The key types of payroll journal entries are:

- Initial recordation. The primary payroll journal entry is for the initial recordation of a payroll. ...

- Accrued wages. There may be an accrued wages entry that is recorded at the end of each accounting period, and which is intended to record the amount of wages owed ...

- Manual payments. ...

How to make a payroll journal entry?

What is the journal entry for payroll accrual? Accrued payroll is entered as a debit entry to record the employee payroll expense, representing the amount of total earnings employees have accumulated for the work they do as of the end of an accounting period.

What are the correct journal entries to record payroll taxes?

Feb 21, 2022 · Accrued Payroll Journal Entry It is quite common to have some amount of unpaid wages at the end of an accounting period, so you should accrue this expense (if it is material). The accrual entry, as shown next, is simpler than the comprehensive payroll entry already shown, because you typically clump all payroll taxes into a single expense account and offsetting …

What are the proper accounting entries for payroll?

Assume a company had a payroll of $35,000 for the month of April. The company withheld the following amounts from the employees’ pay: federal income taxes $4,100; state income taxes $360; FICA taxes $2,678; and medical insurance premiums $940. This entry records the payroll: To record the payroll for the month ended April 30. All accounts credited in the entry are …

What is the journal entry salary paid?

What is the journal entry for accrued payroll? Accrued payroll is entered as a debit entry to record the employee payroll expense, representing the amount of total earnings employees have accumulated for the work they do as of the end of an accounting period. Click to see full answer.

How do you do accrued payroll?

At the end of your accounting month or year, accrue payroll if the wages were earned in one month but paid in another. Note the accrual date and the month and date the wages will be paid. If you do not need to accrue payroll, simply make payroll entries at the end of each pay period, which should match the pay date.

What type of account is accrued payroll?

Accrued payroll is a liability account.

Where does accrued payroll go on the balance sheet?

Accrued wages refers to the amount of liability remaining at the end of a reporting period for wages that have been earned by hourly employees but not yet paid to them. This liability is included in the current liabilities section of the balance sheet of a business.Feb 9, 2022

How do I record accrued payroll in Quickbooks?

To calculate accrued payroll, add together the different sources of liability for each employee. Then, add together all the sums of all the employees for a given pay period.Jul 28, 2021

What are Payroll Journal Entries?

Payroll journal entries are used to record the compensation paid to employees. These entries are then incorporated into an entity's financial statements through the general ledger. The key types of payroll journal entries are noted below.

Primary Payroll Journal Entry

The primary journal entry for payroll is the summary-level entry that is compiled from the payroll register, and which is recorded in either the payroll journal or the general ledger. This entry usually includes debits for the direct labor expense, salaries, and the company's portion of payroll taxes.

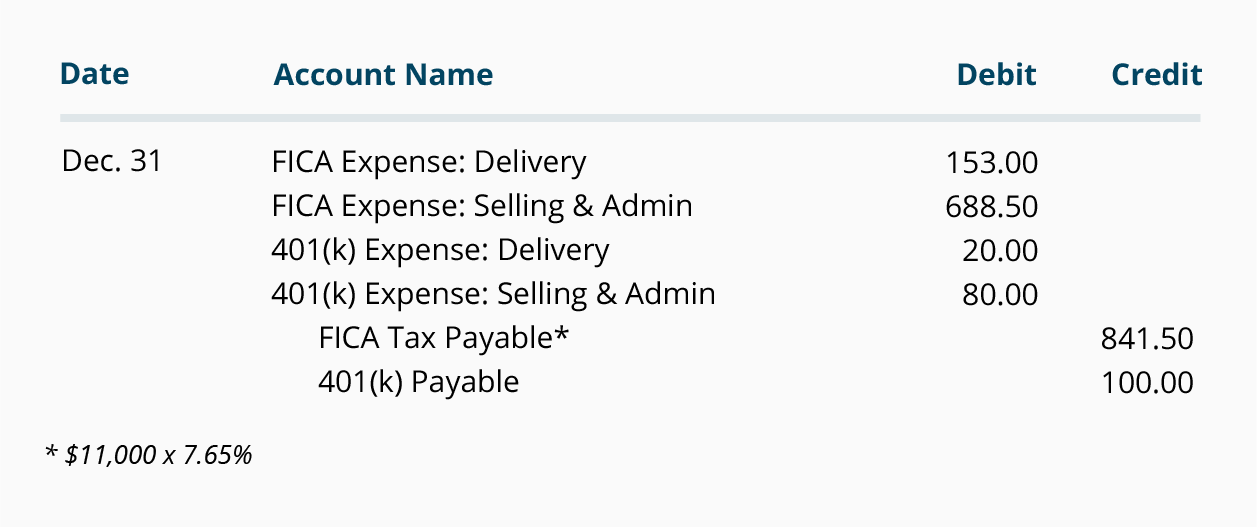

Accrued Payroll Journal Entry

It is quite common to have some amount of unpaid wages at the end of an accounting period, so you should accrue this expense (if it is material).

Manual Paycheck Entry

It is quite common to create a manual check, either because an employee was short-paid in the preceding payroll, or because the company is laying off or firing an employee, and so is obligated to pay that person before the next regularly scheduled payroll.

What happens to accounts credited in the entry?

All accounts credited in the entry are current liabilities and will be reported on the balance sheet if not paid prior to the preparation of financial statements. When these liabilities are paid, the employer debits each one and credits Cash.

Can a company credit FICA to the same account?

The company can credit both its own and the employees’ FICA taxes to the same liability account since both are payable at the same time to the same agency. When these liabilities are paid, the employer debits each of the liability accounts and credits Cash. Watch this video to review how to record payroll and taxes.

What is payroll journal entry?

A payroll journal entry is a record of your employee wages. It sounds deceptively simple but buckle up - it’s all downhill from here! There are a few type of payroll journal entries to consider: Also known as an initial recording, this first entry is very important. It covers the gross wages, withholdings and net pay.

Is payroll accounting complicated?

Payroll accounting can be pretty complicated. We break down what payroll entries are and how to make one to process your payroll. Whether you are paying one employee or dozens of employees, you need to make a payroll journal entry. As a small business owner, payroll accounting can be a headache. Hopefully we can simplify things today!

Is gross wage expense a debit or credit?

As you can see, the gross wage expense is at the top as a debit. Then the payroll deductions are credited as withholding amounts. These are withholding until they are actually paid. But you must account for them now so that it appears correctly in your payroll records.

Does payroll software automatically calculate taxes?

If you use excellent payroll software, you can simplify the process a lot. The system will automatically calculate the tax liabilities and gross pay for you. It will generate payroll journal entries on your behalf that you can present at tax time.

What is offset journal entry for accrued payroll?

What Is the Offset Journal Entry for Accrued Payroll?. Payroll accruals are a common practice when you have payroll cycles that cross different accounting periods. You need to recognize the payroll expenses incurred during the end of the accounting period.

How to enter payroll accrual?

Step 1. Determine the total outstanding payroll amount for the period. Step 2. Create a journal entry that credits the payroll accrual account for the outstanding amount. For example, if you have $12,000 outstanding for payroll in the period, credit the payroll accrual account $12,000. Step 3.

Why is it important to recognize payroll expenses?

Equally important is reversing that accrual when you issue the payroll deposits. It is important to understand the affected accounts, so that you can offset the journal entry appropriately and keep your reporting accurate. Payroll Accrual Entry.

How to reverse a payroll expense?

Step 1. Create a reversal entry when the payroll amount is paid. For the example above, debit the payroll accrual account for $12,000. Step 2. Credit the payroll expense account that was debited during the accrual process. In this example, credit the expense account for $12,000. Step 3.

What is accrued payroll?

Accrued payroll is a debt owed to employees. All accrued expenses are liabilities on your balance sheet until they’re paid. Only businesses that follow the accrual method of accounting need to accrue payroll on their books.

What is payroll accrual?

A payroll accrual starts with recording the total amount an employee earned during the period. Don’t forget to include taxable fringe benefits, such as commuter benefits, in the gross wages accrual. 2. Bonuses. Similarly, cash bonuses earned in one period and paid in the next warrant a payroll accrual.

What is PTO in payroll?

Don’t forget about taxes and paid time off (PTO) either. 1. Salary and hourly wages. Gross wages are an employee’s total compensation before payroll deductions, such as taxes and retirement contributions. A payroll accrual starts with recording the total amount an employee earned during the period.

What is a wages payable account?

The Wages Payable account is your employee’s net pay, or the amount written on her payroll check. 2. Record employer payroll taxes and contributions. Record employer-paid payroll taxes, such as the employer’s portion of FICA, FUTA, and SUTA.

How much is Susie's net pay?

First is the employee-paid taxes, which come out of your employee’s paycheck. Susie’s net pay, or paycheck amount, is $1,093.40 ($1,600 gross wages - $506.60 payroll deductions).

When do you accrue bonuses for 2020?

Since employees earned bonuses in 2020, you accrue a payroll expense for the bonus amount before the ball drops at midnight on Jan. 1. The bonuses count as a wage expense on your 2020 income statement. Accrued payroll is a debt owed to employees.

When will Susie receive her bonus?

If Susie receives a $1,000 bonus in 2021 for reaching her sales targets in 2020, I’d accrue $1,000 in bonus compensation by Dec. 31, 2020. Bonuses may be taxed the same as regular wages when paid with a regularly scheduled payroll run.

What is payroll journal entry?

Payroll journal entries are what an accountant (or in many cases the small business owner) uses to record business activity. Each entry affects at least two accounts that are typically on different sides of the accounting equation:

What is direct labor journal entry?

Here’s how the wages journal entry looks: Some companies expense part of the wages under cost of goods sold with an account called direct labor. For example, a construction company would expense all wages related to open jobs as "direct labor" and all wages related to overhead as "salaries and wages.".

What is the final step in EFTPS?

The final step is making all payments with the IRS EFTPS and other third parties, such as insurance companies, 401 (k) vendors and state agencies. This step will eliminate all current payroll liabilities other than the accrued vacation and sick time.

What are the steps of recording payroll?

Recording the payroll process with journal entries involves three steps: accruing payroll liabilities, transferring cash, and making payments. 1. Accrue short-term wage liabilities. Accounting rules stipulate that expenses and liabilities should be accrued when they are incurred.

What is debit and credit in journal entry?

Each journal entry has debits and credits that must add up to the same number. Accounts on the left side of the equation increase when debited and decrease when credited, and vice versa for accounts on the right side. The most basic payroll entry involves crediting cash and debiting wage expenses.

What is the final step in making direct deposits?

The final step is to make the payments . As direct deposits are sent to employees and the IRS pulls the EFTPS (Electronic Federal Tax Payment System) payment, journal entries are made to show cash paying down the liabilities.

When is payroll processed?

Payroll is processed sometime before the payments are sent at a scheduled time every other week. As part of the payroll process, companies have to make journal entries to recognize the expense for wages and labor burden (benefits and taxes) and balance those entries with liabilities for the same amount until employees are paid. 2.