What is partial claim HUD?

How does HUD partial claim work?

What is the FHA reimbursement?

How to see if you qualify for HUD?

What happens if you default on your mortgage after you receive a HUD claim?

What is HUD insurance?

How long can HUD advance?

See 2 more

:max_bytes(150000):strip_icc()/GettyImages-137556205-9f95ffba1be5439eb659541d9ac04484.jpg)

Can a HUD partial claim be forgiven?

HUD Partial Claim Forgiveness It is designed for borrowers whose loans are heading toward default because of circumstances beyond their control. If approved and paid, the claim amount will later be recovered through a second mortgage.

Does a partial claim hurt your credit?

Does a partial claim hurt credit? A partial claim can hurt your credit if you are late on payments or if you still don't make timely payments. Unlike other loans, a partial claim application probably won't hurt your credit, and it's still less detrimental to your credit than a foreclosure or series of delinquencies.

What is a partial claim payment?

The VA Partial Claim Payment (VAPCP) is a temporary program that is intended to assist Veteran borrowers specifically impacted by the COVID-19 pandemic to resume making their regular (pre-COVID) mortgage payments after exiting forbearance.

Who services HUD partial claims?

Information Systems & Networks Corporation (ISN) is responsible for servicing the following Mortgages in the FHA Single Family Secretary-held Portfolio:Partial Claim Subordinate Mortgages;Section 235 Subordinate Mortgages;Nehemiah Subordinate Mortgages;Emergency Homeowners Loan Program (EHLP) Subordinate Mortgages;More items...

Do you have to pay back a HUD partial claim?

Standalone Partial Claim: Allows mortgage payment arrearages to be placed in a zero-interest subordinate lien against the property. The Partial Claim amount does not require payment until the last mortgage payment is made, the loan is refinanced, or the property is sold, whichever occurs first.

How do I pay off my HUD partial?

All payoff requests must be submitted in writing and include a copy of the Partial Claim Promissory Note. Borrowers unable to locate their Partial Claim Promissory Note should contact their loan servicer.

How is a partial claim calculated?

Partial Claim: The total amount available is the lesser of: (1) the unpaid principal balance as of the date of Default associated with the initial Partial Claim, if applicable, multiplied by 30%, less any previous Partial Claim(s) paid on this Mortgage; (2) if no previous Partial Claim(s), the unpaid principal balance ...

How can I get approved for a partial claim?

Eligibility Requirements for Partial Claim Loans To be eligible for a partial claim the borrower-homeowner must: Be between 4-12 months behind on their mortgage payment. Show they have enough income to make their regular monthly mortgage payments. Live in the property (owner-occupied).

Can I refinance if I have a HUD partial claim?

The HUD puts a lien against the borrower's property for the amount of the claim. The borrower must pay off the partial claim if they either sell the home or refinance it.

Can you be denied for an FHA Partial Claim?

Financial Ability HUD denies partial claims for borrowers that cannot resume their regular monthly payments after the partial claim is paid. The lender analyzes your household income and living expenses. You must have income from employment or other documented and verifiable sources.

Is a partial claim a loan modification?

A "partial claim" is an interest-free loan from HUD to get caught up on overdue payments. The loan doesn't have to be repaid until the first mortgage is paid off, like when you sell the property. Partial claims are sometimes completed along with a loan modification.

Can HUD loans be forgiven?

Notes are forgiven periodically by HUD (principal plus interest less any excess financing) for projects for which there is a record of an approved actual development or modernization certificate.

How long does a partial settlement stay on credit file?

six yearsThis shows future creditors that the debt was cleared for less than the full amount, and this could affect their decision about whether to lend to you. The account will be removed from your credit file six years after it was partially settled, or six years after the date it defaulted if this was earlier.

What happens if I only make a partial car payment?

If you make a partial payment without speaking to your lender, you could get hit with a late fee. The lender may not accept the payment, or will consider the amount that goes unpaid “past due,” as with a credit card. Speak with your lender to find a solution instead.

What happens if I make a partial payment on my credit card?

Debt collectors will start calling. Each month that you make a partial payment, your credit card account falls further and further past due.

Does filing a claim lower your credit score?

Filing any type of insurance claim will not directly impact your credit score. However, if the claim has negative financial consequences, it could indirectly lead to knocks on your credit. For example, having to pay a high deductible or higher insurance premiums could make it difficult to manage your other bills.

Chapter 14. PARTIAL PAYMENT OF CLAIMS, RESTRUCTURING OF HUD-HELD LOANS ...

14-1 Chapter 14. PARTIAL PAYMENT OF CLAIMS, RESTRUCTURING OF HUD-HELD LOANS, AND MODIFICATIONS OF FHA-INSURED LOANS Section 1.GENERAL INFORMATION 14-1. INTRODUCTION Chapter 14 provides guidance regarding three types of FHA workout related multifamily

What Is HUD Partial Claim & Notification? | Home Guides | SF Gate

Borrowers who have delinquent FHA loans need to notify their lenders in order to get the partial claim process started. HUD also needs to be informed about the borrower’s financial hardships.

What is FHA insurance?

The Federal Housing Administration (FHA) provides mortgage insurance on single-family residences, multifamily properties, hospitals and residential care facilities. The FHA works with approved lenders in the United States and agencies such as the U.S. Department of Housing and Urban Development (HUD) to offer HUD partial claim forgiveness.

What is partial claim forgiveness?

HUD partial claim forgiveness pays your lender enough money so that you won't foreclose on your home. Then, you have a second mortgage that abides by rules established by HUD.

How much can a HUD loan modification payoff be?

However, a HUD loan modification payoff cannot be more than the amount of one year’s principal, taxes, insurance and interest.

What is a PPC loan?

It is designed for borrowers whose loans are heading toward default because of circumstances beyond their control. If approved and paid, the claim amount will later be recovered through a second mortgage. An approved PPC will make the mortgage current, and the terms for this are all determined by HUD.

How long does a letter to HUD have to be?

The letter to the lender should include an explanation for the late payments, proof of income, two years of tax returns and bank statements for three to six months. This information is sent to the lender, who will send it on to HUD for approval.

Do you have to pay HUD when you sell your house?

Borrowers must sign promissory notes and repay HUD when that first loan is paid off or the house is sold. Borrowers also have to agree to a partial payment for FHA insurance claims and waive prepayment options (if there were any) on the insurance premiums on the loan’s balance.

Can you default a second time after using PPC?

Some borrowers default a second time after using PPC. In these situations, the lender may do another loan modification or decide to foreclose. The newly modified loan terms would supersede the first PPC. Should the lender refuse to do this, HUD may start collection actions, and the borrower may have to repay the PPC with a lump sum payment.

What is a partial claim?

A partial claim is an interest-free loan from HUD to get caught up on overdue payments on an FHA loan, and is usually completed along with a loan modification. The partial claim does not need to be paid off until the property is sold or the first mortgage is paid off.

Can you have a partial claim against a FHA loan?

If you have an FHA backed loan and you’ve ever had any type of loan workout – including a loan modification or forbearance, odds are you have a partial claim against the home.

Can you sell a home for less than you owe?

If the proceeds of the home sale are insufficient to pay off both loans, you will need to pay the remainder out of pocket or pursue a short sale. FHA has their own short sale process ( FHA PFS Program ), and if you qualify you can sell the property for less than you owe and have the remainder of the debt forgiven.

What happens if I sell my Florida home and I can’t sell for enough to satisfy the mortgage and the partial claim?

If the proceeds of the home sale are insufficient to pay off both loans, you will need to pay the remainder out of pocket or pursue a short sale. FHA has their own short sale process (FHA PFS Program). If you qualify for the program, you can sell the property for less than you owe and have the remainder of the debt forgiven.

What is partial claim?

A partial claim is an interest-free loan from HUD to help make a loan modification possible, or to get you caught up on overdue payments on an FHA loan. The partial claim does not need to be paid off until the property is sold or the first mortgage is paid off.

What is the problem with partial claims?

The problem with partial claims is that they frequently end up being far larger than expected by the homeowner, and usually this additional debt against the home lands the homeowner in a position where they are underwater and must consider a short sale.

Can you file a partial claim against your Florida home?

You may have a HUD partial claim against your Florida home if you have a mortgage backed by FHA and you’ve ever had any type of loan workout – including a forbearance or loan modification.

Can you add videos to your watch history?

Videos you watch may be added to the TV's watch history and influence TV recommendations. To avoid this, cancel and sign in to YouTube on your computer.

How does HUD review a PPC?

HUD’s review of a PPC, Restructuring or Modification request takes place in two phases: The first is carried out by the Hub/PC overseeing the project in question, and the second by the Office of Affordable Housing Preservation/Multifamily (OAHP) at Headquarters. The Applicant must submit an Application to the Hub/PC. Then the Hub/PC must determine that the Application is complete and carry out other steps listed below. This work should be completed within 15 calendar days of receipt of the complete Application. If the Application is incomplete, the lead staff person must notify the Applicant of missing materials immediately and place the request on hold until those materials are provided.

How long does it take to submit a PPC?

For PPCs, the proposal must be submitted within 60 calendar days of default. When in default or facing long term difficulty paying a project’s debt service, the Owner must provide Monthly Accounting Reports to the Hub/PC at least until such time as the PPC, Restructuring or Modification has closed, or later as required by the Hub/PC.

What is an OAHP?

OAHP’s role is to provide the full analysis and underwriting necessary to achieve a balanced assessment of the long-term impact of the proposed transaction on the project, factoring in the cost to the FHA General Insurance Fund and various other considerations. OAHP’s analysis will utilize the PPC Analysis Model for all transactions contemplated in this Chapter. This model helps to perform a real estate feasibility analysis and calculates the amount of the partial payment of claim in the case of a PPC, and the amount of the remaining or new first mortgage debt that a project can carry successfully in the case of a Restructuring or Modification. The most recent version of the model is available to all HUD staff on HUD’s Intranet, and Applicants are encouraged but not required to utilize the model as part of their submission. Applicants may call their HUD Field Office Project Manager to request a copy, and it is essential for Applicants to start with a newly downloaded copy of the latest version for each project.

What is a restructuring note?

Restructurings are refinancings that require 1) a new 223(f) FHA-insured or an uninsured first mortgage offered by a third party that allows for a partial pay down of the HUD-Held note, and 2) recasting of the remaining principal balance of the HUD-Held Note to a new Restructuring Note. The Restructuring Note is subordinated to the new first mortgage, and is paid with 75% of surplus cash. Unlike a PPC, there is no new insurance claim involved in this transaction. To the extent that the new first mortgage provides better terms than the old and relieves the project of some of its first mortgage burden, the project’s operations will benefit and this will help to stabilize and preserve the housing.

Does HUD only cover PPCs?

HUD’s Multifamily Claims Branch will be involved only in PPCs as the other types of transactions do not involve FHA General Insurance Fund claims. Consequently this section applies only to PPCs and not to Restructurings or Modifications.

What is a HAMP loan?

FHA Home Affordable Modification Program (HAMP): FHA HAMP is designed to help FHA-insured borrowers who meet HAMP eligibility requirements to avoid foreclosure by permanently reducing their monthly mortgage payment through the use of a partial claim. The partial claim defers the repayment of mortgage principal through an interest-free subordinate mortgage that is not due until the first mortgage is paid off. Under the partial claim option, lenders are authorized to advance funds on behalf of a borrower, to reinstate a delinquent loan. HAMP will allow HUD to bring eligible FHA borrowers' payments down to an affordable level. This will be accomplished by bringing the mortgage current, buying down the loan by up to 30 percent of the unpaid principal balance and deferring these amounts in a partial claim.

What is the National Servicing Center?

Through its National Servicing Center (NSC), FHA offers a number of various loss mitigation programs and informational resources to assist FHA-insured homeowners facing financial hardship, and whose mortgage is either in default or at risk of default .

How to contact FHA?

The Online FHA Resource Center. Call the FHA Resource Center at 1-800-CALL FHA (800-225-5342) Persons with hearing or speech impairments may access this number via TTY by calling the Federal Information Relay Service at (800) 877-8339. Email the FHA Resource Center.

What is the FHA?

In response, The Federal Housing Administration (FHA), which is a part of the U.S. Department of Housing and Urban Development (HUD), is working aggressively to halt and reverse the losses represented by foreclosure.

Is foreclosure rate increasing?

Communities across the United States are experiencing steady and even increasing rates of foreclosure, as well as an increase in the number of homeowners at risk of foreclosure.

What is a forbearance in mortgage?

Servicers of FHA-insured mortgages are required to offer homeowners suffering financially due to COVID-19 a mortgage payment forbearance – a temporary pause or reduction in mortgage payments when the homeowner requests this assistance . FHA extended the timeframe for homeowners to request a mortgage payment forbearance from their mortgage servicer through September 30, 2021.

What is the FHA recovery for 2021?

WASHINGTON - The Federal Housing Administration (FHA) on July 23, 2021 announced streamlined COVID-19 Recovery options to help homeowners with FHA-insured mortgages who have been financially impacted by the COVID-19 pandemic bring their mortgage current and remain in their homes. The simplified COVID-19 Recovery waterfall allows mortgage servicers to offer eligible homeowners who cannot resume making their mortgage payments a reduction in the principal and interest portion of their monthly payments. The changes announced today will provide those most in danger of losing their homes a path to deep and sustained recovery, including lower income individuals, families of color, and young, first-time homeowners who have disproportionately suffered economic hardships due to the pandemic.

What is the recovery modification for a mortgage?

COVID-19 Recovery Modification: for homeowners who cannot resume making their current monthly mortgage payments, the COVID-19 Recovery Modification extends the term of the mortgage to 360 months at a fixed rate and targets reducing the borrower’s monthly principal and interest portion of their monthly mortgage payment. The COVID-19 Recovery Modification must include a Partial Claim if the homeowner has Partial Claim funds available.

What are mortgagees reminded of?

Mortgagees are also reminded of their obligations under the Fair Housing Act and the Americans with Disabilities Act (ADA) to make exceptions or modifications to rules, policies, practices, and services for Borrowers with disabilities who need them. Mortgagees should contact HUD’s Office of Fair Housing and Equal Opportunity at 800-669-9777 (voice) or 800-927-9275 (TTY) if they believe FHA may need to consider a reasonable accommodation for a Borrower with a disability to any of the rules or policies described in this Mortgagee Letter. Mortgagees are further reminded of their ADA obligation to communicate effectively with, individuals with disabilities including individuals with vision disabilities who cannot read standard print notices and deaf individuals who use Relay Services to communicate by telephone.

How long does a non-occupant loan last?

For properties that are not occupied by the owner, mortgage servicers must offer eligible homeowners FHA’s COVID-19 Recovery Non-Occupant Loan Modification, which extends the term of the mortgage to 360 months, or less if requested by the homeowner, at a fixed interest rate.

How long can a non-occupant mortgage be modified?

This option allows for a fixed-rate mortgage modification of up to 30 years, or less if requested by the borrower.

What is a deed in lieu of foreclosure?

The COVID-19 Deed-in-Lieu of Foreclosure for homeowners who, are unable to keep their home after all home retention options are exhausted, and who are unable to complete a pre-foreclosure sale. With a Deed-in-Lieu of Foreclosure, the homeowner voluntarily offers the deed to HUD in exchange for a release from all obligations under the mortgage.

Forbearance for Borrowers Affected by the COVID-19 National Emergency

COVID-19 Forbearance: If you can’t pay your mortgage because you’re struggling financially due to COVID-19, you can ask for mortgage payment relief (forbearance) through the end of the Presidentially Declared COVID-19 National Emergency.

COVID-19 Recovery Options

FHA offers COVID-19 Recovery Options to borrowers who are on a COVID-19 Forbearance, or borrowers who did not participate in a COVID-19 Forbearance who were 90 days or more delinquent through the end of the Presidentially Declared COVID-19 National Emergency.

Homeowner Assistance Funds

The American Rescue Plan Act of 2021 established the Homeowner Assistance Fund (HAF) in the U.S. Department of the Treasury in order to provide financial assistance to eligible homeowners who have suffered financial hardships during the COVID-19 National Emergency.

CONTACT FHA

FHA staff are available to help answer your questions and assist you to better understand your options as an FHA borrower under these loss mitigation programs. There are several ways you can contact FHA for more information, including:

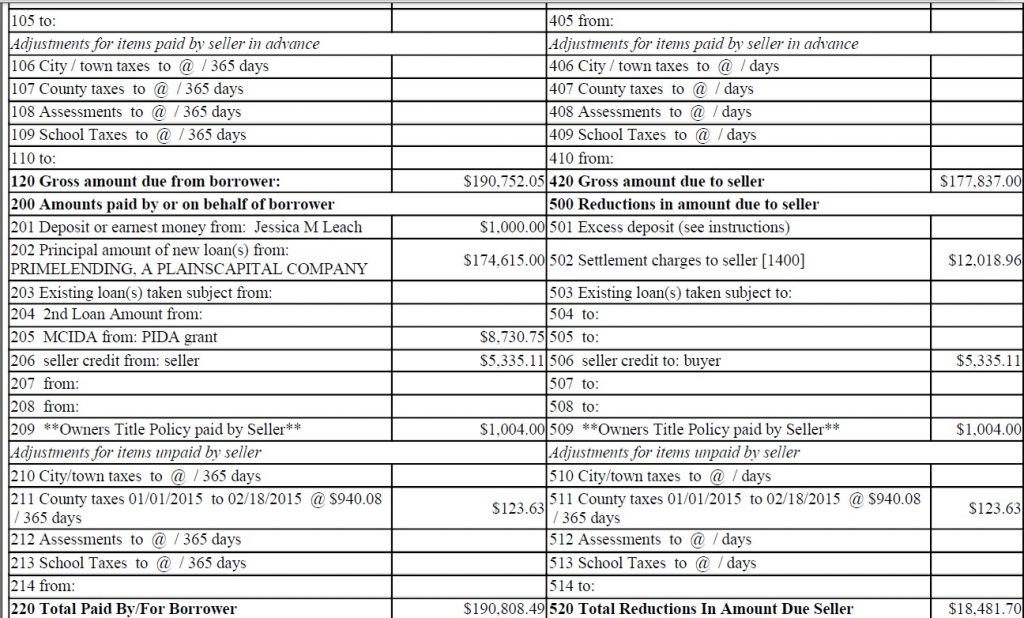

What is a partial claim on a mortgage?

A partial claim is a non-interest bearing, lump sum amount of money that gets recorded against a property as a subordinate lien to the primary mortgage.

How does a partial claim help me transition off forbearance?

A partial claim can be used to transition off of your COVID-19 Forbearance plan as a “standalone partial claim.” A “standalone partial claim” is the name for the type of partial claim that applies specifically to a COVID Forbearance transition and is not part of a modification.

How is a partial claim used in a loan modification?

If you get approved for a loan modification, a partial claim is the tool that FHA uses to put your arrears on the end of the loan, so you don’t have to pay everything you missed at one time.

Can you refinance if you have a partial claim?

After your partial claim is executed and you are back on track with your regular monthly mortgage payments, you can complete a refinance of your loan with a new lender (if you qualify).

What Is A FHA Modification?

A FHA modification will add any arrearages that are owed and add them into your current loan; extend the term out to a 30 year mortgage and use the current interest rate at the time the modification is being done.

What Is A Trial Payment?

A trial payment plan is making the new modification payment for around 3-4 months. After the plan has ended the modification will occur.

Why does FHA require mortgage insurance?

Mortgage insurance is where it protects the lender in the event that the homeowner defaults on the loan. Because FHA takes such higher risk clients ex: low credit score, lower down payments; the mip helps the lender take these risks.

What is the amount of delinquency?

To explain the amounts for the partial claim above, amount of delinquency is how much you were in the arrears with your mortgage payment. Legal fees are if you were referred to foreclosure, then you would have this fees.Principal deferment is how much the servicer is taking off of your current principal balance of your mortgage.

What is partial claim FHA?

What Is A Partial Claim? A FHA Partial Claim is where hud (housing and urban development), gives a loan to you to cover any arrearages, fees and a possibility of taking off some of your unpaid principal balance of your current mortgage.

How long does a trial payment plan last?

You might be on a trial payment plan before the modification is complete. A trial payment plan is making the new modification payment for around 3-4 months. After the plan has ended the modification will occur.

How much is a modified trial payment?

Let’s say your current payment is $800 a month and your new modified trial payment is $600 a month. When you make the first trial payment of $600 that is not enough to cover your current payment. The servicer cannot apply a payment until they have the full $800. The $800 payment will be applied after you make your second trial payment.

What is partial claim HUD?

The HUD partial claim program includes paying the lender on behalf of the homeowner to avoid foreclosure with these funds. To see if you are eligible for a HUD Partial Payments of Claim, you should contact your lender to discuss your delinquent mortgage payments.

How does HUD partial claim work?

HUD partial claims benefit the homeowner by allowing him or her to keep their existing home, thus preserving affordable housing. It also fixes the current default, bringing payments up to date. The program benefits FHA by restructuring the original debt in a way that guarantees more contributions to the FHA General Insurance Fund.

What is the FHA reimbursement?

Lenders are reimbursement from FHA if a borrower defaults. When a loan is insured through FHA, borrowers pay a mortgage insurance premium each year that is approximately 1 percent of the loan amount.

How to see if you qualify for HUD?

To see if you are eligible for a HUD Partial Payments of Claim, you should contact your lender to discuss your delinquent mortgage payments . The lender will examine your situation and determine if you qualify for this service.

What happens if you default on your mortgage after you receive a HUD claim?

If you default on your mortgage after you have received a HUD claim, you may be granted a loan modification or another option so you won’t lose your house through foreclosure.

What is HUD insurance?

The Department of Housing and Urban Development (HUD) has traditionally focused on supporting low to moderate-income home ownerships. Through the Federal Housing Administration’s (FHA) insurance programs, HUD makes loans available to those who otherwise would not meet income requirements. Lenders are reimbursement from FHA if a borrower defaults.

How long can HUD advance?

HUD can advance up to 12 months of mortgage payments through this program. The partial claim total can not exceed 12 months of payment, including the principal, interest, taxes, and insurance.