What is the mortgage disclosure Improvement Act (MDIA)?

Back in 2009, the Mortgage Disclosure Improvement Act (MDIA) brought us the following changes to slow down the loan process and to make sure a borrower has the latest and greatest information in hand before loan closing: The “seven business-day delay” (from the time of initial disclosures) on consumer closed-end dwelling-secured mortgages; and,

What is the home mortgage disclosure act?

The Home Mortgage Disclosure Act (HMDA) is a federal act approved in 1975 that requires mortgage lenders to keep records of certain key pieces of information regarding their lending practices which they must submit to regulatory authorities.

What is the timing of disclosures?

Timing ofDisclosure:the law has always required disclosures within 3 days of the application. The new added regulation is that the client cannot close within 7 days of the application. This gives the client time to review the loan terms offered to them

What if my Apr changes after the last disclosure?

APR (Annual Percentage Rate)Change: If the APR changes by more than .125% since the last disclosure, the borrower must be re-disclosed and cannot close for 3 days from last disclosure for regular transactions (fixed mortgages).

See more

What is the 3 7 3 rule in mortgage terms?

Timing Requirements – The “3/7/3 Rule” The initial Truth in Lending Statement must be delivered to the consumer within 3 business days of the receipt of the loan application by the lender. The TILA statement is presumed to be delivered to the consumer 3 business days after it is mailed.

What are the two types of mortgage disclosures?

But these two legally binding and required documents bookend the loan process: The Loan Estimate comes after you submit an application with a lender, and the Closing Disclosure form arrives when you're nearing the get-a-mortgage finish line.

What are the 6 pieces of RESPA?

For transactions subject to the TRID Rule, an “application” consists of the submission of the following six pieces of information:The consumer's name;The consumer's income;The consumer's social security number to obtain a credit report;The property address;An estimate of the value of the property; and.More items...

Which disclosures must be given within 3 business days of receiving a mortgage application?

The rule requires creditors to deliver or place in the mail the Loan Estimate no later than three business days after the consumer submits a loan application. second form, the Closing Disclosure, replaced the HUD-1 Settlement Statement and the final Truth in Lending disclosure.

What are the three primary ask that impact mortgage loan disclosure?

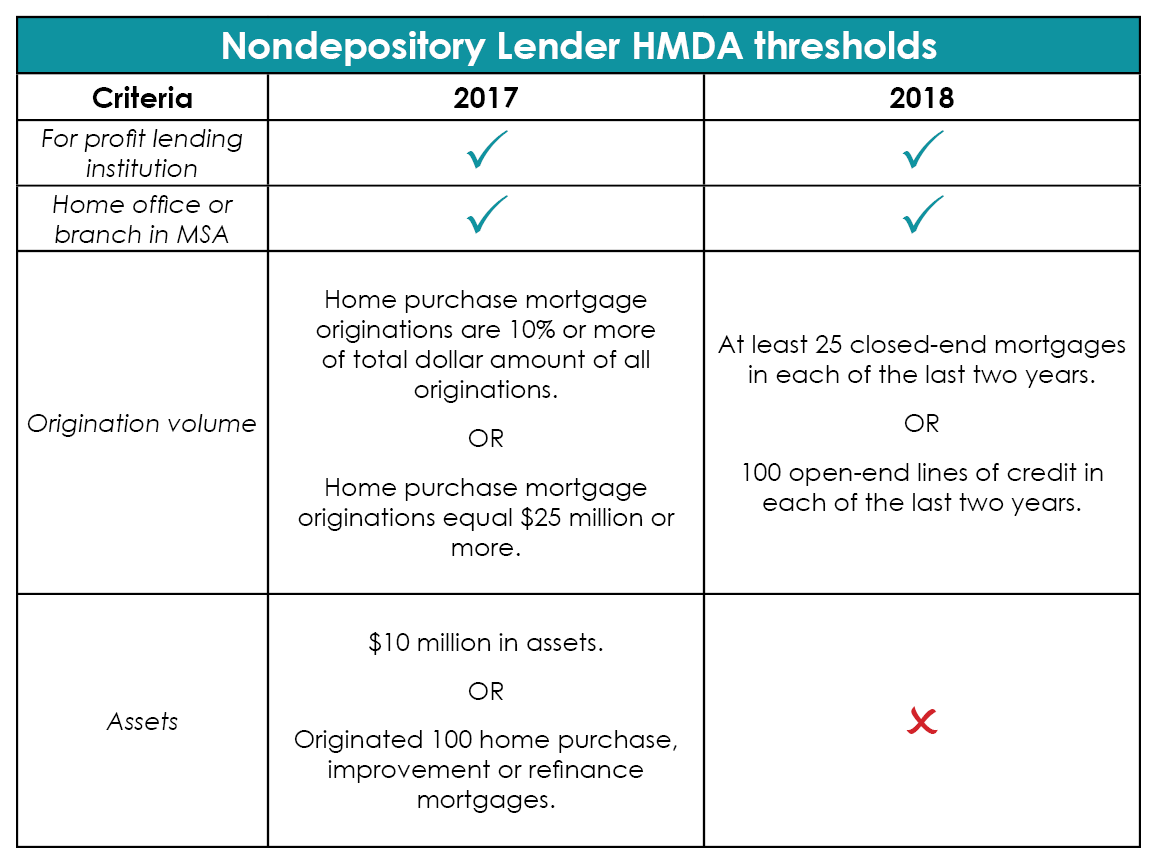

2 The data-related requirements in HMDA and Regulation C serve three primary purposes: (1) to help determine whether financial institutions are serving their communities' housing needs; (2) to assist public officials in distributing public investment to attract private investment; and (3) to assist in identify ing ...

What is the most commonly used disclosure in real estate?

Most Common Disclosures in Real EstateNatural Hazards Disclosure. First on the list is the natural hazards disclosure. ... Market Conditions Advisory (MCA) Market Conditions Advisory, also known as MCA, covers items more financial in nature. ... State Transfer Disclosure. ... Local Transfer Disclosure. ... Megan's Law Disclosures.

What are the most frequent RESPA violations?

6 Most Common RESPA ViolationsKickbacks & Referral Fees. Violation: ... Requiring Excessively Large Escrow Accounts Balances. Violation: ... Responding to Loan Servicing Complaints. Violation: ... Inflating Costs. Violation: ... Not Disclosing Estimated Settlement Costs. ... Demanding Title Insurance.

What does RESPA not prohibit?

RESPA Section 8 does not prohibit a lender or other settlement service provider from giving a consumer a gift or an incentive (e.g., a discount, refund of fees, chance to win a prize, etc.) for doing business with that entity.

What transactions are not covered by RESPA?

The following are kinds of transactions that are not covered: an all cash sale, a sale where the individual home seller takes back the mortgage, a rental property transaction or other business purpose transaction. 3. Is a "time share" a covered transaction under RESPA?

How often must the servicer of a mortgage loan deliver a written disclosure?

For all residential mortgage transactions, including high-risk mortgages for which PMI is required, the servicer must provide to the borrower an annual written statement that sets forth the rights of the borrower to cancel and terminate PMI and the address and telephone number that the borrower may use to contact the ...

Why is there a 3 day waiting period after closing disclosure?

Three Business-Day Waiting Period The CFPB final rule requires the lender to give the borrower three business days to thoroughly review the Closing Disclosure to enable them to compare the charges to the loan estimate and ensure the cost and loan program they are obtaining are as expected.

Which two items will appear on a closing disclosure?

A Closing Disclosure is a five-page form that provides final details about the mortgage loan you have selected. It includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

What are the 2 main types of mortgages and how do they differ?

Fixed Rate Loan vs Adjustable Rate Loan Mortgages are available with two different types of interest rates: fixed and adjustable. On a fixed-rate loan, the interest rate stays the same for the entire life in the loan. That means you lock in the interest rate of today's market for the next 15-30 years.

What are the two main documents in a mortgage?

Again, the loan transaction consists of two main documents: the mortgage (or deed of trust) and a promissory note. The mortgage or deed of trust is the document that pledges the property as security for the debt and permits a lender to foreclosure if you fail to make the monthly payments.

What are the two forms that make up the Trid rule?

TRID is actually a combination and condensed version of two such regulations: the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA).

What are examples of disclosures?

Disclosure is defined as the act of revealing or something that is revealed. An example of disclosure is the announcement of a family secret. An example of a disclosure is the family secret which is told.

How long does it take for a lender to use a closing date?

Guidelines require that the lender use at least 15 days when no closing date is picked. However, if you’re scheduled to close at the end of the month and the contract is extended to the beginning of the following month, ask your lender to re-disclose with the updated, corrected amount.

How long does it take to close a loan application?

Timing of Disclosure: the law has always required disclosures within 3 days of the application. The new added regulation is that the client cannot close within 7 days of the application. This gives the client time to review the loan terms offered to them.

What is the HMDA?

The Home Mortgage Disclosure Act (HMDA) requires many financial institutions to maintain, report, and publicly disclose loan-level information about mortgages. These data help show whether lenders are serving the housing needs of their communities; they give public officials information that helps them make decisions and policies; and they shed light on lending patterns that could be discriminatory. The public data are modified to protect applicant and borrower privacy.

What is HMDA data?

Mortgage data (HMDA) HMDA data are the most comprehensive source of publicly available information on the U.S. mortgage market.

What is mortgage disclosure?

The Mortgage Disclosure Improvement Act is a newer law that was created in part due to the mortgage crisis that occurred in 2008. This law was passed by the Federal Reserve Board in July 2008 and became effective in July 2009. Its main purpose is to make certain early disclosure requirements mandatory on non-purchase transactions that were previously only required on purchase transactions. It also requires waiting periods between the time when disclosures are given and closing of the mortgage transaction.

Can you collect credit report fees prior to early disclosure?

However, today Mortgage Disclosure Improvement Act says that no fee other than the credit report fee can be collected prior to the borrower receiving the early disclosures. Also, only the bona fide fee for the credit report can be charged to the borrower, no profit can be made on this third party fee.

When did the Mortgage Disclosure Improvement Act come into effect?

Back in 2009, the Mortgage Disclosure Improvement Act (MDIA) brought us the following changes to slow down the loan process and to make sure a borrower has the latest and greatest information in hand before loan closing:

How many days to re-disclosure APR?

Required re-disclosure of an inaccurate APR to be received at least three business days prior to closing.

How long do you have to re-disclose an APR?

If you do, you need to do so within three business days. If the APR becomes inaccurate after you’ve delivered the Closing Disclosure, you need to re-disclose it and restart your three business-day waiting period.

Is MDIA a TRID rule?

MDIA Created into TRID Rule. Actually, both MDIA requirements are written into the existing TRID Rule . In short, the seven-day closing delay is tied to the Loan Estimate and the three-day APR re-disclosure delay is tied solely to the Closing Disclosure.

Do you have to re-disclose your loan estimate?

So, there’s no requirement to re-disclose your Loan Estimate just because the APR changes.