What are the steps in the recording process?

- Output location. If you don't want to be prompted for a location and file name every time you save a file, select Browse to set a default location and file ...

- Enable screen capture. ...

- Number of recent screen captures to store. ...

What is the process of recording business transactions?

Recording business transactions is the process of entering business events into the accounting system, which is more common and very automated now, or accounting books. By recording transactions, we translate business transactions into accounting records. Accountants follow a three steps methodology in recording transactions: Understand the business transaction;

What are the 8 steps of the accounting process?

Accounting cycle is the sequence of accounting procedures to record, classify and summarize accounting information. 10 Steps of Accounting Cycle are; (1) Classify transactions, (2) Journalizing them, (3) Post to Ledger, (4) Unadjusted Trial Balance, (5) Adjusting Entries, (6) Adjusted Trial Balance, (7) Financial Statements, (8) Closing Entries, (9) Closing Trial Balance, (10) Recording ...

What is the recording process?

The Recording Process Explained

- Composition. Composition is really where a song or piece is born. ...

- Arrangement. Arranging is taking the Composition that has been created and determining what instruments will be used for the recording, writing the parts that those instruments will play, and the ...

- Recording. ...

- Editing. ...

- Mixing. ...

- Mastering. ...

What are the basic step in recording process?

Answer and Explanation: The recording process has three basic steps as identification, recording, and classification: Identifying: The first step in the recording process requires identifying the impact of transactions on the accounts.

What is recording process of the business?

The steps in the accounting cycle are: Organize transactions. Record journal entries. Post journal entries to the general ledger. Run an unadjusted trial balance.

What are the four steps in the recording process?

The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance.

Why is the recording process important in accounting?

You need good records to prepare accurate financial statements. These include income (profit and loss) statements and balance sheets. These statements can help you in dealing with your bank or creditors and help you manage your business.

What is the difference between recording and reporting?

The distinction between record and report as verbs is that record means "to keep a record of information," but report means "to tell details of (an occurrence or incident); to recount, describe" (something).

What are the processes of accounting?

The 8 Steps of the Accounting CycleStep 1: Identify Transactions. ... Step 2: Record Transactions in a Journal. ... Step 3: Posting. ... Step 4: Unadjusted Trial Balance. ... Step 5: Worksheet. ... Step 6: Adjusting Journal Entries. ... Step 7: Financial Statements. ... Step 8: Closing the Books.

What is the process of recording in the ledger?

Recording of transaction in ledger is called as Posting.

What are the three 3 basic processes of accounting?

Three fundamental steps in accounting are:Identifying and analyzing the business transactions.Recording of the business transactions.Classifying and summarising their effect and communicating the same to the interested users of business information.

What is the correct order of recording the transactions?

Answer and Explanation: The correct answer is option b. Journal, ledger, trial balance, financial statements.

What are the three importance of record keeping?

Per the IRS, good records will help with the following: Monitor the progress of your business. Prepare your financial statements. Identify source of receipts.

Why is recording information important?

Good recordkeeping helps you to conduct better business. Good recordkeeping can be your proof that you have made considered decisions and taken appropriate actions. Records become your protection if you are questioned or challenged. Without them, you are at risk.

Why do we record transactions?

The main reason for recording transactions is to ensure you are charging and being charged accurately. Nobody ever wants unwanted costs and this includes your customers. If you are paying fixed monthlies or one time payments, transactions should never be more than what you expect.

What is the process of recording business transactions in a journal?

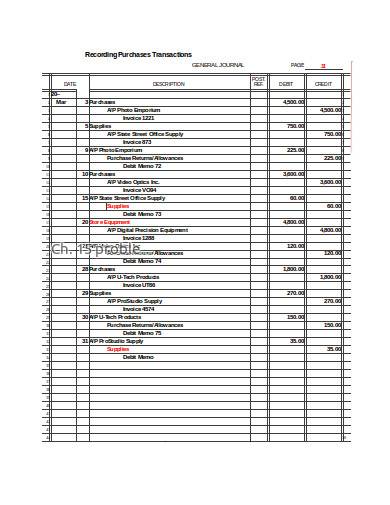

Journalizing is the process of recording a business transaction in the accounting records. This activity only applies to the double-entry bookkeeping system.

How often does the recording process occur in accounting?

Recording process should occur repeatedly during the accounting period in order to represent the information on periodic basis through which corrective actions can be taken and performance can be improved.

What do you call the process of recording transactions in a journal?

4) Recording of a transaction in Journal is called posting.

What are the records used in accounting cycle?

The key steps in the eight-step accounting cycle include recording journal entries, posting to the general ledger, calculating trial balances, making adjusting entries, and creating financial statements.

What is the recording process?

The recording process is the whole process that goes on in maintaining a financial statement. From the very starting to the final destination of the statement, the recording process involves various steps that are to be taken to maintain a good and proper account. These steps are nine in number and help to remove all the flaws from ...

What is the accounting process of a transaction?

Every accounting process of a transaction starts with identifying and analyzing. Under this process, all the important transactions that pertain to a business entity are recorded. Every transaction is identified as to relate to a business entity.

What is the fifth step in accounting?

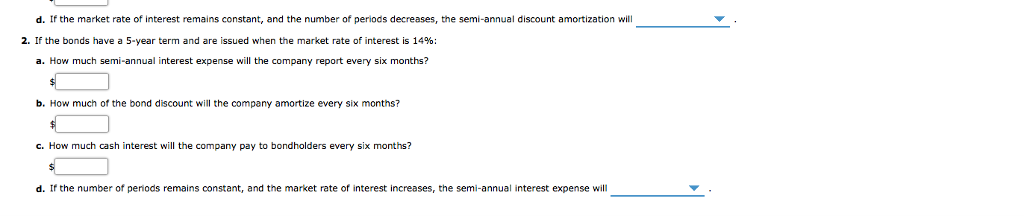

The fifth step involving in a recording process is the step of adjusting the entries of a transaction. It is prepared as an application of the real basis of the accounting. Many of the times, at the end of the accounting period various expenses, are incurred that have not been recorded in the journals.

What is the tail end of a business transaction?

After all the adjustments of the trial balances and several entries comes the step of preparing a financial statement of the transaction. When the accounts are being checked of the flaws and the balance of the debits and the credits is ensured, the financial statement is prepared. The financial statement is the tail end of a business transaction.

What is a ledger in accounting?

A ledger is nothing but a collection of accounts that present the changes made in each account, as a result, of past transactions and their existing balances. The ledgers are also known as the “Books, of final entry.’. This is the most important step in the recording process of the transaction.

Why is maintaining a fine account important?

Maintaining proper and fine accounts has become very essential today, as a result, of increasing complementation in the business-world. Every business organization is, therefore, supposed to maintain fine accounts comprising of all the financial transactions, financial as well as nonfinancial information.

What is the complete chain of forming a proper business transaction and financial statement called?

This complete chain of forming a proper business transaction and financial statement in called as a recording process.

Receiving transaction related documents

As a bookkeeper in a business, he or she will be receiving a document or an online mean of communication related to cash deposit, or an invoice/receipt from a purchase/sale.

Identifying the transaction

The next step is to verify that these are relevant files. Are they signed? Stamped? Is the email valid?

Recording

After identifying the transaction now it is time to record it on the system. The knowledge of the debits and credits in accounting is necessary here. Especially in an organisation that record their transactions manually.

Reporting and Presentation

Most software and even excel sheets have an auto generated financial statements which includes income statements, balance sheets, and cashflow statements. If you want to know about these statements you can visit one of our posts on this link.

Final Thoughts

Basically the above was a simplified steps in recording process in accounting.

What Are Accounting Records?

Accounting records are all of the documentation and books involved in the preparation of financial statements or records relevant to audits and financial reviews. Accounting records include records of assets and liabilities, monetary transactions, ledgers, journals, and any supporting documents such as checks and invoices .

What happens to accounting records during a business cycle?

At different points in the economic or business cycle, parties demanding accounting records will alter their request for information based on the position in a cycle. For instance, at the start of an upswing in a business cycle, requests for financial statements might be strong, as equity investors are bullish. In contrast, during a dip in a business cycle, creditors might require more details surrounding balance sheet items, as they become more hesitant to extend credit.

How long do accounting firms need to keep records?

Rules and laws are generally in place to force accounting entities and accounting firms to retain accounting records for a specified period of time. In the U.S., the Securities and Exchange Commission (SEC) requires that accounting firms retain records from audits and reviews for at least seven years and that they retain any records that support or cast doubt on the conclusions of an audit.

What is financial statement?

The financial statement is the final piece of document that comprises the components of all the other accounting documents. The financial statements are what will be provided to the public and to regulatory bodies for viewing.

Why are accounting records and even methods of accounting continuously evolving?

In short, accounting records and even methods of accounting are continuously evolving to keep pace with the changing nature of business and the information demands of interested market participants.

What is transaction in accounting?

The transaction is the starting point for any accounting record. It is the catalyst for the entire process that shows any item bought or sold, depreciated, etc., that a business transacts.

Do creditors need more details on balance sheet?

In contrast, during a dip in a business cycle, creditors might require more details surrounding balance sheet items, as they become more hesitant to extend credit.

What is the accounting process?

Accounts contain records of changes to assets, liabilities, shareholders' equity, revenues and expenses. The usual sequence of steps in the recording process includes analysis, preparation of journal entries and posting these entries to the general ledger. Subsequent accounting processes include preparing a trial balance ...

How to record a transaction?

The first step in the recording process is to analyze the transaction, determine the accounting entries and record them in the appropriate accounts. The analysis includes an examination of the paper or electronic record of the transaction, such as an invoice, a sales receipt or an electronic transfer. Common transactions include sales of products, delivery of services, buying supplies, paying salaries, buying advertising and recording interest payments. In accrual accounting, companies must record transactions in the same period they occur, whether or not cash changes hands. Revenue and expense transactions affect the corresponding income statement accounts, as well as balance sheet accounts. Some transactions may affect only the balance sheet accounts.

What is the third step in the recording process?

The third and final step in the recording process is to post the journal entries to the general ledger, which contains summary records of all accounts. Each record has fields for transaction date, comments, debits, credits and outstanding balance. In the earlier sales transaction example, the posting process involves entering a credit amount for the sales account, a debit amount for the cash account and updating the respective balances. The general ledger may be in the form of a binder, index cards or a software application.

What are the steps of posting in accounting?

What Are the Five Steps of Posting in Accounting? Accounting is the recording, analysis and reporting of events that are materially significant to a company. Accounts contain records of changes to assets, liabilities, shareholders' equity, revenues and expenses.

What are the common transactions in accounting?

Common transactions include sales of products, delivery of services, buying supplies, paying salaries, buying advertising and recording interest payments. In accrual accounting, companies must record transactions in the same period they occur, whether or not cash changes hands.

What is a journal entry?

Journal entries are the second step in the recording process. A journal is a chronological record of transactions. An entry consists of the transaction date, the debit and credit amounts for the appropriate accounts and a brief memo explaining the transaction. For example, the journal entries for a cash sales transaction are to credit (increase) ...

What is the most basic method used to record a transaction?

Journal entries. The most basic method used to record a transaction is the journal entry, where the accountant manually enters the account numbers and debits and credits for each individual transaction. This approach is time-consuming and subject to error, and so is usually reserved for adjustments and special entries.

What is receipt of invoice?

Receipt of supplier invoices. When a supplier invoice is received, the accountant logs it into the accounts payable module in the accounting software. The module automatically creates a journal entry that debits the relevant expense or asset account, and credits the accounts payable liability account.

What is payroll journal entry?

The module automatically creates a journal entry that debits the compensation and payroll tax expense accounts, and credits cash. This can be quite a complex entry, since it may also address garnishments and other deductions, and separately record several types of payroll taxes.

When are revenues and expenses recorded in accounting?

In the accrual basis of accounting, the revenues and expenses are recorded in the books of the entity in the period when they are earned and incurred respectively, regardless of the actual cash receipt and payment. However, in the case of cash accounting, the transactions are recorded only when the actual cash is received/paid.

What are the Steps in the Accounting Process?

The accounting process is the series of steps followed by the business entity to record the business financial transactions that include steps for collecting, identifying, classifying, summarizing and recording of the business transactions in the books of accounts of the company so that the financial statements of the entity can be prepared and the profits and the financial position of the business can be known after regular intervals of time.

What is profitability in accounting?

After all the above steps are completed, the financial statements of the company are prepared to know the actual financial position, the profitability#N#Profitability Profitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs. It is measured using specific ratios such as gross profit margin, EBITDA, and net profit margin. It aids investors in analyzing the company's performance. read more#N#position, and the cash flow position of the business. The statements that are prepared for knowing the above positions are a statement of profit and loss for knowing the profitability position, the balance sheet for getting the financial position, and the cash flow statement#N#Cash Flow Statement Statement of Cash flow is a statement in financial accounting which reports the details about the cash generated and the cash outflow of the company during a particular accounting period under consideration from the different activities i.e., operating activities, investing activities and financing activities. read more#N#to know the changes in cash flows#N#Cash Flows Cash Flow is the amount of cash or cash equivalent generated & consumed by a Company over a given period. It proves to be a prerequisite for analyzing the business’s strength, profitability, & scope for betterment. read more#N#from the three activities of the business (operating, investing and financing activities).

What is temporary account?

The temporary accounts are the accounts whose balances ends in a single accounting year such as sales, purchases, expenses, etc. These balances are first transferred to the income statement and then to the permanent account, i.e., the profit/loss is transferred to retained earnings.

What is the first step in accounting?

Identifying the business transaction is the initial step in the process of accounting. The business entity has to identify financial and monetary transactions. Therefore, only those transactions that are monetary is recorded. Also, the transactions that belong to the business are to be recorded, and not the personal transactions ...

When is accrual basis used in accounting?

When the accrual basis of accounting is followed, some of the entries are to be made at the end of the accounting year, such as entries of expenses that may have been incurred but are not booked in the Journal and entries of some income that may be earned by the business but are not yet recorded in the books. For example, the interest amount on a fixed deposit is earned each year, but it is accumulated in the fixed deposit amount. This interest income is to be recorded in the books of accounts yearly because the interest is earned yearly, no matter the amount will be received together after the maturity of the fixed deposit.

When is a trial balance to be prepared?

After all the adjusting entries are made, again, a trial balance is to be prepared before preparing the financial statements to check that all the credits are equal to the debits after the adjustment entries are made.

What are the Steps in the Accounting Process?

The accounting process is three separate types of transactions used to record business transactions in the accounting records. This information is then aggregated into financial statements. The transaction types are:

What are the steps required for individual transactions in the accounting process?

The steps required for individual transactions in the accounting process are: Identify the transaction. First, determine what kind of transaction it may be. Examples are buying goods from suppliers, selling products to customers, paying employees, and recording the receipt of cash from customers. Prepare document.

What is the first transaction type?

The transaction types are: The first transaction type is to ensure that reversing entries from the previous period have, in fact, been reversed. The second group is comprised of the steps needed to record individual business transactions in the accounting records. The third group is the period-end processing required to close ...

Where is a business transaction recorded?

Every business transaction is recorded in an account in the accounting database, such as a revenue, expense, asset, liability, or stockholders' equity account. Identify which accounts are to be used to record the transaction. Record the transaction. Enter the transaction in the accounting system.

What is the third group in accounting?

The third group is the period-end processing required to close the books and produce financial statements.

Does accounting software create trial balances?

In reality, any accounting software package will automatically create all versions of the trial balance and the financial statements, so the actual steps in the accounting process may be considerably reduced. Instead, the steps used in a computerized environment are likely to be: Prepare financial statements.