Why is there a difference between absorption and variable costing?

Key Takeaways Absorption costing differs from variable costing because it allocates fixed overhead costs to each unit of a product produced in the period. Absorption costing allocates fixed overhead costs to a product whether or not it was sold in the period.

What is the difference between absorption costing and variable costing quizlet?

Terms in this set (9) What is the difference between full absorption costing and variable costing? In full absorption costing, fixed manufacturing overhead is included in the cost of the product. In variable costing, fixed manufacturing overhead is expensed.

What is the difference between absorption costing and variable costing If variable costing is not GAAP Why do businesses use it?

The only difference between absorption costing and variable costing is in the treatment of fixed manufacturing overhead. Using absorption costing, fixed manufacturing overhead is reported as a product cost. Using variable costing, fixed manufacturing overhead is reported as a period cost.

What is the difference between variable and full costing?

The full costing is the collecting of data and presentation of propositions for the business, while the variable costs are the expenses in the company for its activities and productions. 2. Full costing is somehow related to the environmental issues, variable costing is more of the expenses of the company.

What is included in variable costing?

Variable costing is a costing method that includes only variable manufacturing costs—direct materials, direct labor, and variable manufacturing overhead—in unit product costs.

How is the use of variable costing limited?

Long-term pricing: Variable costing is not useful for long-term pricing policy simply because it does not consider fixed factory overhead as product cost. Undervaluation of inventory: Under variable . costing, finished goods, and work-inprogress are undervalued.

Why is absorption costing higher than variable costing?

When units produced are greater than units sold, i.e., units in inventory increase, absorption income is greater than variable costing income because absorption costing defers a portion of fixed manufacturing costs in finished goods inventory.

Why do managers prefer variable costing over absorption costing?

As opposed to "absorption costing," which is a system that considers all manufacturing costs for reporting purposes, many managers argue that variable costing is more effective for decision making because this method excludes fixed overhead costs of goods sold.

How do you reconcile variable and absorption costing?

Net income under absorption costing can be reconciled with net income under variable costing by (a) subtracting the manufacturing overheads carried forward (absorbed by closing inventories) and (b) adding the manufacturing overheads brought in (absorbed by opening inventories).

What are the advantages of variable costing?

The advantages of the variable costing Variable costing provides management with data on variable costs and contribution margins needed to make daily decisions on special orders, capacity expansion, and production shutdown.

What is cost absorption?

What Is Absorbed Cost? Absorbed cost, also known as absorption cost, is a managerial accounting method that includes both the variable and fixed overhead costs of producing a particular product. Knowing the full cost of producing each unit enables manufacturers to price their products.

What is the difference between absorption costing and marginal costing?

Treatment of Fixed Costs: Absorption costing includes all costs, both fixed and variable, incurred in the production of a given product. On the other hand, marginal costing generally only considers variable costs. Intended Use: Generally, marginal costing is used in order to determine the costs of production.

Which of the following is not included in absorption costing?

Which of the following is not a "product cost" under absorption costing? Answer C. Variable manufacturing overhead is not a product cost under absorption costing. Variable costing is a different form of accounting for product and inventory costs.

Which cost is not charged to the product under absorption costing?

Fixed manufacturing costs are not charged to the product under variable costing. Fixed manufacturing overhead is a period cost under absorption costing.

What is operating income using variable costing?

A variable costing income statement is one in which all variable expenses are deducted from revenue to arrive at a separately-stated contribution margin, from which all fixed expenses are then subtracted to arrive at the net profit or loss for the period.

What is the unit product cost using variable costing?

2 (a) The unit product cost under variable costing can be determined by subtracting the fixed factory overhead rate per unit from the unit product cost under absorption costing.

What is the difference between absorption and variable costing?

There are different types of costs involved in a manufacturing environment. Particularly, the costs can be identified as variable costs and fixed costs. Absorption costing and variable costing are two different costing approaches used by manufacturing organizations. This difference occurs as absorption costing treats all variable and fixed manufacturing costs as product cost while variable costing treats only the costs that vary with the output as product cost. An organization cannot practice both the approaches at the same time while the two methods, absorption costing and variable costing, carry their own advantages and disadvantages.

What is the similarity between variable and absorb costing?

The similarity between Absorption Costing and Variable Costing is that the purpose of both approaches are the same; to value the cost of a product.

What is Absorption Costing?

Absorption costing, which is also known as full costing or traditional costing, captures both fixed and variable manufacturing costs into the unit cost of a particular product. Therefore, the cost of a product under absorption costing consists of direct material, direct labour, variable manufacturing overhead, and a portion of a fixed manufacturing overhead absorbed using an appropriate base.

What is variable costing?

Variable costing, which is also known as direct costing or marginal costing considers only the direct costs as the product cost. Thus, the cost of a product consists of direct material, direct labour and the variable manufacturing overhead. Fixed manufacturing overhead is considered as a periodic cost similar to the administrative and selling costs and charged against the periodic income.

What are the different types of costs in manufacturing?

There are different types of costs involved in a manufacturing environment. Particularly, the costs can be identified as variable costs and fixed costs. Absorption costing and variable costing are two different costing approaches used by manufacturing organizations.

What is absorption costing?

Absorption costing is a method used by companies and organizations to determine their cost of goods sold. When calculating their COGS through absorption costing, companies often include the cost of materials and labor as well as fixed and variable manufacturing costs. Because companies consider a majority of their expenses when conducting absorption costing, it's often referred to as full costing. Using the absorption costing method often increases the inventory value, which can affect the gross profit and increase the price of products.

What is variable costing?

Variable costing is a method used by companies and organizations that calculate their cost of goods sold by excluding any fixed, direct costs from their calculations. Using this method allows businesses to file their fixed costs under the operating expenses, which can help calculate a slightly higher gross profit. Companies most often use the variable costing method for internal purposes or company decisions and not for official financial reports due to certain accounting regulations.

Why is variable costing important?

Decision making: Variable costing is important for companies because it allows them to make important business decisions more easily. When making financial decisions, it's important to understand the relationship between the fixed costs and the production of the company's goods and services to ensure consumer prices aren't too high and they can generate revenue.

When deciding on which costing method to use, it's helpful to talk with a manager or colleague about?

When deciding on which costing method to use, it's helpful to talk with a manager or colleague about the situation. Discussing why the company is looking to calculate the cost of goods sold can help you determine their major goals and objectives to see which method is most useful. For example, if the company is hoping to provide important information to investors, it might be better to use the absorption costing method. However, if the company was trying to determine if they should change the price of their products, the variable method might be more informative.

How does costing affect financial health?

For example, the absorption costing method doesn' t subtract fixed costs from the revenue until the company sells the products , so it's possible that the absorption method might not provide companies with their true expenses, which can negatively affect their financial and manufacturing decisions.

What is the difference between variable and absorbed cost?

Variable cost is the accounting method in which all the variable production costs are only included in product cost whereas Absorption costing is where all the absorbed costs are taken into account and under this method, all the fixed and variable production costs are deducted and then fixed and variable selling expenses are deducted.

What is absorption costing?

Absorption costing is used to calculate the net profit. Profit. Profit is much easier to predict as it is a function of sales. It is much more difficult to predict the effect of change in sales on profit.

What is overhead cost in absorption costing?

Overhead Costs Overhead cost are those cost that is not related directly on the production activity and are therefore considered as indirect costs that have to be paid even if there is no production.

What is variable costing?

Variable costing is generally used for internal reporting purposes. Managerial decisions are taken on the basis of variable costing. Absorption costing is used for reporting to the external stakeholders as well as for the purpose of filing taxes. It is in line with GAAP.

Is absorption costing the sole method of accounting?

Since absorption costing is to be utilized for external reporting, it may be used as the sole method of accounting. Method Of Accounting Accounting methods define the set of rules and procedure that an organization must adhere to while recording the business revenue and expenditure.

Is variable costing a basis for managerial decisions?

Though variable costing aids in managerial decisions, it should not be the sole basis for managerial decisions. The management should look at different perspectives including looking at absorption costing data. The management should look at consumer insights, relation with buyers, the effect on brand-building, and other factors while taking decisions. While calculating net profit, a manager should look at both costing techniques.

What is the purpose of variable costing?

The information provided by variable costing method is mostly used by internal management for decision making purposes. Absorption costing provides information that is used by internal management as well as by external parties like creditors, government agencies and auditors etc.

Is marketing a period cost?

Note: Marketing and administrative expenses are period costs and are not relevant in the computation of unit product cost.

Is product cost included in absorption costing?

Under absorption costing system, the product cost consists of all variable as well as all fixed manufacturing costs i.e., direct materials, direct labor and factory overhead (FOH). But when variable costing system is used, the fixed cost (both manufacturing and non-manufacturing) is treated as a period or capacity cost and is, therefore, not included in the product cost.

Can variable costing and absorption costing be substituted for one another?

Variable costing and absorption costing cannot be substituted for one another because both the systems have their own benefits and limitations. These costing approaches are known by various names. For example, variable costing is also known as direct costing or marginal costing and absorption costing is also known as full costing ...

Is fixed manufacturing overhead included in variable costing?

Notice that the fixed manufacturing overhead cost has not been included in the unit cost under variable costing system but it has been included in the unit cost under absorption costing system. This is the primary difference between variable and absorption costing.

What is the difference between absorption and variable cost?

The major difference between both methods includes the fixed cost as a part of the total cost. Both methods appeal to different stakeholder groups.

What is Absorption Costing?

The term “absorption costing” describes the method of accounting for a cost that is applied in vertically integrated organizations. It is also referred to as the “all-inclusive” method of accounting for costs.

What is variable costing?

As the name suggests, variable costing is a method of costing that focuses on the product’s variable costs being manufactured.

What is the difference between costing and budgeting?

Costing is a measurement of the actual cost of a product or service. It is a tool that allows an organization to track its costs. Costing and budgeting are two terms that are often used interchangeably. They are different, however, in the way they are used. Costing is a tool that helps you track your expenses. It helps you identify areas where you can reduce costs. Budgeting is the process of estimating the costs of a project or the expenses you expect to incur in the future.

Why does the per unit cost under absorption costing decrease?

Therefore, as we increase the number of units, the per-unit cost under absorption costing will reduce because each extra unit of production will absorb the fixed costs of production.

Why do businesses use variable costs?

This brings uncertainty for management decisions, which is why businesses usually use variable costs for internal decision-making and absorption costing to communicate the costs to various stakeholder groups.

Why is fixed cost not considered a direct contributor to the cost of production?

Because fixed costs remain the same at every production level till the maximum capacity of production is reached. Since the fixed cost does not change with variation in the production units , it is not considered a direct contributor to the cost of production.

What is the difference between absorption and variable costing?

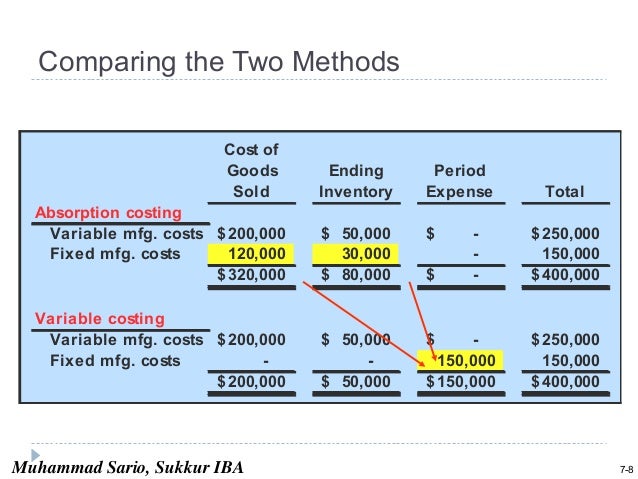

The difference between the absorption and variable costing methods centers on the treatment of fixed manufacturing overhead costs. Absorption costing “absorbs” all of the costs used in manufacturing and includes fixed manufacturing overhead as product costs. Absorption costing is in accordance with GAAP, because the product cost includes fixed overhead. Variable costing considers the variable overhead costs and does not consider fixed overhead as part of a product’s cost. It is not in accordance with GAAP, because fixed overhead is treated as a period cost and is not included in the cost of the product.

How does absorption costing affect sales?

The use of absorption versus variable costing creates more of a timing issue for the recognition of fixed expenses, and this is why net income would vary from period to period under the two methods but in the long run would not. In addition, absorption costing does allow for manipulation of income by managers through overproduction. Increasing production at year-end results in a higher net income than if the additional goods had not been produced, since increasing the number of units decreases the fixed cost per unit. Under absorption costing, these fixed costs follow the units produced and do not become a part of cost of goods sold until they are sold. Instead, a portion of the fixed costs is in the inventory accounts. Why would a manager want to manipulate income by overproducing? If the manager’s annual bonus or other compensation is linked to net income, then the manager may be motivated to overproduce in order to increase the potential for or the amount of a bonus. If the level of sales remain constant while manipulating the production level, such an action would increase the company’s expenses (including the amount of bonus) while not increasing its revenue. Barring any other justification for the increase in production, such an action by the manager would typically be considered an ethical violation, since the manager’s actions would be in the manager’s best interests, but contrary to the best interests of the company.

Why are variable costing statements useful for CVP analysis?

Variable costing statements provide data that are immediately useful for CVP analysis because fixed and variable overhead are separate items. Computations from financial statements prepared with absorption costing need computations to break out the fixed and variable costs from the product costs.

How to tell if sales and production are equal?

Sales and Production equal. When a company sells the same quantity of products produced during the period, the resulting net income will be identical whether absorption costing or variable costing is used. When sales equals production, all manufacturing costs are accounted for in net income, and none of the costs are waiting in finished goods inventory to be recognized in a future period. Remember, with absorption costing, all manufacturing costs are added to the cost of the product during the work in process phase; thus, as the goods are sold, all costs have been accounted for. With variable costing, only the variable costs or production are added to the cost of the product during the work in process phase, and the fixed costs are expensed in the period in which they are incurred. Thus, in the example where sales and production are equal, all costs have been accounted for since all of the produced inventory has moved through cost of goods sold. This means that net income under absorption costing would be the same as net income under variable costing.

Why would management prefer variable costing?

If absorption costing is the method acceptable for financial reporting under GAAP, why would management prefer variable costing? Advocates of variable costing argue that the definition of fixed costs holds, and fixed manufacturing overhead costs will be incurred regardless of whether anything is actually produced. They also argue that fixed manufacturing overhead costs are true period expenses and have no future service potential, since incurring them now has no effect on whether these costs will have to be incurred again in the future.

Why do companies use variable costing?

While companies use absorption costing for their financial statements, many also use variable costing for decision-making. The Big Three auto companies made decisions based on absorption costing, and the result was the manufacturing of more vehicles than the market demanded. Why? With absorption costing, the fixed overhead costs, such as marketing, were allocated to inventory, and the larger the inventory, the lower was the unit cost of that overhead. For example, if a fixed cost of $1,000 is allocated to 500 units, the cost is $2 per unit. But if there are 2,000 units, the per-unit cost is $0.50. While this was not the only reason for manufacturing too many cars, it kept the period costs hidden among the manufacturing costs. Using variable costing would have kept the costs separate and led to different decisions.

What is ABC costing?

ABC costing assigns a proportion of overhead costs on the basis of the activities under the presumption that the activities drive the overhead costs. As such, ABC costing converts the indirect costs into product costs. There are also cost systems with a different approach. Instead of focusing on the overhead costs incurred by the product unit, these methods focus on assigning the fixed overhead costs to inventory.

What is period cost?

Costs that are not a necessary part of the manufacturing process. As a result, period costs cannot be assigned to the products or to the cost inventory.

Is period cost expensed?

In both costing methods they are treated as Period Costs. They are expensed immediately as incurred on the income statement.