7 documents you need when applying for a home loan

- 1. Tax returns Mortgage lenders want to get the full story of your financial situation. ...

- 2. Pay stubs, W-2s or other proof of income Lenders may ask to see your pay stubs from the past month or so. ...

- 3. Bank statements and other assets ...

- 4. Credit history ...

- 5. Gift letters ...

- 6. Photo ID ...

- 7. Renting history ...

Full Answer

What documents are required for a mortgage?

Mortgage lenders request documentation to qualify you for a mortgage based on rules set by the CFPB and other government entities. You'll generally need to provide proof of your identity, income, assets, and debt payments. More complicated or unusual financial scenarios may require additional documentation.

What is the best way to get a mortgage?

In this guide

- Know what mortgage you want

- Get an idea of what you can get

- Talk to a mortgage broker

- Check deals that brokers miss

- Check mortgage paperwork

- Watch out for the hard sell

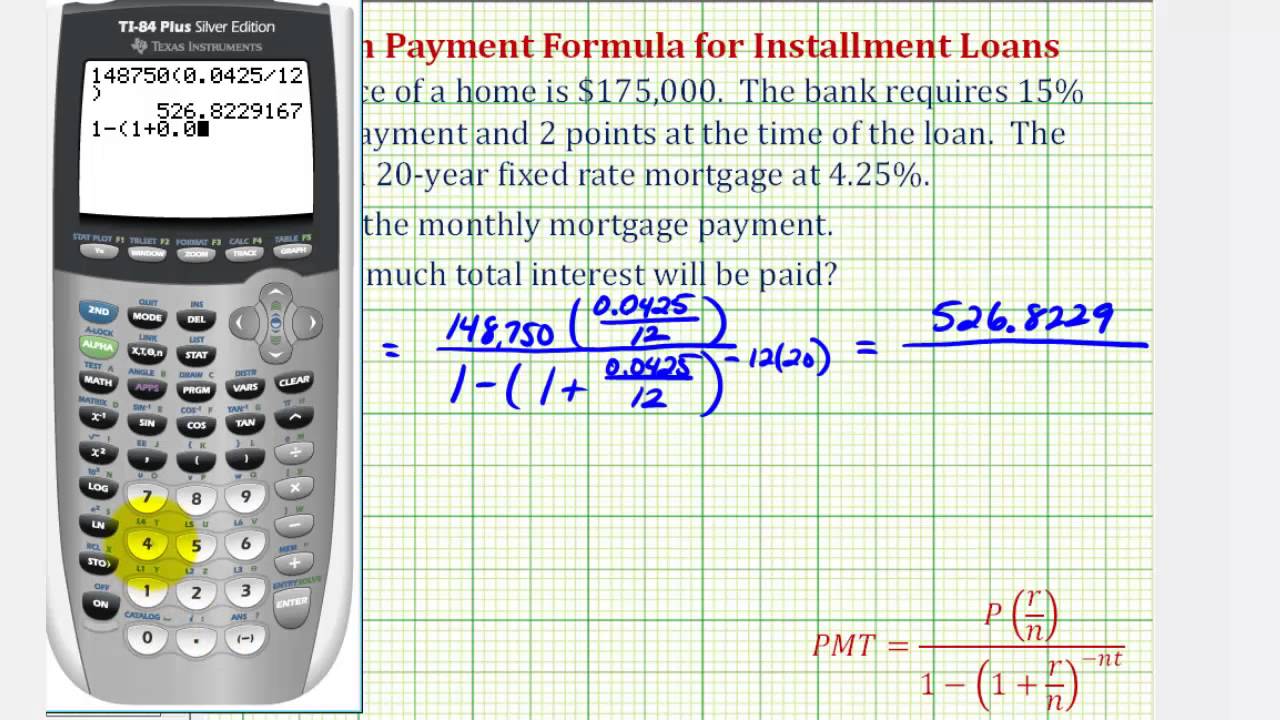

How to calculate what mortgage is best for You?

- Comparing the monthly payment for several different home loans

- Figuring how much you pay in interest monthly, and over the life of the loan

- Tallying how much you actually pay off over the life of the loan, versus the principal borrowed, to see how much you actually paid extra

What documents are required for a loan?

What documents are needed for a home loan?

- Personal identification. Any lender you go through will require you to verify your identity when making a loan application. ...

- Income details. You can prove your income in a number of different ways depending on your employment circumstances. ...

- Home loan situation

- Assets and liabilities. ...

What Is A Mortgage?

A simple definition of a mortgage is a type of loan you can use to buy or refinance a home. Mortgages are also referred to as “mortgage loans.” Mor...

Who Gets A Mortgage?

Most people who buy a home do so with a mortgage. A mortgage is a necessity if you can’t pay the full cost of a home out of pocket.

What’s The Difference Between A Loan And A Mortgage?

Mortgages are “secured” loans. With a secured loan, the borrower promises collateral to the lender in the event that they stop making payments. In...

How Does A Mortgage Loan Work?

When you get a mortgage, your lender gives you a set amount of money to buy the home. You agree to pay back your loan – with interest – over a peri...

What do lenders look for when applying for a mortgage?

Lenders must be careful to only choose qualified clients who are likely to repay their loans. To do this, lenders look at your full financial profile – including your credit score, income, assets and debt – to determine whether you’ll be able to make your loan payments.

Why do you need a mortgage?

A mortgage is a necessity if you can’t pay the full cost of a home out of pocket. There are some cases where it makes sense to have a mortgage on your home even though you have the money to pay it off. For example, investors sometimes mortgage properties to free up funds for other investments.

How Does A Mortgage Loan Work?

When you get a mortgage, your lender gives you a set amount of money to buy the home. You agree to pay back your loan – with interest – over a period of several years. You don’t fully own the home until the mortgage is paid off.

What is a mortgage loan?

A mortgage is a type of loan that’s used to finance property. A mortgage is a type of loan, but not all loans are mortgages. Mortgages are “secured” loans. With a secured loan, the borrower promises collateral to the lender in the event that they stop making payments. In the case of a mortgage, the collateral is the home.

What is a borrower on a mortgage?

The borrower is the individual seeking the loan to buy a home. You may be able to apply as the only borrower on a loan, or you may apply with a co-borrower. Adding more borrowers with income to your loan may allow you to qualify for a more expensive home.

How long does a fixed rate mortgage stay the same?

Fixed interest rates stay the same for the entire length of your mortgage. If you have a 30-year fixed-rate loan with a 4% interest rate, you’ll pay 4% interest until you pay off or refinance your loan. Fixed-rate loans offer a predictable payment each month, which makes budgeting easier.

How long does an adjustable rate mortgage last?

Most adjustable rate mortgages begin with a fixed interest rate period, which usually lasts 5, 7 or 10 years. During this time, your interest rate remains the same. After your fixed interest rate period ends, your interest rate adjusts up or down every 6 months to a year.

1. Check your credit report

You can view your credit score on our app or if you don’t have the NatWest app you can use various platforms such as Experian, Equifax or ClearScore.

2. Proof of ID

A passport or driving license are the more commonly used documents for proof of ID but we will accept other forms of ID if you don't have these. You'll also need to make sure these documents are in date.

3. Proof of address documents

These can include council tax bills, utility bills, bank statements and should be dated within the last three months.

4. Evidence of where your deposit is coming from

This is important as lenders will need to see Proof of Deposit to understand where your deposit is coming from.

5. Proof of income

Last 3 months payslips. If you have recently started a new job or changed salary, you’ll need to be able to provide proof of your salary.

6. Proof of expenses

As well as proof of income, expenses are also needed to ensure that the mortgage loan amount suits your lifestyle and requirements.

Looking to buy to let?

If you're looking for a property to let out, the mortgage process is very similar to the residential mortgage process but there are some differences regarding eligibility and criteria.

What do you need to show to get a mortgage?

Potential buyers need to show documentation to prove their assets and income, good credit, employment verification, among other documentation to be pre-approved for a mortgage.

What do you need to prove that you have funds for the down payment?

The borrower needs bank statements and investment account statements to prove that they have funds for the down payment and closing costs, as well as cash reserves. 2

How do potential buyers benefit from a pre-approval letter?

Potential buyers benefit in several ways by consulting with a lender and obtaining a pre-approval letter. First, they have an opportunity to discuss loan options and budgeting with the lender. Second, the lender will check the buyer's credit and unearth any problems. The homebuyer will also learn the maximum amount they can borrow, which will help set the price range. Using a mortgage calculator is a good resource to budget the costs.

When does a final loan approval occur?

Final loan approval occurs when the buyer has an appraisal done and the loan is applied to a property. 1

Do you need a pre-approval letter for a home?

Shopping for a home may be exciting and fun, but serious homebuyers need to start the process in a lender's office, not at an open house. Most sellers expect buyers to have a pre-approval letter and will be more willing to negotiate with those who prove that they can obtain financing.

Do sellers expect buyers to have pre-approval?

Most sellers expect buyers to have pre-approval letter and will be more willing to negotiate if you do.

Do you need a gift letter for a VA loan?

Veterans Affairs (VA) loans, which require no money down, are for U.S. veterans, service members, and not-remarried spouses. A buyer who receives money from a friend or relative to assist with the down payment may need a gift letter to prove that the funds are not a loan. 6 . 3. Good Credit.

Pre-Qualification vs. Pre-Approval

Requirements For Pre-Approval

- Mortgage pre-approval requires a buyer to complete a mortgage application and provide proof of assets, confirmation of income, good credit, employment verification, and important documentation. Pre-approval is based on the buyer's FICO credit score, debt-to-income ratio (DTI), and other factors, depending on the type of loan. Except for jumbo loans...

Pre-Approval vs. Approval

- A lender is required to provide a document called a loan estimatewithin three business days of receiving a completed mortgage application. It outlines the pre-approved loan amount and maximum loan amount, terms and type of mortgage, interest rate, estimated interest and payments, estimated closing costs, an estimate of property taxes, and homeowner’s insurance. …

What If You Don't Get Pre-Approved?

- After reviewing a mortgage application, a lender will provide a decision to pre-approve, deny, or pre-approve with conditions. These conditions may require the borrower to provide extra documentation or reduce existing debt to meet the lending guidelines. If denied, the lender should explain and offer options to improve a borrower's chances for pre-approval.

The Bottom Line

- Mortgage pre-approval is an examination of a home buyer's finances and lenders require five items to ensure borrowers will repay their loan. Potential borrowers complete a mortgage application and provide proof of assets, confirmation of income, credit report, employment verification, and important documentation to obtain pre-approval.