What Exactly Is the FHA 203 (k) Rehab Loan?

- Purchasing a property that requires extensive renovations and repairs

- Purchasing a dilapidated house with the intention of renovating it

- Your current residence need remodeling

- You wish to relocate your present residence to a new location.

How much house can I afford with a FHA loan?

These compensating factors include:

- A higher down payment than the minimum requirement of 3.5%, which most FHA loan borrowers take advantage of.

- Applicants showing dutiful mortgage payments in the past equal to or greater than the new potential loan.

- Excellent credit scores (however, people with great credit scores will probably get more enticing offers from conventional loans).

What to expect with a FHA loan?

most housing experts don’t expect it to dampen homes sales significantly, particularly Houston where prices are still relatively affordable. Even an average mortgage rate of 4 percent is a bargain compared to the double-digit rates of 1980s or the 6 ...

How to buy a house with a FHA loan?

- Windows and doors are cracked or off their hinges

- Handrails and stairs are broken or missing

- The roof is leaky, has more than three layers, or will not last much longer

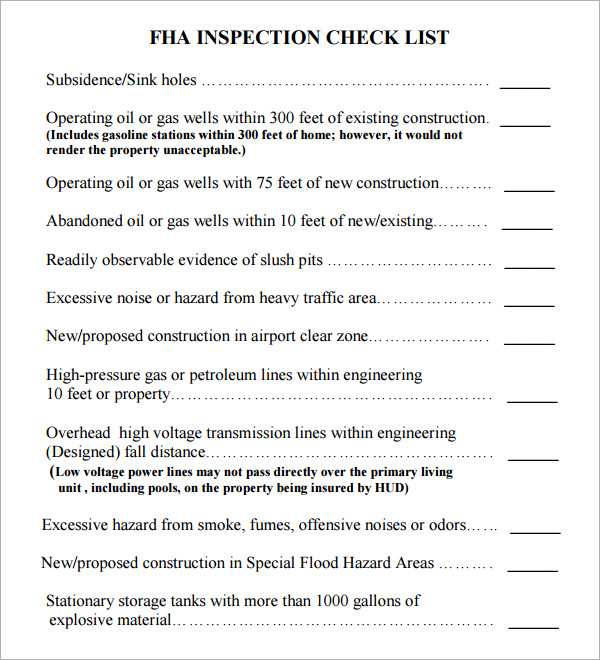

- Close proximity to a hazardous waste site, oil and gas well, or petroleum line

- Close proximity to a transmission tower or high-voltage power lines

Is a FHA loan the same as a VA loan?

While both have less-strict requirements for borrowers compared to conventional loans, there are some differences between FHA and VA loans. Some people might qualify for an FHA loan, but not a VA loan, for example. Another notable difference between a VA loan and an FHA loan is the size of the down payment.

What is a main feature of the FHA rehabilitation loan?

With the FHA Rehab Loan, you have the option to refinance your property and create your own home equity with repairs and upgrades. This 203(k) allows you to buy an older house at a low price (and great interest rates).

What is the difference between FHA and FHA 203k?

The major difference between an FHA 203(b) and a 203(k) mortgage loan is that one is intended for homes in need of extensive repair while the other one isn't.

How hard is it to get a FHA rehab loan?

An FHA 203(k) loan requires a minimum down payment of 3.5% for those who possess a credit score of 580 or above, and 10% for those with a lower score.

What are the cons of a 203k loan?

ConsOnly eligible for primary residences.Mortgage Insurance Premium (MIP) required (can be rolled into loan)Do it yourself work not allowed*More paperwork involved as compared to other loan options.

Is a 203k loan hard to get?

Is an FHA 203k loan hard to get? FHA loans are not hard to get: most lenders work with FHA. However, most lenders do not do 203k Rehab loans. Most lenders do not want to do 203k loans because they take more time, are tougher to get approved, and require more work on the lender's part.

How do I get pre approved for a FHA 203k loan?

To qualify for an FHA 203(k) loan, you'll have to meet the same FHA requirements you would for a standard loan. These include the credit score and down payment minimums mentioned above, as well as having a debt-to-income ratio of at least 50%. The property you're buying or refinancing must be your primary residence.

How do rehab loans work?

To put it simply, a rehab loan lets you purchase or refinance a home and put the costs of your renovation into the form of a loan. You then combine those costs with your mortgage to pay both off in the form of 1 monthly payment.

What credit score is needed for a rehab loan?

Your Credit Score If you currently have at least a 620 FICO score and 3.5% down, you may be eligible for an FHA 203(k) loan. Additional requirements need to be met for those whose FICO scores are below 620.

How long do I have to live in an FHA home before selling?

You need to know how soon after purchasing a home with an FHA loan you can legally sell it. The answer to that is typically 90 (to up to 180) days is best, but in reality you can sell it whenever you need to.

Do sellers like 203k loans?

There's very little downside to a seller accepting an offer with this type of financing. Typically 203K lenders who actively do these types of loans generally have the infrastructure in place to handle rehab loans and have good sales people who know the product(s) and can facilitate the closing for the buyer.

Can you live in a 203k house?

There's only one legitimate way to use a 203k loan for an investment property. You can buy and renovate — or construct or convert — a multifamily (2-4 unit) building and live in one of the units. FHA allows borrowers to purchase 2-, 3-, and 4-unit properties and renovate them using the 203k loan.

Is it worth it to get a 203k loan?

A big benefit of the 203(k) is that you can borrow the funds you need based on what your house is expected to be worth after the renovation is complete. The loan is set up to amortize the cost of the repairs and upgrades into the investment. And you're also gaining instant equity.

What are the benefits of a 203k loan?

203 (k) Rehab Loan Advantages 1 A convenient way to finance your home improvements without the need for perfect credit, huge down payments, or high interest rates 2 Upgrade your home with your style and needs 3 Buy a home that’s usually listed at a lower price due to the older existing condition 4 Great interest rates for your rehab in one loan 5 Come with a low down payment 6 A minimum down payment of 3.5% means you won’t deplete your savings trying to come up with a down payment 7 Qualifications may be more lenient than for a conventional loan because FHA#N#insures your mortgage

How long does it take to repair a home loan after closing?

After closing, the following will occur: A Repair Escrow Account is set up and the repairs must start within 30 days of closing and completed within six months.

What is the minimum down payment for rehab?

Great interest rates for your rehab in one loan. Come with a low down payment. A minimum down payment of 3.5% means you won’t deplete your savings trying to come up with a down payment. Qualifications may be more lenient than for a conventional loan because FHA. insures your mortgage.

What are the rules for FHA 203k?

FHA 203 (k) loan rules include a list of projects that are not allowed, which includes (but may not be limited to) the following: purchase or repair of any luxury item. any improvement that does not become a permanent part of the subject Property. improvements that solely benefit commercial functions within the Property.

What is a gazebo?

gazebos. additions or alterations to support commercial use or to equip or refurbish space for commercial use. The FHA loan rules are not the only ones that can affect FHA 203 (k) transactions; state law, lender standards, and building code may apply to any or all of the eligible improvements permitted under the 203 (k) rehab loan program. ...

Do 203k rehab loans need escrow?

FHA loan rules require escrow accounts to disburse 203 (k) rehab loan funds, and the completed work must meet state/local building code, FHA minimum standards, and other benchmarks where applicable.

Can you cash back on a rehab loan?

For example: cash back to the borrower is not allowed for FHA rehab loans, except specifically required to pay for materials and labor. The basic rule is that the borrower cannot "profit" from the loan in the form of money back that is not a refund or a “draw” for expenses on the renovations/upgrades. FHA loan rules require escrow accounts ...

Can I repair a pool with 203k?

One example: FHA borrowers are allowed to repair a swimming pool with 203 ( k) loan funds, but FHA loan rules state the borrower may not have one installed if one does not currently exist. Bath houses and tennis courts may not be installed, nor can barbecue pits or satellite dishes. The general rule is that FHA 203 (k) loans cannot be used ...

Can I use 203k for luxury?

The general rule is that FHA 203 (k) loans cannot be used for “luxury” items. Speak to your loan officer to learn what the parameters are for your specific needs. making structural alterations such as the repair or replacement of structural damage, additions to the structure, and finished attics and/or basements.

What is 203 H loan?

FHA 203 (h) loans for disaster victims permit the borrower to do the following, with one important additional feature. “The Section 203 (h) Mortgage Insurance for Disaster Victims program allows FHA to insure Mortgages made by qualified Mortgagees to victims of a Presidentially-Declared Major Disaster Area (PDMDA) who have lost their housing, ...

Can you use 203(h) for rehab?

The FHA 203 (h) loan for disaster victims allows the borrower to apply for both of the rehab loans- you can use the “regular” 203 (h ) in conjunction with the version offered to disaster victims if you qualify to do so.

How long does it take to certify a 203k loan?

The contractor must certify work will begin within 30 days of loan closing and must be completed within 6 months. Since the Streamline 203k is for non-structural repairs, the contractor may need to certify that the borrowers will not be displaced for more than 30 days during the repair period.

What is the HUD 203k form?

This form is a breakdown of all loan costs, 203k fees, purchase price, repair bid amount, final loan amount, etc. Your lender will provide you with this form.

What is a 203k loan?

The 203k loan helps the borrower open up one loan to pay for the purchase price of the home, plus the cost of home improvements. Buyers end up with one fixed-rate FHA loan, and a home that’s in much better shape than when they found it. Remodel a bathroom with an FHA 203k loan.

Why is a 203k loan important?

This allows the loan to close before construction has begun. This is important because most sellers won’t allow construction to be done prior to the sale closing. Nor is it a good idea for buyers to sink money into a home that isn’t theirs yet.

How long does a contractor have to complete a home repair?

The contractor has six months to complete the work. When the work is complete, the remaining repair costs are issued to the contractor. The escrow account is closed out. The buyer has a home that is 100% complete, and one loan with one interest rate that covered the original purchase price and all repair costs.

Why are homes in need of repair discounted?

The reason is that the number of buyers who want to take on a fixer-upper is significantly lower than the amount of buyers who want a move-in ready home. Also, most types of financing are not available for these homes.

Can a 203k bid be changed?

An incomplete bid can kill your 203k transaction. A bid may not change nor can repair costs increase after loan closing.

Limited 203 (k) Mortgage

FHA's Limited 203 (k) program permits homebuyers and homeowners to finance up to $35,000 into their mortgage to repair, improve, or upgrade their home. Homebuyers and homeowners can quickly and easily tap into cash to pay for property repairs or improvements, such as those identified by a home inspector or an FHA appraiser.

203 (k) Mortgage

The Section 203 (k) program is FHA's primary program for the rehabilitation and repair of single family properties. As such, it is an important tool for community and neighborhood revitalization, as well as to expand homeownership opportunities.