The process of accounting

- 1. Identifying Identifying business transactions ...

- 2. Measuring Measuring refers to the analysis, recording and classifying of business transactions. ...

- 3. Communicating Communicating relevant information through accounting reports, such as the income statement and the balance sheet, for decision-making purposes. ...

- 4. Decision making ...

What are some basic accounting procedures?

Basic accounting procedures include collecting financial documents, posting transactions and reconciling accounts. Other procedures include auditing accounts payable and accounts receivable, and conducting internal and external reporting, according to David Ingram for the Houston Chronicle.

What are the steps in the accounting process?

Steps in the Accounting Process - The Accounting Process is a sequence of organization activities that is used for gaining quantitative information about the finances. This complex process consists of a set of sequential steps. 9 steps in the accounting process: Analysis of Business Transactions, Make Journal Entries, Post to Ledger Accounts, Prepare Trial Balance, Make Adjusting Entries ...

What are the 10 steps in the accounting cycle?

What are the 10 steps of accounting cycle? 10 Steps of Accounting Cycle are; Analyzing and Classify Data about an Economic Event. Journalizing the transaction. Posting from the Journals to General Ledger. Preparing the Unadjusted Trial Balance. Recording Adjusting Entries. Preparing the Adjusted Trial Balance. Preparing Financial Statements.

What does the accounting process begins with?

Thus, the accounting process includes the steps that are to be followed for recording, classifying, summarizing, etc. the financial transaction of the business where the process starts with identifying the transaction and ends mainly with the preparation of financial statements that are finally used and evaluated by the users of the business.

What are the 4 accounting processes?

The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance.

What are the 3 processes of accounting?

Three fundamental steps in accounting are:Identifying and analyzing the business transactions.Recording of the business transactions.Classifying and summarising their effect and communicating the same to the interested users of business information.

What are the 5 steps in the accounting process?

Here are the steps in the accounting cycle:Step 1: Transactions.Step 2: Record journal entries.Step 3: Post journal entries to the general ledger (G/L)Step 4: Run unadjusted trial balance.Step 5: Make adjusting entries.Step 6: Prepare an adjusted trial balance.Step 7: Run financial statements.Step 8: Close the books.More items...•

What are the 7 steps in the accounting process?

The seven steps in the accounting cycle are as follows:Identifying and Analysing Business Transactions.Posting Transactions in Journals.Posting from Journal to Ledger.Recording adjusting entries.Preparing the adjusted trial balance.Preparing financial statements.Post-Closing Trial Balance.

What is accounting process or cycle?

The accounting cycle is the process of accepting, recording, sorting, and crediting payments made and received within a business during a particular accounting period.

Why Accounting is a process?

Accounting is a process that sets out to make sense of the everyday financial transactions that a business will encounter. This process deals with the constant stream of paperwork that usually accompanies every financial transaction, for example invoices received from suppliers for goods the business has bought.

How many steps are in the accounting cycle?

eightThe accounting cycle is eight basic steps that ensure a business fulfills its bookkeeping tasks accurately. Perform the process monthly, quarterly or annually based on how often your company needs financial reports.

What are the different types of accounting?

Here are the nine most common types of accounting:Financial accounting. ... Managerial accounting. ... Cost accounting. ... Auditing. ... Tax accounting. ... Accounting information systems. ... Forensic accounting. ... Public accounting.More items...

What is the last step of accounting process?

The final accounting cycle step is to close your books. Closing your books wraps up financial activities for the period.

What is the 6 step accounting process?

The steps of the accounting process are analyzing, recording, classifying, summarizing, reporting, and interpreting. Computers are often used in the recording, classifying, summarizing, and reporting.

What is the 6 accounting cycle?

Step 6: Prepare financial statements The last step in the accounting cycle is preparing financial statements—they'll tell you where your money is and how it got there. It's probably the biggest reason we go through all the trouble of the first five accounting cycle steps.

What are the 10 steps in the accounting cycle?

10 Steps of the Accounting CycleAnalyzing transactions.Entering journal entries of the transactions.Transferring journal entries to the general ledger.Crafting unadjusted trial balance.Adjusting entries in the trial balance.Preparing an adjusted trial balance.Processing financial statements.Closing temporary accounts.More items...

What are three golden rules accounting?

Take a look at the three main rules of accounting: Debit the receiver and credit the giver....Debit the receiver and credit the giver. ... Debit what comes in and credit what goes out. ... Debit expenses and losses, credit income and gains.

What are the three 3 steps in the accounting cycle that need to be done before a trial balance can be drafted?

Step 1: Analyze and record transactions. ... Step 2: Post transactions to the ledger. ... Step 3: Prepare an unadjusted trial balance. ... Step 4: Prepare adjusting entries at the end of the period. ... Step 5: Prepare an adjusted trial balance. ... Step 6: Prepare financial statements.

What is the most important step in accounting process?

There are eight steps in accounting cycle they are: Journal entries, Posting, trial balance, worksheet, adjusting journal entries, financial statements, and closing of the books. Preparing financial statement is the most important phase of accounting cycle.

What is the first step of accounting process?

The first step of accounting process is identifying the financial transactions.

1. What are the Interim and Annual Financial Statements?

The interim statement is a type of financial report which covers a period of less than one year. Annual statements are not audited. Interim stateme...

2. Define an Accounting Period.

An accounting period is a type of established range of time during which the accounting functions are performed, aggregated and analyzed including...

3. What is a Balance Sheet?

A Balance Sheet is the financial statement of a company that comprises assets, liabilities, equity capital, total debt, etc. at a point in time. Th...

4. What is an Income Statement?

The income statement focuses on four key terms—revenue, expenses, gains, and losses. This statement does not differentiate between cash and non-cas...

5. How can Vedantu help someone to understand accounting easily?

Vedantu provides easy-to-understand information about various important topics in accounting including Final Statements of a company, Income, and E...

What is accounting in economics?

Definition of Accounting: Accounting is a set of concepts and techniques that are used to identify, measure, record, classify, summarize and report financial information of an economic unit to the users of the accounting information.

How old is accounting?

There are proofs which suggest that accounting might be more than 7000 years old.

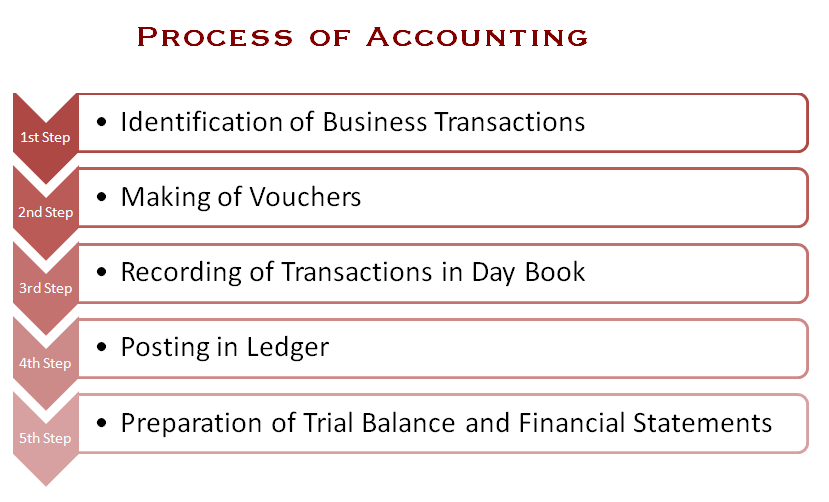

What is the process of accounting?

The process starts with identifying and analyzing business events and transactions. Not every transaction and event is entered into the accounting system. Only those which pertain to a business entity are included.

What is the last step in the accounting cycle?

In the accounting cycle, the last step is to prepare a post-closing trial balance. It is prepared to test the equality of debits and credits after the closing entries. It contains real accounts, and these balances are transferred to the next financial year as an opening balance.

What is a financial statement?

Financial statements are a set of statements like Income and expenditure account or profit and loss and trading account, fund flow statement, cash flow statement, balance sheet or statement of affairs account.

When are adjustments made in accounting?

Various adjustments are made in accounts at the end of the accounting period before the preparation of the final trial balance. It may be prepared after adjusting entries that are made before the preparation of financial statements.

What is debit and credit balance?

Debit and credit balance of all accounts affect through journal entries which are posted in ledger accounts. A ledger is known as ‘Books of Final Entry’, the collection of funds that shows the changes made to each account due to current balances and past transactions.

What are the Steps in the Accounting Process?

The accounting process is the series of steps followed by the business entity to record the business financial transactions that include steps for collecting, identifying, classifying, summarizing and recording of the business transactions in the books of accounts of the company so that the financial statements of the entity can be prepared and the profits and the financial position of the business can be known after regular intervals of time.

What is the first step in accounting?

Identifying the business transaction is the initial step in the process of accounting. The business entity has to identify financial and monetary transactions. Therefore, only those transactions that are monetary is recorded. Also, the transactions that belong to the business are to be recorded, and not the personal transactions ...

What is profitability in accounting?

After all the above steps are completed, the financial statements of the company are prepared to know the actual financial position, the profitability#N#Profitability Profitability refers to a company's ability to generate revenue and maximize profit above its expenditure and operational costs. It is measured using specific ratios such as gross profit margin, EBITDA, and net profit margin. It aids investors in analyzing the company's performance. read more#N#position, and the cash flow position of the business. The statements that are prepared for knowing the above positions are a statement of profit and loss for knowing the profitability position, the balance sheet for getting the financial position, and the cash flow statement#N#Cash Flow Statement Statement of Cash flow is a statement in financial accounting which reports the details about the cash generated and the cash outflow of the company during a particular accounting period under consideration from the different activities i.e., operating activities, investing activities and financing activities. read more#N#to know the changes in cash flows#N#Cash Flows Cash Flow is the amount of cash or cash equivalent generated & consumed by a Company over a given period. It proves to be a prerequisite for analyzing the business’s strength, profitability, & scope for betterment. read more#N#from the three activities of the business (operating, investing and financing activities).

What is temporary account?

The temporary accounts are the accounts whose balances ends in a single accounting year such as sales, purchases, expenses, etc. These balances are first transferred to the income statement and then to the permanent account, i.e., the profit/loss is transferred to retained earnings.

When is a trial balance to be prepared?

After all the adjusting entries are made, again, a trial balance is to be prepared before preparing the financial statements to check that all the credits are equal to the debits after the adjustment entries are made.

When is accrual basis used in accounting?

When the accrual basis of accounting is followed, some of the entries are to be made at the end of the accounting year, such as entries of expenses that may have been incurred but are not booked in the Journal and entries of some income that may be earned by the business but are not yet recorded in the books. For example, the interest amount on a fixed deposit is earned each year, but it is accumulated in the fixed deposit amount. This interest income is to be recorded in the books of accounts yearly because the interest is earned yearly, no matter the amount will be received together after the maturity of the fixed deposit.

When are revenues and expenses recorded in accounting?

In the accrual basis of accounting, the revenues and expenses are recorded in the books of the entity in the period when they are earned and incurred respectively, regardless of the actual cash receipt and payment. However, in the case of cash accounting, the transactions are recorded only when the actual cash is received/paid.

What are the Steps in the Accounting Process?

The accounting process is three separate types of transactions used to record business transactions in the accounting records. This information is then aggregated into financial statements. The transaction types are:

What are the steps required for individual transactions in the accounting process?

The steps required for individual transactions in the accounting process are: Identify the transaction. First, determine what kind of transaction it may be. Examples are buying goods from suppliers, selling products to customers, paying employees, and recording the receipt of cash from customers. Prepare document.

What is the first transaction type?

The transaction types are: The first transaction type is to ensure that reversing entries from the previous period have, in fact, been reversed. The second group is comprised of the steps needed to record individual business transactions in the accounting records. The third group is the period-end processing required to close ...

Where is a business transaction recorded?

Every business transaction is recorded in an account in the accounting database, such as a revenue, expense, asset, liability, or stockholders' equity account. Identify which accounts are to be used to record the transaction. Record the transaction. Enter the transaction in the accounting system.

What is the third group in accounting?

The third group is the period-end processing required to close the books and produce financial statements.

Why adjust trial balance?

It may be necessary to adjust the trial balance, either to correct errors or to create allowances of various kinds, or to accrue for revenues or expenses in the period .

Does accounting software create trial balances?

In reality, any accounting software package will automatically create all versions of the trial balance and the financial statements, so the actual steps in the accounting process may be considerably reduced. Instead, the steps used in a computerized environment are likely to be: Prepare financial statements.

What is the accounting cycle?

The accounting cycle is the holistic process of recording and processing all financial transactions of a company, from when the transaction occurs, to its representation on the financial statements. Three Financial Statements The three financial statements are the income statement, the balance sheet, and the statement of cash flows.

What are the most important steps in the accounting cycle?

The fundamental concepts above will enable you to construct an income statement, balance sheet, and cash flow statement, which are the most important steps in the accounting cycle. To learn more, check out CFI’s free Accounting Fundamentals Course.

What is an adjusting entry?

Adjusting Entries#N#Adjusting Entries This guide to adjusting entries covers deferred revenue, deferred expenses, accrued expenses, accrued revenues and other adjusting journal#N#: At the end of the company’s accounting period, adjusting entries must be posted to accounts for accruals and deferrals.

What is journal entries?

Journal Entries#N#Journal Entries Guide Journal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)#N#: With the transactions set in place, the next step is to record these entries in the company’s journal in chronological order. In debiting one or more accounts and crediting one or more accounts, the debits and credits must always balance.

What is revenue recognition?

Revenue Recognition Revenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. In theory, there is a. (when a company can record sales revenue), the matching principle.

What would happen if there were no financial transactions?

Transactions: Financial transactions start the process. If there were no financial transactions, there would be nothing to keep track of. Transactions may include a debt payoff, any purchases or acquisition of assets, sales revenue, or any expenses incurred.

What are the three financial statements?

Three Financial Statements The three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. : The balance sheet, income statement, and cash flow statement can be prepared using the correct balances.

What Is the Accounting Cycle?

The accounting cycle is a basic, eight-step process for completing a company’s bookkeeping tasks. It provides a clear guide for the recording, analysis, and final reporting of a business’s financial activities.

How is the accounting cycle used?

The accounting cycle is used comprehensively through one full reporting period. Thus, staying organized throughout the process’s time frame can be a key element that helps to maintain overall efficiency. Accounting cycle periods will vary by reporting needs. Most companies seek to analyze their performance on a monthly basis, though some may focus more heavily on quarterly or annual results.

What is the second step in the cycle?

The second step in the cycle is the creation of journal entries for each transaction. Point of sale technology can help to combine steps one and two, but companies must also track their expenses. The choice between accrual and cash accounting will dictate when transactions are officially recorded. Keep in mind, accrual accounting requires the matching of revenues with expenses so both must be booked at the time of sale.

What is a general ledger?

Once a transaction is recorded as a journal entry, it should post to an account in the general ledger. The general ledger provides a breakdown of all accounting activities by account. This allows a bookkeeper to monitor financial positions and statuses by account.

How many steps are there in an accounting cycle?

There are usually eight steps to follow in an accounting cycle. The closing of the accounting cycle provides business owners with comprehensive financial performance reporting that is used to analyze the business. The eight steps of the accounting cycle are as follows: identifying transactions, recording transactions in a journal, posting, ...

Why is it important to know the amount of time for each accounting cycle?

Overall, determining the amount of time for each accounting cycle is important because it sets specific dates for opening and closing. Once an accounting cycle closes, a new cycle begins, restarting the eight-step accounting process all over again.

When is adjusting entries needed for revenue and expense matching?

In addition to identifying any errors, adjusting entries may be needed for revenue and expense matching when using accrual accounting.