How do I ask for a good faith estimate?

Make sure your health care provider gives you a Good Faith Estimate in writing at least 1 business day before your medical service or item. You can also ask your health care provider, and any other provider you choose, for a Good Faith Estimate before you schedule an item or service.

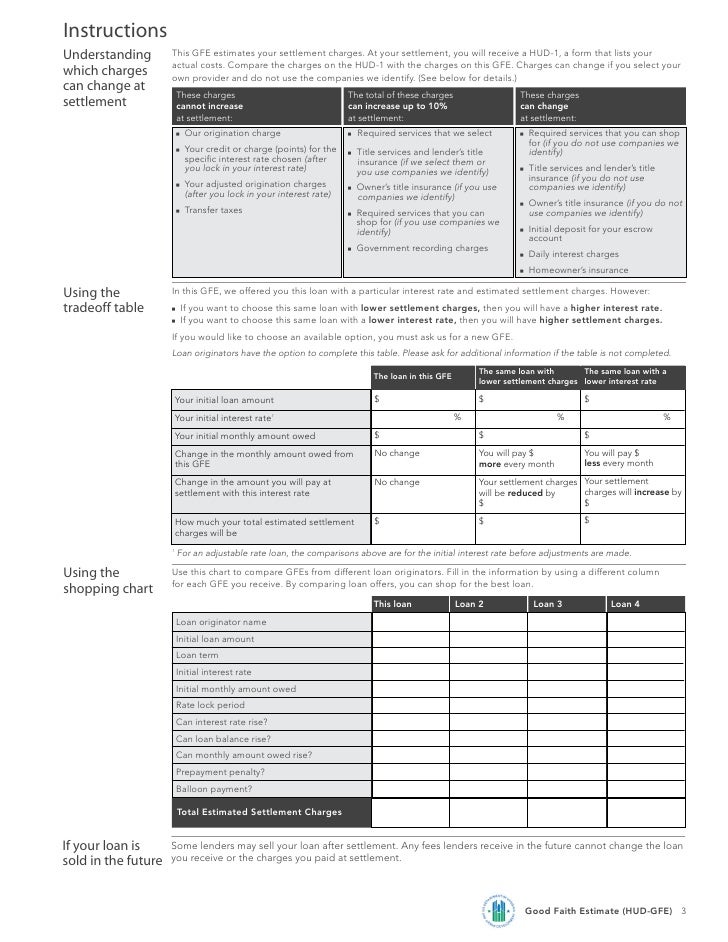

What is a good faith estimate (GFE) for a loan?

If you applied for a loan before that date, or you’re applying for a reverse mortgage, you will receive a GFE. Lenders are required by law to give you the Good Faith Estimate (GFE) within three business days of receiving the loan application. This will explain your loan terms and costs associated with the loan.

Is the lender’s good faith estimate more accurate?

The lender’s good faith estimate should be more accurate than a mortgage broker’s GFE, but some numbers are likely to change. For example, third-party fees on the GFE, such as the title company fees, could change because the title company you use for closing charges different fees.

How do I get an estimate of the cost of services?

The cost of services depends on a number of factors including your provider’s fee, frequency of services, and duration of treatment. You can receive an estimate of service costs as described below. Make sure your health care provider gives you a Good Faith Estimate in writing at least 1 business day before your medical service or item.

What disclosure replaces the Good Faith Estimate?

The Loan Estimate combines and replaces the Good Faith Estimate and the initial Truth-in-Lending (TIL) statement. The form highlights the most important elements of the transaction and allows for easy comparisons among competing lenders.

What replaced the HUD-1 in all conforming loan closing?

Your Closing Disclosure is one of the most important pieces of paperwork you'll receive during the mortgage process, so check it over carefully. In August 2015, under the direction of the Consumer Financial Protection Bureau (CFPB), the Closing Disclosure Form replaced the HUD-1 settlement statement.

Is a Good Faith Estimate the same as a closing disclosure?

On October 15, 2015, the GFE was replaced by the Loan Estimate and Closing Disclosure Form. The GFE outlines all of the costs of your mortgage loan, including your loan amount, term, interest rate, whether there is a prepayment penalty, origination charge, and more.

Is a Good Faith Estimate the same as a loan estimate?

A Loan Estimate (LE) is a standard document you'll receive when you apply for a mortgage with any lender. This document used to be called a “Good Faith Estimate,” but was updated in 2015. The new version, called a “Loan Estimate,” is easier to read and a more useful tool for loan shoppers.

What is the HUD-1 called now?

Now, for most kinds of mortgage loans, borrowers receive a form called the Closing Disclosure instead of a HUD-1 form.

Is a HUD-1 still used?

The HUD-1 Settlement Statement is a standard government real estate form that was once used by settlement agents, also called "closing agents," to itemize all charges imposed upon a borrower and seller for a real estate transaction. The statement is no longer used, with one exception: reverse mortgages.

What is the GFE called now?

Loan Estimate formIn 2015, the Consumer Financial Protection Bureau (CFPB) launched the Know Before You Owe mortgage initiative to ensure that all consumers have the information they need in order to make informed decisions. As part of the initiative, CFPB retired the Good Faith Estimate and replaced it with the Loan Estimate form.

When should a lender give you a Good Faith Estimate?

within three business daysThe lender must provide you with a GFE within three business days of receiving your application or other required information. You can be charged a credit report fee before receiving a GFE. But, you can't be charged any other fees until you get the GFE and indicate that you want to proceed with the mortgage loan.

Does Good Faith Estimate need to be signed?

The No Surprises Act doesn't require your client to sign the Good Faith Estimate. However, you still have to note in their medical record that you gave it to them and they received it.

What two federal forms are replaced by the loan estimate form?

The Rule replaces the Good Faith Estimate (GFE) and early TILA form with the new Loan Estimate. It also replaces the HUD-1 Settlement Statement and final TILA form with the new Closing Disclosure.

Is loan estimate and closing disclosure the same?

After choosing a lender and running the gantlet of the mortgage underwriting process, you will receive the Closing Disclosure. It provides the same information as the Loan Estimate but in final form. This means that it contains the locked-in costs of your loan and the specific amount you'll need to pay at closing.

What's the relationship between TILA RESPA and Trid?

The TRID (TILA-RESPA Integrated Disclosure) rule took effect in 2015 for the purpose of harmonizing the Real Estate Settlement Procedures Act (RESPA) and Truth in Lending Act (TILA) disclosures and regulations. The rule has been amended twice since the initial issue, most recently in 2018.

Which of the following statements best defines what is included in a closing disclosure?

Which of the following statements best defines what is included in a Closing Disclosure? A Closing Disclosure details all financial particulars of a transaction.

Is a loan estimate the same as a preapproval?

Receiving a Loan Estimate from a lender isn't the same thing as receiving an approval on a loan. Instead, the Loan Estimate shows the details of the loan that the lender expects to offer you should you decide to move forward. After you decide to proceed, your lender will ask for additional financial information.

How accurate is a good faith estimate?

An analysis of new research suggests that, contrary to the views of some observers, the Good Faith Estimate disclosure has been an accurate predictor of actual mortgage closing costs.

Which of the following disclosures must be given within 3 business days of receiving an application?

Disclosure of good faith estimate of costs must be made no later than 3 days after application. This means that a creditor must deliver or mail the early disclosures for all mortgage loans subject to RESPA no later than 3 business days (general definition) after the creditor receives a consumer's application.

Receiving A Good Faith Estimate

Lenders are required by law to give you the Good Faith Estimate (GFE) within three business days of receiving the loan application. This will expla...

What Type of Fees Are in A GFE?

The Good Faith Estimate (GFE) will outline all of the fees you should expect to pay for your mortgage. The fees in the GFE will include: 1. Applica...

New Disclosures For Mortgages After October 3, 2015

For most new loans, the Good Faith Estimate no longer applies. Effective October 3, 2015, the U.S. government made significant revisions to the rat...

How long does it take to get a good faith estimate?

Receiving a good faith estimate. Lenders are required by law to give you the Good Faith Estimate (GFE) within three business days of receiving the loan application. This will explain your loan terms and costs associated with the loan. The GFE must be mailed or hand-delivered by the end of the third day.

Why do third party fees on GFE change?

For example, third-party fees on the GFE, such as the title company fees, could change because the title company you use for closing charges different fees. The lender’s fees on the GFE may be more accurate because they know their own fees, but these fees can fluctuate. So be prepared for any fees to increase.

What is a GFE?

A GFE, also referred to as a good faith estimate, is a document that includes the breakdown of approximate payments due upon the closing of a mortgage loan. A GFE helps borrowers shop and compare costs of loans with lenders. You are not obligated to accept the loan just because you received a GFE. Smart mortgage shoppers apply for at least two loans and use the GFE’s to determine which lender to use.

What type of fees are in a GFE?

The Good Faith Estimate (GFE) will outline all of the fees you should expect to pay for your mortgage. The fees in the GFE will include:

What are the fees for a mortgage?

The GFE outlines all of the costs of your mortgage loan, including your loan amount, term, interest rate, whether there is a prepayment penalty, origination charge, and more. In the fees outlined in the GFE, some fees are paid by the buyer and some by the seller. The charges fall into these categories: 1 Loan fees 2 Fees to be paid in advance 3 Reserves or escrow paid to third parties 4 Title charges 5 Government charges 6 Additional charges

When was the GFE replaced?

On October 15, 2015, the GFE was replaced by the Loan Estimate and Closing Disclosure Form. The GFE outlines all of the costs ...

What is an appraisal fee?

Appraisal Fee: Pays for an independent appraisal of the home’s value, which is not the same as the home inspection.

AOA offers resources, guidance on GFE compliance

Although the HHS has indicated some enforcement discretion in 2022, the AOA emphasizes that doctors of optometry must familiarize themselves with the GFE requirements.

Learn more about the No Surprises Act

Access the AOA’s newly updated guidance on the No Surprises Act and how it applies to optometry practices, including the good faith estimates requirement.