How do you calculate VaR?

What are the mechanics of calculating VaR using Historical Simulation?

- Using historical data, determine your portfolio’s value for a number of days (typically around 500)

- Calculate the % change between each day

- Using your current portfolio valuation, calculate the monetary impact of the % change.

- Sort your results from the highest loss to most profit

How to compute VaR?

- Set a significance percentile , a market observation period, and holding period n. 1

- Generate a set of future market conditions (“scenarios”) from today to period n.

- Compute a P/L on the position for each scenario

What is VaR calculation?

• Variance is calculated by subtracting the average return from each individual return, squaring that figure, summing the squares across all observations, and dividing the sum by the number of observations. • The square root of the variance, called the standard deviation or the volatility, can be used to estimate risk.

What is a Var confidence level?

Value-at-risk is a statistical measure of the riskiness of financial entities or portfolios of assets. It is defined as the maximum dollar amount expected to be lost over a given time horizon, at a pre-defined confidence level. For example, if the 95% one-month VAR is $1 million, there is 95% confidence that over the next month the portfolio will not lose more than $1 million.

What is the VaR technique?

More specifically, VaR is a statistical technique used to measure the amount of potential loss that could happen in an investment portfolio over a specified period of time. Value at Risk gives the probability of losing more than a given amount in a given portfolio.

What is VaR and how is it calculated?

Value at Risk (VAR) is a statistic that is used in risk management to predict the greatest possible losses over a specific time frame. VAR is determined by three variables: a specific time period, a confidence level, and the size of the possible loss.

What are the methodologies used for VaR calculation?

There are three methods to calculate Value at Risk which are:Historical Method. The Historical Method is the simplest method among the three to calculate Value at Risk. ... Parametric method. The most common way of calculating VaR is the parametric method, also known as variance covariance method. ... Monte Carlo Method:

What do you mean by VaR?

Value at risk (VaR) is a statistic that quantifies the extent of possible financial losses within a firm, portfolio, or position over a specific time frame.

What is VaR example?

Value at Risk (VAR) can also be stated as a percentage of the portfolio i.e. a specific percentage of the portfolio is the VAR of the portfolio. For example, if its 5% VAR of 2% over the next 1 day and the portfolio value is $10,000, then it is equivalent to 5% VAR of $200 (2% of $10,000) over the next 1 day.

What is a 95% VaR?

It is defined as the maximum dollar amount expected to be lost over a given time horizon, at a pre-defined confidence level. For example, if the 95% one-month VAR is $1 million, there is 95% confidence that over the next month the portfolio will not lose more than $1 million.

Which VaR method is most accurate?

From a user's perspective, the important point to remember is that if you have significant nonlinear exposures in your portfolio, a simulation approach will generally be more accurate for estimating VaR than a parametric approximation--however, at the cost of greater complexity and computational requirements.

What is the value at risk methodology?

Value at risk (VaR) is a popular method for risk measurement. VaR calculates the probability of an investment generating a loss, during a given time period and against a given level of confidence. It gives investors an indication of the level of risk they take with a certain investment.

What is VaR in Excel?

The Excel VAR function estimates the variance of a sample of data. If data represents the entire population, use the VARP function or the newer VAR. P function. VAR ignores text values and logicals in references. Get variation of a sample.

What is the role of the VaR?

VAR – Video Assistant Referee; main video official whose main role is to check all reviewable incidents and recommend an OFR where a possible clear and obvious error has occurred. The VAR is a current or former qualified referee.

What is a VAR?

Value at Risk (VAR) calculates the maximum loss expected (or worst case scenario) on an investment, over a given time period and given a specified degree of confidence. We looked at three methods commonly used to calculate VAR. But keep in mind that two of our methods calculated a daily VAR and the third method calculated monthly VAR. In Part 2 of this series, we show you how to compare these different time horizons .

What are the components of a VAR statistic?

Now let's get specific. A VAR statistic has three components: a time period, a confidence level and a loss amount (or loss percentage). Keep these three parts in mind as we give some examples of variations of the question that VAR answers: 1 What is the most I can—with a 95% or 99% level of confidence —expect to lose in dollars over the next month? 2 What is the maximum percentage I can—with 95% or 99% confidence—expect to lose over the next year?

Why are stocks volatile?

The main problem with volatility, however, is that it does not care about the direction of an investment's movement: stock can be volatile because it suddenly jumps higher. Of course, investors aren't distressed by gains.

How to calculate variance covariance?

In some cases, a method equivalent to the variance covariance approach is used to calculate VAR. This method does not generate the variance covariance matrix and uses the following approach: 1 Separate the portfolio in a long side and a short side. 2 Calculate the return series for the long side and the short side. 3 Use the return series to calculate the correlation and variances for the long and short sides 4 Use the results in (3) to calculate the VaR.

What is the assumption of hypothetical data set?

The assumption is that the selected distribution captures or reasonably approximates price behavior of the modeled securities.

When calculating value at risk of a portfolio, do you need to measure or estimate?

When you’re calculating Value At Risk of a portfolio, you need to measure or estimate not only the return and volatility of individual assets, but also the correlations between them. With growing number and diversity of positions in the portfolio, the difficulty (and cost) of this task grows exponentially.

What does 99% mean in value at risk?

VAR does not measure worst case loss. 99% percent VAR really means that in 1% of cases (that would be 2-3 trading days in a year with daily VAR) the loss is expected to be greater than the VAR amount. Value At Risk does not say anything about the size of losses within this 1% of trading days and by no means does it say anything about ...

Is value at risk misleading?

Value At Risk can be misleading: false sense of security. Looking at risk exposure in terms of Value At Risk can be very misleading. Many people think of VAR as “the most I can lose”, especially when it is calculated with the confidence parameter set to 99%.

MONTE CARLO SIMULATION

Many commercial providers simulate future market conditions using Monte Carlo simulation. To do this, they must first estimate the distributions of risk factors, including correlations between risk factors. Using correlations that are derived from historical data makes the general assumption that correlations are constant within the period.

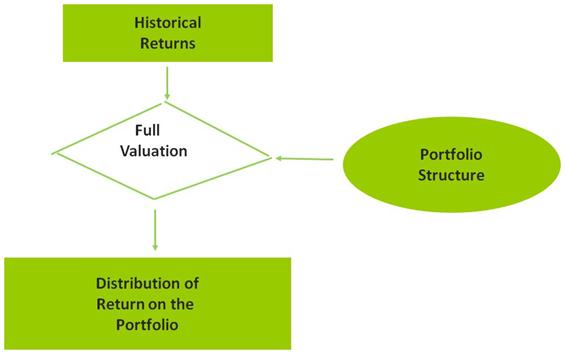

HISTORICAL SIMULATION

RiskSpan projects future market conditions by using actual (observed) -day changes in market conditions over the look-back period. For example, if we are computing 10-day VaR for regulatory capital usage under the Market Risk Rule, RiskSpan takes actual 10-day changes in market variables.

RATIONALIZING WEAKNESS IN THE APPROXIMATION

With the weaknesses in the Taylor approximation cited above, why do some providers still use delta-gamma VaR? Most practitioners will cite that the Taylor approximation is much faster than full revaluation for complex, non-linear instruments. While this seems true at first glance, you still need to:

ENDNOTES

1 The holding period n is typically one day, ten days, or 21 days (a business-month) although in theory it can be any length period.

The Idea Behind var

Methods of Calculating var

Historical Method

- The historical method simply re-organizes actual historical returns, putting them in order from worst to best. It then assumes that history will repeat itself, from a risk perspective. As a historical example, let's look at the Nasdaq 100 ETF, which trades under the symbol QQQ (sometimes called the "cubes"), and which started trading in March of 1999.3 If we calculate each daily return, we p…

The Variance-Covariance Method

- This method assumes that stock returns are normally distributed. In other words, it requires that we estimate only two factors—an expected (or average) return and a standard deviation—which allow us to plot a normal distribution curve. Here we plot the normal curve against the same actual returndata: The idea behind the variance-covariance is similar to the ideas behind the hist…

Monte Carlo Simulation

- The third method involves developing a model for future stock price returns and running multiple hypothetical trials through the model. A Monte Carlo simulationrefers to any method that randomly generates trials, but by itself does not tell us anything about the underlying methodology. For most users, a Monte Carlo simulation amounts to a "black box" generator of ra…

The Bottom Line

- Value at Risk (VAR) calculates the maximum loss expected (or worst case scenario) on an investment, over a given time period and given a specified degree of confidence. We looked at three methods commonly used to calculate VAR. But keep in mind that two of our methods calculated a daily VAR and the third method calculated monthly VAR. In Part 2 of ...