What is the guidance on consideration payable to a customer?

The guidance on consideration payable to a customer states that such amounts should be recognized as a reduction of revenue at the later of when the related revenue is recognized or the entity pays or promises to pay such consideration (promises could be implied by customary business practices).

Should we evaluate all consideration paid to customers?

While evaluating all consideration paid to customers would potentially be time consuming and costly, this would improve the entity’s chances of accounting for all transactions appropriately. Members of the TRG noted that this approach seems to be best supported by the revenue standard.

How do you account for consideration payable in accounting?

The entity concludes that the consideration payable is accounted for as a reduction in the transaction price when the entity recognizes revenue for the transfer of the goods. Consequently, as the entity transfers goods to the customer, the entity reduces the transaction price for each good by 10 percent ($25,000 ÷ $250,000).

What happens if the amount of consideration payable exceeds fair value?

If the amount of consideration payable to the customer exceeds the fair value of the distinct good or service that the entity receives from the customer, then the entity shall account for such an excess as a reduction of the transaction price.

How do you account for consideration payable?

Any excess consideration payable over the fair value of the distinct goods or services received should be accounted for as a reduction of the transaction price. If the fair value cannot be reasonably estimated, the entire consideration payable results in a reduction of the transaction price.

When determining the transaction price the following must be considered?

As per ASC 606-10-32-2, An entity shall consider the terms of the contract and its customary business practices to determine the transaction price. As per ASC 606-10-32-3, The nature, timing, and amount of consideration promised by a customer affect the estimate of the transaction price.

Is the amount of consideration that a company expects to receive from a customer?

The transaction price is the amount of consideration that a company expects to receive from a customer in exchange for transferring a good or service.

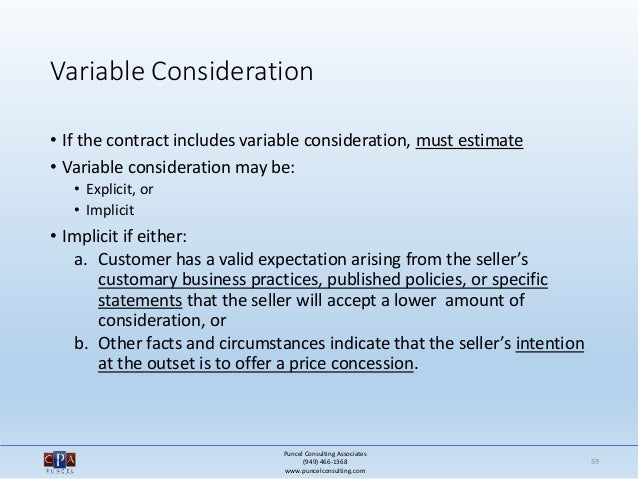

What is variable consideration and how is it measured?

Variable consideration is defined broadly and can take many forms, such as price concessions, rebates or refunds. Consideration is also considered variable if the amount an entity will receive is contingent on a future event occurring or not occurring, even though the amount itself is fixed.

What expected consideration?

Expected consideration uncertainty occurs for an extended period; The entity's experience with similar contracts is limited; The entity's practices include offering a broad range of price concessions; and. The contract has a broad range of possible consideration amounts.

What is consideration in revenue?

Variable consideration includes discounts, credits, rebates, performance bonus, penalties, sales returns, refunds, price concessions, incentives, etc. The transaction price includes such variable considerations, whether explicitly stated in the contract or implicitly stated.

What is a consideration payable?

Consideration payable to a customer includes cash amounts that an entity pays, or expects to pay, to a customer (or to other parties that purchase the entity's goods or services from the customer).

What is a consideration payment?

Consideration is a payment made by one party to another in exchange for the transfer of something of value. Consideration can include the payment of property, the settlement of an obligation, or forbearance. It must be of value to both parties entering into a transaction.

Which of the following must be met before a contract with a customer is accounted for under Pfrs 15?

Under IFRS 15, a contract is only accounted for by an entity when all of the following requirements are met: The parties to the contract have approved the contract and are committed to perform their respective obligations. The entity can identify each party's rights regarding the goods or services to be transferred.

What are some examples of variable consideration?

Examples of variable consideration include discounts, incentives, rebates, penalties, refunds, contingencies, credits, price concessions, performance bonuses, etc. A company can use either of the following methods for estimating variable consideration – (i.) the expected value method or (ii.) the most likely amount.

Which of the following is an example of variable consideration?

Variable consideration is common and takes various forms, including (but not limited to) price concessions, volume discounts, rebates, refunds, credits, incentives, performance bonuses, milestone payments, and royalties.

What is fixed consideration?

Fixed Consideration means the aggregate sum (a) the Cash Consideration, and (b) the Stock Consideration.

Classification of the different types of consideration paid or payable to a customer

To determine the appropriate accounting treatment, an entity must first determine whether the consideration paid or payable to a customer is a payment for a distinct good or service, a reduction of the transaction price or a combination of both. Consideration paid or payable to a customer

Forms of consideration paid or payable to a customer

Consideration paid or payable to customers commonly takes the form of discounts and coupons, among others. Furthermore, the promise to pay the consideration may be implied by the entity’s customary business practice. Consideration paid or payable to a customer

Consideration paid or payable to a customer

Annualreporting provides financial reporting narratives using IFRS keywords and terminology for free to students and others interested in financial reporting. The information provided on this website is for general information and educational purposes only and should not be used as a substitute for professional advice. Use at your own risk.

What is consideration payable to a customer?

Consideration payable to a customer. If the consideration paid or payable to a customer is a discount or refund for goods or services provided to a customer, ...

What are some examples of consideration paid to a customer?

Many consumer products entities make payments to their customers. Common examples of consideration paid to a customer include: Consideration payable to a customer. In addition, some entities make payments to the customers of resellers or distributors that purchase directly from them. For example, manufacturers of breakfast cereals offer coupons ...

Why does an entity conclude that the payment to the customer is not in exchange for a distinct good or service that transfers

This is because the entity does not obtain control of any rights to the customer’s shelves and the shelving is of no value to the entity absent the revenue relationship.

How to determine appropriate accounting treatment?

To determine the appropriate accounting treatment, an entity must first determine whether the consideration paid or payable to a customer is a payment for a distinct good or service, a reduction of the transaction price or a combination of both. In order for an entity to treat its payment to a customer as something other than a reduction ...

What is a one year contract?

Example. A consumer goods manufacturer enters into a one-year contract to sell goods to a large retail company. The customer commits to buy at least $250,000 of products during the year. The contract also requires the entity to make a non-refundable payment of $25,000 to the customer at the inception of the contract.

Is consideration payable a receivable?

Consideration payable to a customer, this is a payable to the customer not a receivable from the customer (just because otherwise I get confused) – When determining the transaction price, an entity should consider the effects of all of the following: (1) variable consideration; (2) a significant financing component (i.e., the time value of money); (3) non-cash consideration; and#N#(4) consideration payable to a customer.

What is consideration payable to a customer?

606-10-32-25 (IFRS 15 – Paragraph 70) Consideration payable to a customer includes cash amounts that an entity pays, or expects to pay, to the customer (or to other parties that purchase the entity's goods or services from the customer). Consideration payable to a customer also includes credit or other items (for example, a coupon or voucher) that can be applied against amounts owed to the entity (or to other parties that purchase the entity's goods or services from the customer). An entity shall account for consideration payable to a customer as a reduction of the transaction price and, therefore, of revenue unless the payment to the customer is in exchange for a distinct good or service (as described in paragraphs 606-10-25-18 through 25-22) that the customer transfers to the entity. If the consideration payable to a customer includes a variable amount, an entity shall estimate the transaction price (including assessing whether the estimate of variable consideration is constrained) in accordance with paragraphs 606-10-32-5 through 32-13.

When does an entity promise to pay consideration to a customer?

However, in some cases, an entity promises to pay consideration to a customer only after it has satisfied its performance obligations and, therefore, after it has recognized revenue. When this is the case, a reduction in revenue should be recognized immediately.

What is the interpretation of the guidance?

Potential interpretations of the guidance include the following: Interpretation A: Entities must consider all consideration paid or payable to a customer and assess whether such amounts are paid for a distinct good or service and if so, whether the amounts exceed fair value of that good or service.

What is BC255 payment?

BC255 refers to payments an entity makes to"its customers or to its customer's customer (for example, an entity may sell a product to a dealer or distributor and subsequently pay amounts to or provide a cash incentive to a customer of that dealer or distributor).

What is a valid expectation arising from an entity's customary business practices, published policies, or specific statements

The customer has a valid expectation arising from an entity's customary business practices, published policies, or specific statements that the entity will accept an amount of consideration that is less than the price stated in the contract. That is, it is expected that the entity will offer a price concession.

Who makes incentive payments to the principal?

The agent may make incentive payments to parties that purchase the principal's good or service. In many cases, these incentives are not part of the contract with the principal, or a promise made explicitly or implicitly to the principal; although, the principal may be aware of the incentive program.

Does the standard state that consideration payable to a customer should be applied at the contract level?

The standard does not explicitly state whether the guidance on consideration payable to a customer should be applied at the contract level (that is, only to individual contracts or contracts that are required to be combined) or more broadly to the entire "customer relationship.".

What is considered payable to a customer?

Consideration payable to a customer also includes credit or other items (for example, a coupon or voucher) that can be applied against amounts owed to the entity (or to other parties that purchase the entity’s goods or services from the customer).

Does the new revenue standard state that some payments are excluded from the assessment?

The new revenue standard also does not state that some payments are excluded from the assessment. Stakeholders have identified three different interpretations on the scope of the consideration payable to a customer guidance: