What is the penalty for breaking a mortgage with Scotiabank? Three months Click to see full answer. Also, is there a penalty for breaking a mortgage? As we mentioned earlier, the penalty for breaking your existing mortgage is equal to three months worth of interest, or $1,881. In addition, you would pay about $1,000 in administrative costs.

Full Answer

Does Scotiabank charge prepayment penalty fees?

What is the penalty for breaking a mortgage with Scotiabank? Three months Click to see full answer. Also, is there a penalty for breaking a mortgage? As we mentioned earlier, the penalty for breaking your existing mortgage is equal to three months worth of interest, or $1,881. In addition, you would pay about $1,000 in administrative costs.

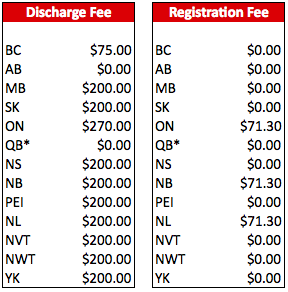

How much does Scotiabank charge to discharge a mortgage?

Dec 20, 2020 · the 2 year posted on scotia's website is 3.19%. Your original discount was 1.65% (4.64- 1.64 = 2.99%) So the 2 year posted, minus your discount: 3.19-1.65 = 1.54% 2.99 - 1.54% = 1.45%.. so your penalty is basically 18 months of interest at 1.45% On a $500,000 mortgage, it's like 0.0145 x $500,0000 / 12 x 18 = $10,875.

What is the penalty for breaking a mortgage contract?

May 16, 2021 · For example, the current 5 year posted rate is 4.79% according to Scotia's website. However, they are advertising a 5 year 1.99% closed mortgage. If you can manage to get 1.89%, the documents might show a 0.10% discount. The cost of borrrowing documents are separate and should show the details like posted rate...

What are the drivers of the mortgage penalty?

Your estimated mortgage penalty is $- . 3 months' interest penalty 0% x $- outstanding mortgage balance x 3/12 = 0.08 three month's interest penalty 0.00 mortgage break penalty + 0.00 lender discharge fees = 0.00 total fee to break mortgage Interest rate differential (IRD) penalty ( 0% - 0% ) / 12 convert to monthly interest rate = 0.00 ird factor

How much does Scotiabank charge to discharge a mortgage?

$270involved with discharging a mortgage from title. So this fee is not simply a lender cash grab. Although it's “interesting” that some lenders can be $100 apart for this service....Discharge Fees – The Basics.LenderDischarge FeeScotiabank$270TD Canada Trust$2005 more rows•Mar 27, 2008

What is the penalty to get out of a fixed mortgage?

As we mentioned earlier, the penalty for breaking your existing mortgage is equal to three months worth of interest, or $1,881. In addition, you would pay about $1,000 in administrative costs.Dec 17, 2021

How much does it cost to break a fixed mortgage Canada?

To break your mortgage contract with your current lender you'll need to pay a prepayment penalty of $6,000. You may also choose a blend-and-extend option with your current lender. This would give you a 4.6% interest rate.Jun 28, 2021

How are Scotiabank prepayment penalties calculated?

& Mortgage Prepayment Charges The rate of interest fluctuates when Scotiabank Prime Rate changes. If paying out the mortgage before the end of the term, typically a 3 months' interest prepayment charge calculated using the current interest rate on the mortgage, or cap rate if there is one, will apply.

How can I get out of my mortgage penalty in Canada?

Still, if you're facing a big penalty, you may be able to reduce it by taking advantage of your prepayment privileges, which allow you to pay a portion of the mortgage early cost-free. This will help you lower the balance used to calculate your penalty, McLister notes.Oct 10, 2020

How is a mortgage penalty calculated?

The two most common mortgage penalty calculations are known as Interest Rate Differential (IRD) and 3 Months Interest. 3 months Interest – This calculation is most commonly used for variable rate mortgage penalties. The following formula is used: [(mortgage rate/months in a year) x mortgage balance) x 3 = penalty.Apr 29, 2019

Is it worth breaking a fixed-rate mortgage?

As a general rule, customers won't financially benefit from breaking fixed rates and refinancing when interest rates are falling. The prepayment fee will offset any reduction in interest paid.Apr 12, 2009

Does it cost money to break a mortgage?

The cost to break your mortgage contract If you have an open mortgage, then there's no cost to break your mortgage. That said, most people have a closed mortgage, so you will have to pay a fee. The formula used is based on whether you have a fixed-rate or variable-rate mortgage.Aug 3, 2021

Can I pay my mortgage off early?

In most cases, you can pay your mortgage off early without penalty — but there are a few things to keep in mind before you do. First, reach out to your loan servicer to find out if your mortgage has a prepayment penalty. If it does, you'll have to pay an additional fee if you pay your loan off ahead of schedule.Dec 21, 2021

What is a mortgage penalty?

A prepayment penalty is a fee that your mortgage lender may charge if you: pay more than the allowed additional amount toward your mortgage. break your mortgage contract. transfer your mortgage to another lender before the end of your term.Jun 28, 2021

What does breaking a mortgage mean?

When you break your mortgage contract early it means that you want to stop making your agreed upon regular payments before your term is up.Dec 8, 2021

How is mortgage prepayment calculated?

Prepayment charges are calculated differently depending on the type of mortgage you have. For Fixed rate mortgages, the prepayment charge will be the greater of 3 months interest or interest for the remainder of the term on the amount prepaid calculated using the interest rate differential.

How to determine mortgage break penalty?

Most lenders determine the mortgage break penalty for a variable rate mortgage by calculating three months of interest. The interest rate that they use can depend from lender to lender, but is usually either your current mortgage interest rate or the lender's prime rate. Based On Your Mortgage Rate.

What is a closed term mortgage?

That being said, a closed-term mortgage is one that you take out for a specified amount of time. In Canada, the standard term is about 5 years. As mentioned, the main difference with a closed-term mortgage is you don't have the freedom to payoff your principal when you want.

How to get a mortgage discount?

Method 2: Interest Rate Differential (IRD) 1 First the lender will get the non-discounted rate that was posted the day you signed your mortgage agreement 2 years ago. So you may be paying 3.25% but the actual rate was 4.0% on that day. Which means you got a discount of .75%. 2 Next, the lender will see that you have 3 years left on your agreement and will find a similar product that they have, right now, to cover the remainder of your 5-year term. That being, a 3-year fixed rate mortgage let's say at a rate of 2.75%. 3 Finally, the lender takes the difference of rates 4.0% and 2.75% (.04 - .0275 = .0125), divides that total by 12 to get the monthly intereset rate (.0125 divide 12 = .00104), multiplies the monthly interest rate value by the 36 months (3 years) you have remaining on your mortgage (.00104 x 36 months). Then, multiplies this 36 month amount by your $400,000 principal to get your prepayment penalty (.00104 x 36 months) x $400,000. Thus, you will pay around $15,000 as a prepayment penalty.

What is IRD in mortgage?

The IRD is the difference of interest that you owe to your lender for the remainder of your mortgage contract, calculated at two different rates. The first amount of interest owing is calculated at the non-discounted rate you originally signed your agreement.

Can you break a mortgage early?

For example, if you are 3 years into your 5-year fixed rate mortgage, and you find out that a lender is offering a significantly lower interest rate, then it is possible to break your mortgage early to sign a new mortgage with the discounted lender.

When you renew your mortgage do you have to qualify?

The one good reason to stick with your current lender is that it doesn't need to re-qualify you (for example, determine your debt service ratios). Typically, as long as you've made all your mortgage payments throughout your term, there's no reason your current lender would deny your mortgage renewal application.

What happens if I don't renew my mortgage on time?

However, if you frequently miss your mortgage payments, lost your job or have a low credit score, the lender may choose to decline the renewal. They must notify you of their decision at least 21 days prior to the expiry of your term.

Do banks check credit for mortgage renewal?

At mortgage renewal time, credit checks are usually considered before a renewal is processed – there are some exceptions. Remember, your credit score is always available to your creditors and they will check at any time they wish. They will likely not even check the credit report.

How long does it take to renew your mortgage?

You may qualify to renew your mortgage as early as 150 days before maturity. If you do, lenders often waive any prepayment charges or other fees, depending on the mortgage type and other incentives. Thirty days before renewal, time gets tight and you should take action. Leave at least 3 weeks to complete the paperwork.

How early can I renew my mortgage RBC?

120-Day Early Renewal Option : Take advantage of our 120-day early renewal option, which allows you to renew early without any penalties1. This could save you in interest costs if rates rise before your regular renewal date.

When should I start looking to renew my mortgage?

By finding out which lenders are offering what, in terms of mortgage rates, prepayment options and other terms and conditions, you'll be better armed to negotiate when you are ready to renew.

What documents do I need for mortgage renewal?

Income verification – have ready. 2 recent pay stubs. 2 recent year's tax assessments.