How to calculate Cost allocation?

- Add up total overhead.

- Compute the overhead allocation rate by dividing total overhead by the number of direct labor hours.

- Apply overhead by multiplying the overhead allocation rate by the number of direct labor hours needed to make each product.

How do you calculate allocation base?

How do you calculate allocation base? Therefore, 1,400 direct labor hours divided by 3,000 direct labor hours equals an allocation base of about 46 percent for Product A. Then 1,600 direct labor hours divided by 3,000 direct labor hours equals an allocation base of about 54 percent for Product B. Multiply the total cost by the allocation base.

How do you define the cost allocation system?

Types of Cost Allocation

- Direct Costs. Direct costs are the easiest to assign to an identified cost object, because they are directly related.

- Indirect Costs. When you have an indirect cost, it is not attached to a specific cost object but still is necessary for the business to function.

- Overhead Costs. ...

What are the different types of cost allocation systems?

Types of Cost Allocation Methods for Government Contractors

- Indirect Cost Basics. Indirect costs cover a wide range of expenses incurred for multiple cost objectives. ...

- Allocation Requirements and Method. The aim of indirect cost allocation is to work out the proportion of non-direct expenses that each project will bear.

- Overhead Pool. ...

- G&A Pool. ...

- Fringe Pool. ...

- Facilities Pool. ...

How do you determine cost allocation?

If the auditor's cost is based on the Total Revenue of the organization, then you would divide the total revenue of this program by the total organizational revenue, to calculate the allocation percentage for that cost.

How do you choose cost allocation base?

The allocation base should be a cause, or driver, of the cost being allocated. A good indicator that an allocation base is appropriate is when changes in the allocation base roughly correspond to changes in the actual cost. Thus, if machine usage declines, so too should the actual cost incurred to operate the machine.

What is cost allocation used for?

Cost allocation is the method business owners use to calculate profitability for the purpose of financial reporting. To ensure the business's finances are on track, costs are separated, or allocated, into different categories based on the area of the business they impact.

What is the main reason of cost allocation?

Cost allocation provides the management with important data about cost utilization that they can use in making decisions. It shows the cost objects that take up most of the costs and helps determine if the departments or products are profitable enough to justify the costs allocated.

What are the three methods of cost allocation?

C. There are three methods commonly used to allocate support costs: (1) the direct method; (2) the sequential (or step) method; and (3) the reciprocal method.

What are common allocation bases?

Common allocation bases are direct labor hours, direct labor costs, and machine hours.

What are the four steps in the cost allocation process?

There are four major steps to allocating expenses:Determine program services and supporting activities. ... Determine direct and indirect expenses. ... Determine proper allocation methods for indirect expenses. ... Apply allocation methods to indirect expenses.

What is the allocation method?

The benefit allocation method sets aside the money contributed by employer and employee into a fund that is invested to pay the benefit down the line. By contrast, a cost allocation method estimates the overall cost of benefits that will be owed and sets aside that amount.

What is the process of allocation?

An allocation is the process of shifting overhead costs to cost objects, using a rational basis of allotment. Allocations are most commonly used to assign costs to produced goods, which then appear in the financial statements of a business in either the cost of goods sold or the inventory asset.

What are four purposes for cost allocation?

The four main purposes for allocating costs are to predict the economic effects of planning and control decisions, to motivate managers and employees, to measure the costs of inventory and cost of goods sold, and to justify costs for pricing or reimbursement.

Which allocation method is best?

The best method for allocating overhead in construction is a way that's fair. After all, the idea is to allocate (or, distribute) costs that each job shares responsibility for — meaning the job either caused or benefited from the cost. But, the costs should also be proportional to that responsibility.

What is a cost allocation plan?

• A cost allocation plan is a written summary which shows how an organization allocates costs. between two or more programs. • An organization often has several allocation plans based on type of expenditure or how the. expenditure is being used. • There are many ways to allocate expenses.

Which allocation method is best?

The best method for allocating overhead in construction is a way that's fair. After all, the idea is to allocate (or, distribute) costs that each job shares responsibility for — meaning the job either caused or benefited from the cost. But, the costs should also be proportional to that responsibility.

What are the four cost allocation methods?

When allocating costs, there are four allocation methods to choose from.Direct labor.Machine time used.Square footage.Units produced.

What is cost allocation base?

A cost allocation base is a strategy that is used while identifying the most reasonable means of assigning or allocating cost to specific cost objects. A cost object may be a project, a department, or even a function within a department. By creating a workable base for this assignment of expenses in a fashion that is in keeping with generally accepted accounting principles, it is possible to create a cost allocation base that takes into account the number of cost objects involved and how certain types of expenses are to be allocated among those objects. As with the process of cost allocation itself, the object is not necessarily to assign specific amounts of costs but to determine where to allocate those cost types to best effect.

Why is cost allocation important?

One of the chief benefits of identifying a cost allocation base is that the process helps to provide greater understanding into the types of costs involved with specific activities or functions within the company’s operational structure. The data that is compiled in order to make use of the base can often help identify areas of the operation in which some improvement in the general operational processes could benefit the business over time. From this perspective, a balanced and well-planned cost allocation base serves as the framework for evaluating expenses as well as assigning them in a logical manner.

What is cost allocation?

Cost allocation means the direct distribution of the cost heads to various departments based on a reasonable factor. It is a type of cost apportionment which allocates a cost to a cost object. The distribution is done to a department only when it is connected to a department.

When is allocation done?

Allocation is done in the ratio of benefits expected to be achieved from the cost heads. A cost is apportioned when it is not directly related to a particular department but instead is connected to various departments.

What is apportionment of cost?

On the other hand, apportionment of cost means attribution of various cost heads to departments in proportion, based on a reasonable factor. Allocation is done in the ratio of benefits expected to be achieved from the cost heads. A cost is apportioned when it is not directly related to a particular department but instead is connected to various departments.

Why is it important to keep track of the cost incurred in each department?

It becomes vital to keep track of the cost incurred in each department to fix accountability and maintain control over costs.

What is cost pool?

Cost pools are the elements of cost for which allocation is to be done based on cost drivers. It may include costs such as factory rent, electricity, fuel, labor cost. Labor Cost Cost of labor is the remuneration paid in the form of wages and salaries to the employees. The allowances are sub-divided broadly into two categories- direct labor ...

Why do managers keep a check on costs incurred in their respective departments?

Thus, managers of such departments will keep a check on the costs incurred in their respective departments since they are to be held responsible for any unnecessary expenses incurred.

What is profitability in accounting?

Profitability Profitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs.

What are the functional expenses of a nonprofit?

Per Generally Accepting Accounting Principles, there are four classes of functional expenses for nonprofit organizations: program services, management and general, fundraising, and membership development (uncommon for most nonprofits) . The last three categories are known as “supporting activities”.

What are the categories of expenses on 990?

Only three categories of expenses are present on the 990: program, management and general, and fundraising. So if a nonprofit has any expenses assigned to membership development in its financial statements, it needs to determine a reasonable way of allocating those to the other three categories.

What expenses should be removed from 990?

Some expenses should be removed for functional reporting purposes, and placed on different parts of the 990: Rental expenses (that are associated with rental income activities) Costs of inventory sold. Direct expenses of fundraising events. Gaming expenses.

What is direct versus indirect cost?

Direct versus indirect costs. Direct costs are clearly identified with, or directly related to, a single objective or purpose. They should be directly assigned a functional category; no actual allocation is involved. Indirect costs cannot be clearly identified with, or directly related to, a single objective or purpose.

Do nonprofits have to allocate expenses to 990?

All 501 (c) (3) and (c) (4) nonprofits must allocate expenses to functions in Part IX of the 990 informational return. Generally, the cost allocation system used in the organization’s accounting system can serve as the basis of allocations for 990 purposes. However, there are a few important points to consider:

Is rent an indirect cost?

Here’s a very important distinction: indirect costs are NOT the same as supporting activities. Rent is an indirect cost, but it can be allocated to the program services function. On the other hand, accounting is a direct cost, but it is usually assigned to the management and general category (a supporting activity).

Does cost allocation work?

In conclusion. Any cost allocation method can work and pass muster if it’s rational, consistently applied, and documented. An organization does not need to worry about developing the one true and correct allocation system for its situation because for most nonprofits this simply doesn’t exist.

Purpose

Process

Examples of Cost Allocation

- Thank you for reading CFI’s guide to Cost Allocation. In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: 1. Break-Even Analysis 2. Cost of Production 3. Fixed and Variable Costs 4. Projecting Income Statement Line Items

Difference Between Cost Allocation & Cost Apportionment

Advantages

- Identify the cost object for which the cost is to be allocated. It may include a product, department, project, customer, and so on.

- Establish the cost of poolsCost Of PoolsA cost pool is a strategy to identify the company's individual departments or service sector costs incurred. It determines the total expenses incurred in man...

- Identify the cost object for which the cost is to be allocated. It may include a product, department, project, customer, and so on.

- Establish the cost of poolsCost Of PoolsA cost pool is a strategy to identify the company's individual departments or service sector costs incurred. It determines the total expenses incurred in man...

- Identify the cost driverCost DriverA cost driver is a unit that derives the expenses and sets a basis on which a particular cost is to be allocated between the different departments and on the basi...

Disadvantages

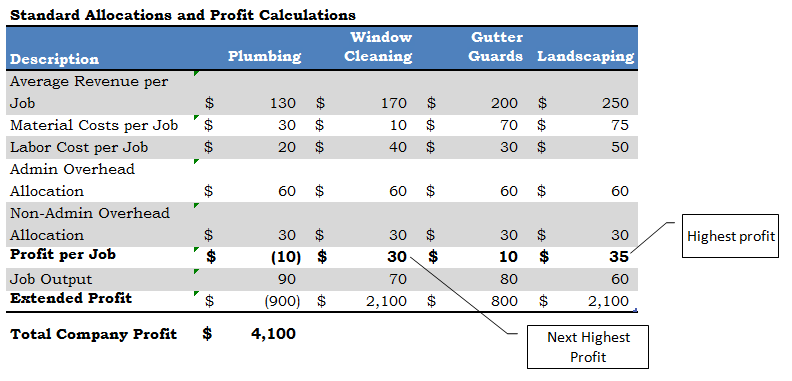

- This process can be understood by way of the following example. A company produces two products, namely “A” and “B” on the premises of the same factory. 1. Factory Rent = $1,00,000 2. Units Produced of “A” = 30,000 3. Units Produced of “B” = 20,000 4. Total no. of units produced = 50,000 Let us see how can the cost allocation of factory rent be done for the two products. Here…

Conclusion

- Cost allocation means the direct distribution of the cost heads to various departments based on a reasonable factor. It is a type of cost apportionment which allocates a cost to a cost objectA Cost...

- On the other hand, apportionment of cost means attribution of various cost heads to departments in proportion, based on a reasonable factor. Allocation is done in the ratio of be…

- Cost allocation means the direct distribution of the cost heads to various departments based on a reasonable factor. It is a type of cost apportionment which allocates a cost to a cost objectA Cost...

- On the other hand, apportionment of cost means attribution of various cost heads to departments in proportion, based on a reasonable factor. Allocation is done in the ratio of benefits expected to...

Recommended Articles

- When a company follows cost allocation for its various departments, each department tries to maintain efficiency in its operations and keep the cost under control.

- It helps in determining the actual cost of a product produced or a service rendered.

- It enables a company to fix accountability on the various departments regarding the cost that is incurred by them.

- When a company follows cost allocation for its various departments, each department tries to maintain efficiency in its operations and keep the cost under control.

- It helps in determining the actual cost of a product produced or a service rendered.

- It enables a company to fix accountability on the various departments regarding the cost that is incurred by them.

- It is helpful in decision making as it can provide information as to what is the actual cost, which can be compared with the revenuesRevenuesRevenue is the amount of money that a business can earn...