How do you calculate interest on a mortgage loan?

- Comparing the monthly payment for several different home loans

- Figuring how much you pay in interest monthly and over the life of the loan

- Tallying how much you actually pay off over the life of the loan versus the principal borrowed, to see how much you actually paid extra

What is the formula for calculating interest on a mortgage?

- Identify the sanctioned loan amount, which is denoted by P.

- Now figure out the rate of interest being charged annually and then divide the rate of interest by 12 to get the effective interest rate, which is denoted by r.

- Now determine the tenure of the loan amount in terms of a number of periods/months and is denoted by n.

What are the benefits of interest only mortgage?

What are the benefits of interest-only loans?

- Enjoy lower repayments Whether you apply for an interest-only loan or you switch to interest-only payments, you will be able to trim the amount of your repayments. ...

- Take advantage of tax deductions Interest-only loans allow investors to maximise their tax-deductible expenses. ...

- Manage expenses

What are the benefits of interest only loans?

What are the benefits of interest-only loans? 1. Enjoy lower repayments. Whether you apply for an interest-only loan or you switch to interest-only payments, you will be able to trim the amount of your repayments. As mentioned earlier, your repayments over the interest-only period only cover the interest charges.

What Is an Interest-Only Mortgage?

What is the introductory period?

Why do first time home buyers have interest only mortgages?

How long does a 7/1 ARM last?

How long do you have to pay interest on a mortgage?

What does it mean when you pay interest on a house?

Can you refinance a mortgage after the interest only term has expired?

See 4 more

About this website

Why would you have an interest-only mortgage?

The main benefit of an interest-only mortgage is that your monthly payments will be cheaper. This means that you could potentially borrow more.

What happens at the end of an interest-only mortgage?

If you have an Interest Only mortgage, your monthly payments have been paying the interest but have not reduced your loan balance (unless you have been making overpayments to purposely reduce the balance of your mortgage). This means that at the end of your agreed mortgage term, you need to repay your loan in full.

Is an interest-only loan a good idea?

Riskier loans with Higher Interest Rates. Since interest-only loans, which were once easy to sell to other financial institutions, are now less marketable, lenders demand larger down payments from borrowers and they charge more interest than on conventional loans, which are considered a better risk.

How do I qualify for an interest-only mortgage?

Banks take on a bigger risk when they offer interest-only mortgages, so lenders look for well-qualified borrowers with a minimum credit score of 700 or higher, a debt-to-income (DTI) ratio of 43 percent or lower and a down payment of at least 20 percent to 30 percent.

How much deposit is needed for an interest-only mortgage?

Many lenders require a 50% deposit for interest-only mortgages, but some specialist lenders and private banks can go as high as 75% LTV interest only mortgages in the right circumstances. You'll likely need a specialist mortgage adviser to secure this type of loan.

How long can you pay interest-only mortgage?

On an investment property, interest-only repayments can be requested and applied to existing or new loans for up to 10 years over the life of the loan.

What is a main disadvantage of the interest only loan?

You cannot build equity with an interest-only mortgage because you're only paying the interest. Underwater risk-when your home depreciates in value, you may end up paying more than its actual worth at the time of sale. You will have to pay the principal one day. You cannot keep putting off payment.

Can you pay off an interest-only mortgage early?

Can you Pay-off an Interest-Only Mortgage Early? Yes, you can pay off an interest-only mortgage early but as with fixed-rate mortgages this might incur an Early Repayment Charge (ERC) so check with your lender.

Is it harder to get an interest-only mortgage?

It's possible to get an interest only mortgage with bad credit, but it's not easy in today's anti-risk lending environment. If you still have outstanding debt to pay off, this could make things even more complicated, as potential lenders will want to be sure that you can repay what you owe them.

What is a good example of an interest-only loan?

A line of credit is a good example of an interest-only loan. Because there are no principal payments, the monthly servicing requirements are low. They can also be paid back and then “redrawn” (meaning borrowed again) without penalty, making them highly flexible.

Do banks still do interest-only mortgages?

In fact, some lenders will only consider this type of mortgage for high-net-worth individuals. If you're able to meet the criteria, however, it's perfectly possible to use an interest-only mortgage to purchase residential property.

What happens when the interest on an interest-only mortgage is paid in full?

Once the interest-only period ends, you'll have to start repaying principal over the rest of the loan term—on a fully-amortized basis, in lender speak.

Can I get an extension on my interest-only mortgage?

Yes, it is possible. But, extending the term with your current provider is by no means guaranteed. Interest-only mortgages are riskier than conventional ones, making applying for an extension more difficult at times. Extensions are always at the discretion of the lender.

What is the longest term for an interest-only mortgage?

25 yearsInterest only mortgage It is entirely your responsibility to ensure that at the end of the term the remaining balance on your mortgage is repaid in full by your repayment strategy. The maximum term for interest only is 25 years.

Do you get all interest back your house?

For most homeowners, mortgage interest is their biggest tax deduction and getting a home loan allows a home buyer to make the shift from the standard tax deduction to itemized deductions. You do not get all of your mortgage interest back on your tax return.

Interest-only mortgage: Pros & cons | Chase.com

To put it simply, an interest-only mortgage is when you only pay interest the first several years of the loan — making your monthly payments lower when you first start making mortgage payments. Though this may sound like an exciting opportunity to help save on your mortgage payments, before exploring interest-only loan options, learning how they work is key.

How Interest-Only Mortgages Work: Pros & Cons - NerdWallet

An interest-only mortgage allows payments that never reduce your debt. You'll have a lower monthly payment, but there are drawbacks to consider.

How can an interest-only mortgage calculator help?

You can use an interest-only mortgage calculator to help break down what your payments will look like the first few years with interest-only, and the consecutive years when principal rates kick in to see if this type of mortgage makes sense for you.

How long does an interest only loan last?

Most interest-only loans are structured as an adjustable-rate mortgage (ARM) and the ability to make interest-only payments can last up to 10 years. After this introductory period, you’ll start to repay both principal and interest. This is repaid in either a lump sum or in subsequent payments. The interest rate on an ARM Loan can increase or decrease throughout the length of your loan, so when your rate adjusts, your payment will change too.

What is interest only mortgage?

To put it simply, an interest-only mortgage is when you only pay interest the first several years of the loan — making your monthly payments lower when you first start making mortgage payments. Though this may sound like an exciting opportunity to help save on your mortgage payments, before exploring interest-only loan options, learning how they work is key.

What happens when interest only mortgage ends?

An important thing to remember about interest-only mortgages is: Once the interest-only period ends, you begin paying both the interest and principal. You have the option of making principal payments during your interest-only payment term, but once the interest-only period ends, both interest and principal payments are required. Keep in mind that the amount of time you have for repaying the principal is shorter than your overall loan term.

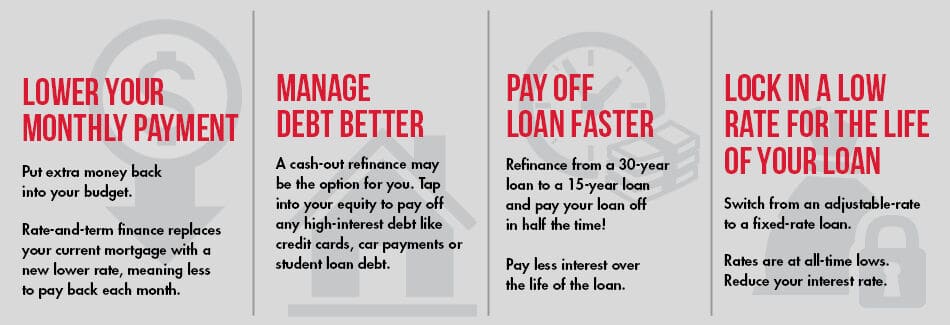

Can you pay off a loan faster than a conventional loan?

Can be paid off faster than a conventional loan: If you’re making extra payments towards an interest-only loan, the lower principal can generate a lower payment each month. When it comes to a conventional loan, extra payments can reduce the principal, but the monthly payments remain the same.

Is interest only mortgage good?

An interest-only mortgage has its benefits and drawbacks. If you’re looking for lower monthly payments or a short-term living arrangement, this could be the right option for you. Keep in mind that payments towards your principal are inevitable down the line. Talk with a Home Lending Advisor to see if an interest-only mortgage is right for you.

Can lower monthly payments increase your cash flow?

Possible increase to your cash flow: Lower monthly payments can leave you with a few extra dollars in your budget.

Can You Get an Interest-only Loan?

Interest-only loans are considered nonqualified mortgages. This means that Fannie Mae and Freddie Mac—the government-sponsored enterprises that buy most mortgages from lenders to help credit flow to homebuyers—don’t purchase or back interest-only mortgages. Freddie stopped in 2010, and Fannie stopped in 2014. You also won’t find interest-only Federal Housing Administration (FHA), Veterans Affairs (VA), or U.S. Department of Agriculture home loans.

What happens if you don't plan to keep your mortgage?

If you do not plan to keep the mortgage longer than the interest-only period. If you are buying out another person’s ownership in a home and need low monthly payments until you can sell it. If you need temporary financing on a new home while you’re trying to sell your old home (an alternative to a bridge loan ).

Why are interest only mortgages so hard to come by?

Part of the reason why interest-only mortgages are harder to come by is because they were a contributor to the 2008 financial crisis as borrowers could no longer afford the spike in mortgage payments when the loan ammortized and home values were underwater.

How does an interest only mortgage work?

An interest-only mortgage allows you to pay just the interest and no principal with each monthly payment, usually for the first five, seven or 10 years of the loan term .

What happens to the principal balance of a mortgage every month?

In this scenario, your overall principal mortgage balance declines every month which means the interest charged is lower the following month. In the case of an interest-only mortgage, once that interest-only period ends, the loan becomes fully amortized. That means you then pay principal and interest every month.

Why is interest less if you don't pay principal?

As more of your monthly payments lower the principal balance, the interest charged will also be less because it’s based on the total balance. It’s also important to note that if you don’t pay any principal, you don’t accumulate equity, unless the market value of your home goes up.

Can you leverage your savings?

Leverage your savings: With no principal payment for several years, you can leverage that money toward another investment that might have a stronger performance in a short time period. But then again, it’s a calculated risk.

Who Might Want an Interest-Only Loan?

An interest-only mortgage may have its perks, but these loans also come with risks that borrowers should be aware of. You may want to consider one of these loans if:

What are the factors that are considered when considering a home loan?

As with any mortgage, lenders considering you for an interest-only home loan will review factors like credit history, down payment, employment, income, assets, and home value.

How long do you have to pay interest on a mortgage?

These loans let you pay just the interest for a set period of time, normally five to 10 years.

How long does principal plus interest stay in a mortgage?

When the initial 10 years are up, you’ll begin paying principal plus interest for the remaining 20 years, and the interest rate will continue to adjust annually.

What are the closing costs for an interest only loan?

As with any mortgage, when you take out an interest-only loan, you can expect to pay closing costs, such as the origination fee, the appraisal fee, and the title insurance premium.

What are the two types of interest only mortgages?

There are two types of interest-only mortgages: fixed-rate and adjustable-rate mortgages. Here’s a look at the two options.

Is an interest only mortgage considered an ARM?

An interest-only mortgage, usually an ARM, could make sense in certain situations, but a borrower could end up paying much more in interest in the long run compared with having a fully amortized loan.

What is an interest-only mortgage?

An interest-only mortgage is exactly what it sounds like: a home loan that allows borrowers to make interest-only payments for a set amount of time, typically between seven and 10 years, at the start of a 30-year term. After the introductory period ends, the borrower begins paying principal and interest for the remainder of the loan term at a variable interest rate.

How do interest-only mortgages work?

With an interest-only mortgage, the borrower pays interest at a fixed or adjustable rate during the interest-only period. The interest rates are comparable with what you might find with a conventional loan, but the initial payments are much lower. Borrowers must still pay taxes, insurance and possibly private mortgage insurance (PMI).

Can I change my current loan to an interest-only mortgage?

It is possible to refinance a traditional mortgage to an interest-only loan, and homeowners may consider this option as a way to free up money to put toward short-term investments or an unexpected expense. You would meet the same scrutiny and requirements as you would if applying for a first-time interest-only loan.

What do mortgage reporters and editors focus on?

Our mortgage reporters and editors focus on the points consumers care about most — the latest rates, the best lenders, navigating the homebuying process, refinancing your mortgage and more — so you can feel confident when you make decisions as a homebuyer and a homeowner.

How long does an interest only mortgage last?

An interest-only mortgage is exactly what it sounds like: a home loan that allows borrowers to make interest-only payments for a set amount of time, typically between seven and 10 years, at the start of a 30-year term.

How much does it cost to refinance a home?

In any refinance, you will need to receive a home appraisal and pay closing costs and fees. Refinancing can cost 3 percent to 6 percent of the home’s total amount. In addition, if you have less than 20 percent equity in your home, you will be required to pay PMI.

What happened in the late 2000s?

Leading up to the housing crisis of the late 2000s, homebuyers gave in to the instant gratification of mortgages that allowed them to make interest-only payments at the start of the loan, so long as they took on supersized payments over the long term. In the end, many people lost their homes.

What Is an Interest-Only Home Loan?

However, with an interest-only mortgage, borrowers only pay the interest on their home loan for a period that generally ranges from five to ten years. After this initial period has expired, payments are recalculated and borrowers begin paying down the principal amount.

How Do I Qualify for an Interest-Only Mortgage?

In general, more people are able to qualify for our non-QM loan program compared to qualified mortgages (QMs). That’s because QMs have stricter qualification criteria and more stringent income verification standards. Non-QM loans, on the other hand, don’t rely on traditional income verification methods. This can make interest-only loans attractive prospects for real estate investors and other individuals whose income isn’t accurately reflected on tax returns, W-2s, and other income documents.

Are There Any Risks with Interest-Only Loans?

Although interest-only loans allow borrowers to make low mortgage payments for a few years, you should consider the risks of these types of loans before applying. Some of the most important factors to consider when taking out an interest-free loan include:

Is an Interest-Only Right for You?

If you’re considering applying for an interest-only loan, it’s important to evaluate your financial situation and come up with a long-term plan. Interest-only loans have unique demands, such as a substantial increase in future mortgage payments, so it’s essential that you’re prepared to meet those demands.

Why do people choose interest only mortgages?

In general, borrowers choose interest-only mortgages because lower payments upfront can free up cash flow that can be used to expand your investment portfolio, build wealth, or simply make mortgage payments manageable. These payments are also typically tax-deductible during the interest-only term.

What happens after interest only period?

After the interest-only period, the remaining balance will be amortized, meaning that you will make equal monthly payments on the balance. You also have the option to refinance your home or pay a lump sum toward the balance of the mortgage. While you are only obligated to pay interest during the first period according to the loan terms, ...

What is bank statement loan?

Bank statement loans: Loans where bank statements can be used as the sole source of income verification.

Who can qualify for an interest-only mortgage?

Compared with a typical principal-and-interest mortgage, interest-only loans often require higher down payments and lower debt-to-income ratios, as well as good-to-excellent credit scores — for example, a FICO score of 700 or higher.

What happens if you opt for interest only again?

If you opt for the interest-only loan again, it's likely your mortgage rate will change. Who knows whether that will be higher or lower?

How long does a home loan last?

These home loans are usually structured as adjustable-rate mortgages and frequently have terms of up to 10 years.

What is the best suited borrowers?

The best-suited borrowers have cash and liquid investment assets and are in a "very strong financial position," Linnane says. "The fact that they are not reducing principal is not a danger for them."

How long is an interest only loan?

An interest-only loan is offered for a relatively short term, usually five to 10 years. If you remain in the home, you can refinance the loan into a traditional principal-and-interest mortgage, or sign up for another interest-only term.

What happens if the market declines?

If market values decline, you could lose any equity in your home provided by your down payment — and perhaps any opportunity to refinance.

Can interest only mortgages be used for a job?

Interest-only mortgages can be appropriate for borrowers who are disciplined enough to make periodic principal payments as well. They might also work for someone with a job that pays large annual bonuses that can be used to pay down the principal balance of the loan each year.

What Is an Interest-Only Mortgage?

An interest-only mortgage is a type of mortgage in which the mortgagor (the borrower) is required to pay only the interest on the loan for a certain period. The principal is repaid either in a lump sum at a specified date, or in subsequent payments.

What is the introductory period?

You pay just the interest, at a fixed rate, for a certain number of years, known as the introductory period . After the introductory period ends, the borrower starts repaying both principal and interest, and the interest rate will start to vary. For example, if you take out a "7/1 ARM", it means your introductory period of interest-only payments ...

Why do first time home buyers have interest only mortgages?

For first-time home buyers, an interest-only mortgage also allows them to defer large payments into future years when they expect their income to be higher.

How long does a 7/1 ARM last?

For example, if you take out a "7/1 ARM", it means your introductory period of interest-only payments lasts seven years, and then your interest rate will adjust once a year. Fixed-rate interest-only mortgages are not very common; they usually exist on longer, 30-year mortgages.

How long do you have to pay interest on a mortgage?

Most interest-only mortgages require only the interest payments for a specified time period—typically five, seven, or 10 years.

What does it mean when you pay interest on a house?

However, just paying interest also means that the homeowner is not building up any equity in the property —only the repayment of principal debt does that. Also, when payments start to include principal, they get significantly higher. This could be a problem if it coincides with a downturn in one's finances—loss of a job, an unexpected medical emergency, etc.

Can you refinance a mortgage after the interest only term has expired?

At the end of the interest-only mortgage term, the borrower has a few options. Some borrowers may choose to refinance their loan after the interest-only term has expired, which can provide for new terms and potentially lower interest payments with the principal. Other borrowers may choose to sell the home they mortgaged to pay off the loan. Still other borrowers may opt to make a one-time lump sum payment when the loan is due—having saved up by not paying the principal all those years.

How An Interest-Only Works

- Most interest-only loans are structured as an adjustable-rate mortgage(ARM) and the ability to make interest-only payments can last up to 10 years. After this introductory period, you’ll start to repay both principal and interest. This is repaid in either a lump sum or in subsequent payments. The interest rate on an ARM Loan can increase or decreas...

Why Get An Interest-Only Mortgage

- If you’re interested in keeping your month-to-month housing costs low, an interest-only loan may be a good option. Common candidates for an interest-only mortgage are people who aren’t looking to own a home for the long-term — they may be frequent movers or are purchasing the home as a short-term investment. If you’re looking to buy a second home, you may want to consi…

The Pros of An Interest-Only Loan

- Interest-only loans may make financial sense for some borrowers because: 1. The initial monthly payments are usually lower: Since you’re only making payments towards interest the first several years, your monthly payments are usually lower compared to some other loans. 2. May help you afford a pricier home: You may be able to borrow a larger sum of money because of the low…

The Cons of An Interest-Only Loan

- Choosing an interest-only loan could be a risk for borrowers. Some cons with this type of loan include: 1. You’re not building equity in the home: Building equity is important if you want your home to increase in value. With an interest-only loan, you aren’t building equity on your home until you begin making payments towards the principal. 2. You can lose existing equity gained from y…

How Can An Interest-Only Mortgage Calculator Help?

- You can use an interest-only mortgage calculator to help break down what your payments will look like the first few years with interest-only, and the consecutive years when principal rates kick in to see if this type of mortgage makes sense for you.

Learn More About Interest-Only Mortgage Options

- An interest-only mortgage has its benefits and drawbacks. If you’re looking for lower monthly payments or a short-term living arrangement, this could be the right option for you. Keep in mind that payments towards your principal are inevitable down the line. Talk with a Home Lending Advisorto see if an interest-only mortgage is right for you.

How Interest-Only Mortgages Work

Interest-Only Loan Costs

- The national average interest-only mortgage rateis not as widely available like other popular 30-year fixed, 15-year fixed and 5/1 ARM rates are. You may have to shop multiple lender websites to get a general idea of rates. As with any mortgage, you can expect to pay a rate in proportion with the loan’s risk. And you will likely get the best rate by shopping around to get quotes from severa…

Can You Get An Interest-Only Loan?

- Interest-only loans are considered nonqualified mortgages. This means that Fannie Mae and Freddie Mac—the government-sponsored enterprisesthat buy most mortgages from lenders to help credit flow to homebuyers—don’t purchase or back interest-only mortgages. Freddie stopped in 2010, and Fannie stopped in 2014. You also won’t find interest-only Federal Housing Administ…

Pros and Cons of Interest-Only Mortgages

- Some people think interest-only mortgages are inherently risky, but that’s not always the case. It depends on the type of borrower and their financial situation. Learning the pros and cons of an interest-only mortgage will help illustrate this point.

Who Is Best Suited For An Interest-Only Mortgage

- You might benefit from an interest-only mortgage if one or more of these characteristics apply to you: 1. If you do not plan to keep the mortgage longer than the interest-only period. 2. If you are buying out another person’s ownership in a home and need low monthly payments until you can sell it. 3. If you need temporary financing on a new home while you’re trying to sell your old hom…

What Is An Interest-Only Mortgage?

How Do Interest-Only Mortgages Work?

- With an interest-only mortgage, the borrower is only required to pay interest at a fixed or adjustable rate during the interest-only period. The interest rates are comparable with what you might find with a conventional loan, but the initial payments are much lower. Borrowers must still pay taxes, insurance and possibly private mortgage insurance(PMI). Even though you’re only req…

Example of An Interest-Only Mortgage

- Say you obtain a 30-year interest-only loan for $330,000, with an initial rate of 5.1 percent and an interest-only term of seven years. During the interest-only period, you’d pay roughly $1,403 per month. After this initial phase, the payment would rise to $2,033 per month — assuming your rate doesn’t change. Many interest-only loans convert to an adjustable rate, so if rates rise in the futu…

Candidates For Interest-Only Mortgages

- The best candidates for an interest-only mortgage are borrowers who have full confidence they’ll be able to cover the higher monthly payments when they arise. For example, if you’re in medical school and want to buy a home, you’re likely on a tight budget now, but can count on a bigger paycheck when you establish your practice. If you flip houses, an interest-only loan might help y…

Pros and Cons of Interest-Only Mortgages

- Interest-only loans can be a prudent personal finance strategy under certain circumstances, but they’re not a good idea for everyone. Here are some pros and cons:

How to Qualify For An Interest-Only Mortgage

- Interest-only loans have been harder to come by since the fallout of the housing crisis. Fewer lenders offer them, and banks have set stricter requirements to qualify. Banks take on a bigger risk when they offer interest-only mortgages, so lenders look for well-qualified borrowers with a minimum credit score of 700 or higher, a debt-to-income (DTI) ratio of 43 percent or lower and a …

Can I Change to An Interest-Only Mortgage?

- It is possible to refinance a traditional mortgage to an interest-only loan, and borrowers might consider this option as a way to free up money to put toward short-term investments or an unexpected expense. You would meet the same scrutiny and requirements as you would if applying for a first-time interest-only loan. The same requirements of refinancing also apply, an…

Bottom Line

- Interest-only mortgages are not ideal for most people, but they can be a useful tool for homeowners who fully understand the risks involved and can exercise extreme self-control. In exchange for having low mortgage payments on the front end, you could eventually face enormous monthly payments that your income doesn’t support — and if you choose not to pay d…