney or Vendor fails to respond to a Billing Audit Deficiency or fails to provide necessary documentation within a reasonable period of time, then JAC may take appropriate action including, but not limited to, rejecting the bill for payment, issuing a letter of objection to payment, or paying the amount established by law or applicable court order.

How long does it take for a vendor to respond to a billing audit?

Vendor agrees to respond to any Billing Audit Deficiency related to a due process provider billing within thirty (30) days of receipt of the Billing Audit Deficiency.

What is a deficiency claim date?

Deficiency Claim Date means, with respect to any Distribution Date, the fourth Business Day immediately preceding such Distribution Date.

What is borrowing base deficit?

Borrowing Base Deficiency means, at any date on which the same is determined, the amount, if any, that (a) the aggregate Covered Debt Amount as of such date exceeds (b) the Borrowing Base as of such date.

What is spread account deficit?

Spread Account Deficiency means the excess, if any, of the Required Spread Account Amount over the Available Spread Account Amount.

What are the common audit problems?

OTHER COMMON AUDIT PROBLEMS INCLUDE FAILURE to exercise due professional care and the appropriate level of professional skepticism, overreliance on inquiry as a form of audit evidence, deficiency in confirming accounts receivable, failure to recognize related party transactions and assuming internal controls exist when they may not.

What is the problem with audit program design?

AUDIT PROGRAM DESIGN WAS A PROBLEM CITED in 44% of the cases. Auditors failed to properly assess inherent risk and adjust the audit program according ly. The best way for a firm to remedy such deficiencies is to promote more involvement by audit firm executives—partners and managers—in planning the engagement.

How can CPAs learn to detect financial statements?

CPAs CAN LEARN HOW TO BETTER DETECT financial statement fraud by understanding the mistakes others made in cases where the SEC imposed sanctions on auditors for their association with fraudulently misstated financial statements. This article focuses on 45 SEC enforcement actions against auditors in the period 1987 to 1997.

Why should CPA firms evaluate their own quality control systems?

CPA firms should evaluate their own quality control systems to ensure policies and procedures emphasize the importance of proper audit planning, supervision and review, including timely involvement by engagement and concurring partners. Additionally, firms should reexamine existing quality control procedures to make sure they are detailed enough to assure firm leaders that audit teams are examining appropriate documentation (final documentation, not drafts) and that teams complete all audit program steps. Those procedures should emphasize that auditors should corroborate management representations with additional evidence and not overuse management inquiry as a form of audit evidence.

Why should audit firms be closely examining their performance?

Performance measurement and compensation. Audit firms can benefit from closely examining their performance measurement and compensation systems. In many of the fraud cases, it appeared auditors simply chose not to pursue identified audit issues, perhaps fearing the time spent investigating those issues would hinder career advancement or result in penalties during salary and bonus reviews because they ran overtime budgets or missed client-imposed deadlines.

How can audit planning be remedied?

Auditors can best remedy audit planning deficiencies by promoting more extensive and timely involvement by partners—both engagement and concurring—and managers in planning the engagement. Such involvement increases the likelihood the auditor will correctly assess risks (both inherent and control) and modify the firm’s audit approach (nature, extent and timing of tests) as appropriate. Involving the audit team partner and manager during the planning phase will help ensure that audit plans emphasize careful scrutiny of nonroutine transactions, particularly those recorded near yearend—when management sometimes records inappropriate transactions.

Why do auditors rely on internal controls?

In the SEC cases, auditors sometimes relied too much on internal controls by either failing to expand testing after discovering internal control weaknesses or assuming a baseline level of internal control existed even in the absence of any controls testing.

What is a deficiency in accounting?

1 A deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility (the likelihood of the event is either reasonably possible or probable as those terms are defined in the Financial Accounting Standards Board Accounting Standards Codification glossary) that a material misstatement of the governments financial statements will not be prevented, or detected and corrected on a timely basis.

How to minimize material audit adjustments?

Minimize the likelihood of material audit adjustments. Every practical step should be taken to minimize the possibility of material auditor-initiated audit adjustments. A periodic process during the year to ensure the ongoing completeness and accuracy of data [6] can aid in identifying and preparing adjustments to limit the number and dollar amounts of adjustments that result from the auditor. Further, procedures at the end of the period can also help limit auditor-initiated adjustments. For example, a government should carefully review its cutoff procedures and the method it uses to uncover unrecorded liabilities at the end of the fiscal period (items found by the auditor rather than by management could result in a significant deficiency or material weakness being reported).

What is the AICPA?

The Auditing Standards Board (ASB) of the American Institute of Certified Public Accountants (AICPA) has issued guidance on communicating matters related to a governments internal control over financial reporting identified in an audit of financial statements.

What is the responsibility of an independent auditor?

3 While this strategy will help the government to avoid, limit, or eliminate findings related to its internal control over financial reporting, ultimately, it is the independent auditors responsibility to make the judgment about what findings to report.

Why should we provide ongoing training for accounting staff?

[7] Accordingly, ongoing training should be provided to ensure that appropriate staff remains current on the authoritative guidance as it evolves. [8] Every attempt should be made to ensure that such training is provided consistently even when the government experiences fiscal stress or tough economic times.

What are the deficiencies in PCAOB?

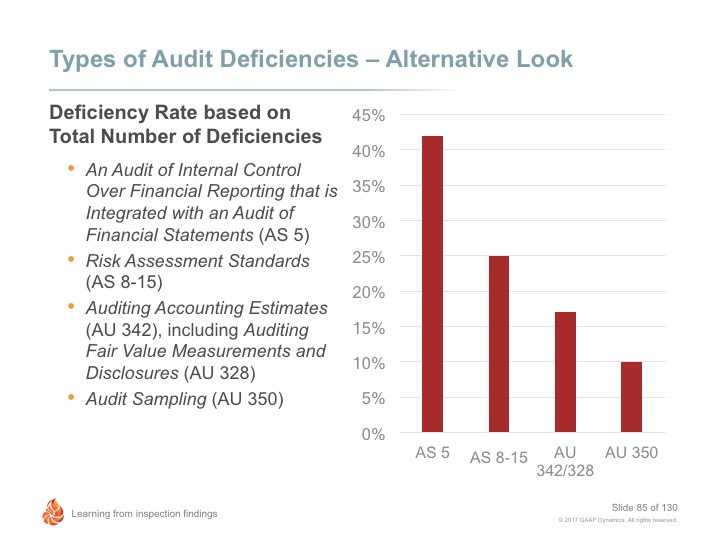

The PCAOB inspection reports document numerous deficiencies in the testing of design of controls or operating effectiveness of controls of various accounts. AS 5 and AS 12, Identifying and Assessing Risks of Material Misstatement, require auditors to first obtain an understanding of internal controls designed to prevent and detect material misstatements, which should then help them select relevant controls to test for the identified risk. AS 5 cautions that auditors cannot infer effectiveness because no misstatements were detected by substantive procedures; instead, they should obtain direct evidence about a control’s operating effectiveness. The PCAOB identified several cases where auditors did not perform important assessments. Furthermore, the PCAOB has indicated that auditors sometimes fail to test all the relevant assertions of significant accounts and disclosures (PCAOB Staff Audit Practice Alert 11).

Why should auditors use the work of competent and objective third parties in low-risk areas?

Auditors can more extensively use the work of competent and objective third parties in low-risk areas because as the risk decreases, the necessary level of competence and objectivity decreases (AS 5). On the other hand, auditors should perform more extensive testing of the work done by third parties in high-risk areas involving significant judgment and fraud risk, particularly when the competency of those third parties is judged to be low.

What is PCAOB audit?

As part of its oversight mission, the PCAOB has sought to improve the quality of U.S. public company audits. A major part of its focus has centered on auditors’ assessments of companies’ internal controls over financial reporting (ICFR), as required under the Sarbanes-Oxley Act of 2002. This article assesses whether audit quality has improved by ...

Why is IT important in internal control audits?

Many companies rely on IT, such as enterprise resource planning (ERP) systems to process accounting data— and the role of IT is even more important in internal control audits. Auditors should identify IT risks and assess general and application IT controls as an integral part of the top-down risk-based approach used in the financial statement audit. The PCAOB expects auditors to understand how IT affects a company’s flow of transactions and “obtain an understanding of specific risks to a company’s internal control over financial reporting resulting from IT” (AS 15, Audit Evidence, para B4).

How many inspection reports did the Big Four audit?

Big Four auditors as a group, which audit the vast majority of listed U.S. companies, dominated the count with 35 inspection reports (26.7%) that contained ICFR-related audit deficiencies.

Do auditors respond to PCAOB feedback?

In general, it appears that auditors were not responsive to the PCAOB’s feedback on their audits of ICFR and did not remediate observed deficiencies by the next inspection. Of the 131 inspection reports containing deficient audits related to ICFR, 16 auditors—8 annually inspected U.S. auditors and 8 foreign auditors, representing 75 inspection reports—had multiple inspection reports containing ICFR-related audit deficiencies. In comparison, 10 inspection reports with ICFR-related audit deficiencies were remediated by the next PCAOB inspections. Of the 10 subsequent reports, 6 were clean reports without any audit deficiencies and 4 contained other audit deficiencies that are not related to ICFR. No information about the outcomes of subsequent inspections was available for the remaining 46 deficient ICFR audits as of the end of the period examined (December 31, 2013). Based on the available information, it seems that auditors do not adequately address the ICFR-related audit deficiencies pointed out by the PCAOB inspections and improve the quality of subsequent audits of ICFR.

Does PCAOB test all significant accounts?

The PCAOB has indicated that auditors sometimes fail to test all the relevant assertions of significant accounts and disclosures.

What is a control deficiency?

Firstly, a control deficiency can occur when an entity’s internal controls are designed, implemented or operated in such a way that they cannot deter, identify or correct risks. In this event, the necessary controls may be in place but they may be insufficient or ineffective in deterring, identifying or mitigating the risks.

When do control deficiencies occur?

However, some control deficiencies may occur from time to time. Control deficiencies occur when the controls in place are insufficient or ineffective or when there is a lack of control that contributes to the problem. The entities should take the necessary measures to minimise these deficiencies.

Why do external auditors conduct risk evaluations?

Since the external auditors frequently conduct extensive risk evaluations for a large number of different entities, they may provide the management with valuable insights on control deficiencies discovered across other entities following legislative changes and the procedures to work with internal audit teams.

Why is it important to take the time to audit an entity?

Therefore, it is important for an entity to take the time before an audit to ensure that its controls are up to date on regulatory compliance. This extra effort will help the entity to go a long way towards improving its internal controls and ensure sustainability.

How to avoid risks in audit?

Internal Audit. To avoid risks, entities will first identify the high-risk areas and use a number of internal controls to tackle them. However, sometimes the controls are not enough to keep the risks and threats at bay. There are also times where those controls in place are not functioning as they should. All these might cause issues, which can ...

Why does the probability of each category of risk in each entity differ from one entity to another?

The results will vary from one entity to another because the probability and effect of each category of risk in each entity will differ depending on its environment, its business nature, its competitors, its industry, etc.

Why should entities not seek to remove or even decrease risk?

Because risk is inherent in the pursuit of value, entities should not seek to remove or even decrease it. Instead, they should strive to manage risk exposures across all aspects of their operations so that they take exactly the correct amount of risk at any given time to achieve their strategic objectives.

What do auditors do to determine Internal Control Deficiencies?

However, auditors must not term these as deficiencies. Instead, they must discuss their findings with the client’s management. In some cases, however, that may not be an option. It may happen, for example, when the deficiencies question the management’s integrity or competence.

What is a Significant Deficiency?

A significant deficiency is basically referred to as a deficiency or a combination of internal controls that merit the attention of those charged with governance. These deficiencies relate to a misstatement occurring or the likelihood of it happening in the future and its potential effects. Therefore, significant deficiencies may exist even if auditors cannot identify any deficiencies within an audit engagement.

How to Assess Significant Deficiencies of Internal Control of a Company?

There are several factors that auditors need to consider to assess significant deficiencies of internal control. Once auditors identify areas that may have deficiencies, they will need to consider the following factors to evaluate whether these are significant.

What is a misstatement in audit?

Misstatements detected by the auditor’s procedures that internal controls failed to prevent, or detect and correct.

What is evidence of an ineffective entity risk assessment process?

This evidence may relate to the management’s failure to identify a risk area that auditors would expect to have been covered.

What is IAS 265?

IAS 265 – Communicating Deficiencies in Internal Control to Those Charged with Governance and Management [ Source]

What is a deficiency in design?

A deficiency in design exists when (a) a control necessary to meet the control objective is missing or (b) an existing control is not properly designed so that, even if the control operate s as designed, the control objective would not be met .

What is significant deficiency?

A significant deficiency is a deficiency, or a combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of the company's financial reporting. 1/ See Securities Exchange Act Rules 13a-15 (f) and 15d-15 (f), ...

What is material weakness?

A7. A material weaknessis a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibilitythat a material misstatement of the company's annual or interim financial statements will not be prevented or detected on a timely basis.

What are the limitations of internal control over financial reporting?

Internal control over financial reporting also can be circumvented by collusion or improper management override. Because of such limitations, there is a risk that material misstatements will not be prevented or detected on a timely basis by internal control over financial reporting. However, these inherent limitations are known features of the financial reporting process. Therefore, it is possible to design into the process safeguards to reduce, though not eliminate, this risk.

What is internal control audit?

An Audit of Internal Control Over Financial Reporting that is Integrated with an Audit of Financial Statements

What is A8 in financial reporting?

A8. Controls over financial reporting may be preventive controlsor detective controls. Effective internal control over financial reporting often includes a combination of preventive and detective controls.

What is the meaning of "pertain to the maintenance of records"?

Pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company;