When to perform tests of controls in an audit?

Tests of control are only performed when the auditor believes that the control risk is low, enabling them to verify this assessment. However, a test of details is almost always required to obtain sufficient audit evidence. Purposes of tests of control. There are several reasons to perform tests of control in auditing.

What are the types of Audit test?

What are The Types of Audit Tests That Professionals Use to Assess Risk

- Types of Audit Tests. There are two main types of audit tests that an auditor carries to understand the internal control of the sales cycle.

- Test of Controls. This process evaluates the company’s internal audit process to prevent or detect risks associated with financial calculations.

- Test of Details. ...

- Final Thoughts. ...

What is a substantive audit test?

Substantive testing is an auditing technique that checks for any errors or material misstatements in a company's accounts, financial statements or supporting documents. When a company claims that their financial records are accurate, complete and valid, substantive testing supports this claim as evidence that there are no errors.

What are the types of audit procedures?

Audit procedures are the specific tests and methods that auditor executes when gathering the evidence which are necessary for making an opinion on the financial statements of the firm. There are three types of audit procedures: data selection, reliability validation, relevance confirmation.

What is test of details example?

Test of Details Examples Vouching invoices. Tracing bills sent to customers. Search for unrecorded liabilities in accounts payable. Testing bank reconciliations by examining subsequent month bank statements.

What is test of controls and test of details?

While a test of controls supports control risk assessment, a test of details is performed to support the overall audit opinion of a company's balance sheet and accompanying transactions. Tests of control are only performed when the auditor believes that the control risk is low, enabling them to verify this assessment.

Why do we do test of details?

The purpose of tests of details is to obtain direct audit evidence to detect material misstatements or non-compliance at the assertion level. Tests of details are mostly applied to selected individual items.

Is test of details the same as substantive testing?

The terms are used interchangeably, but technically, substantive testing procedures include test of details and analytical procedures. Test of details relates to obtaining source documentation and reconciling, tracing, vouching, etc.

How do you create a test of details?

Procedures to Perform Test of DetailsVouching. One of the main ways in which auditors perform tests of details audit procedure is vouching. ... Tracing. While vouching requires auditors to select a transaction and check its source documents, tracing is the other way round. ... Confirmations. ... Examining Contracts. ... Other procedures.

What is a substantive test of details?

Substantive tests of details is an auditing protocol that's necessary when there's a high chance of material misstatement. Its purpose is to verify the auditor's conclusions about the amount of money in accounts and the figures that appear on the client's documents.

Why does an auditor perform tests of details of balances?

Auditors typically choose a sample to test whether the details match the transaction recorded in a company's books. Tests of details of balances. A test of balances is done to check whether any material misstatement exists in the balances of the financial statements' accounts.

What is TOC and TOD in audit?

in toc intention is to check whether systems are created and are they working to protect assertions of TBD. in tod intention is to check directly assertions of transactions, balances & disclosure (TBD)

What are the three types of substantive tests?

The three types of substantive tests are analytical procedures, a test of details of transactions, and tests of details of balances.

What are the two types of substantive procedures?

There are two categories of substantive procedures - analytical procedures and tests of detail. Analytical procedures generally provide less reliable evidence than the tests of detail.

Is recalculation a test of details?

Recalculation procedures can be used as a test of control and a substantive test, and like reperformance, it results in audit evidence obtained directly by the auditor so it's considered to be highly reliable evidence. The procedure can be done manually, but is most often done using CAATs.

What is the difference between Tod and toe?

Test of Design (TOD) – which verifies that a control is designed appropriately and that it will prevent or detect a particular risk. Test of Effectiveness (TOE) – although it's less reliable, it is use for verifying that the control is in place and it operates as it was designed.

What are the types of control test?

What are Tests of Controls?Reperformance Classification. Auditors may initiate a new transaction, to see which controls are used by the client and the effectiveness of those controls.Observation Classification. ... Inspection Classification.

What is TOC and TOD in audit?

in toc intention is to check whether systems are created and are they working to protect assertions of TBD. in tod intention is to check directly assertions of transactions, balances & disclosure (TBD)

How do you perform test of controls?

4 Steps to Build An Effective Internal Control Testing ProgramCreate an Inventory of Controls. ... Prioritize Controls Testing. ... Design an Appropriate Test for Each Control. ... Document and Follow Up on Identified Issues.

What are the two types of audit tests?

These are the five types of testing methods used during audits.Inquiry.Observation.Examination or Inspection of Evidence.Re-performance.Computer Assisted Audit Technique (CAAT)

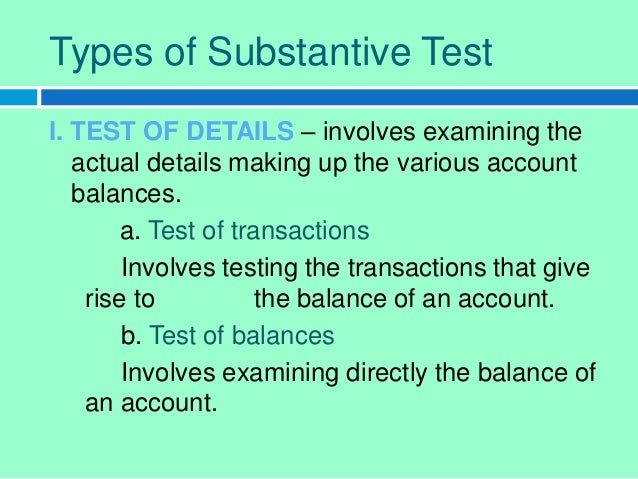

What is the test of details?

Test of details as the name suggests is detailed testing by the auditors for collection of audit evidence that the balances, underlying disclosures, and the transactions associated with the financial statements are correct. In other words, these are the primary responses of an auditor to check for the risk ...

What is the purpose of the test of details of balances?

The test of details of balances is intended to demonstrate that the tests of control and the substantive tests related to transactions are all reasonable. The test of control is an audit test. It is intended to quantify the adequacy of the controls. If, for instance, the test shows that the controls are frail, this will affect the test ...

What is the evidence that an auditor finds reasonable evidence that the receivables figure is understated or over?

If an auditor finds reasonable evidence that the receivables figure is understated or overstated, one of the evidence he can use is the confirmation of receivables balances by the customers themselves. This is a third-party confirmation and is more appropriate than evidence from within the organization.

What is re-perform figuring of legal deductions?

Re-perform figuring of legal deductions to affirm whether the right deductions during the current year have been incorporated inside the total payroll expense.

What is a test of balance?

Test of balances are done to check if any material misstatement exists the balances of the financial statements’ accounts.

What does it mean when an auditor perceives a company to be of higher risk?

If an auditor perceives a company to be of higher risk, he may require more evidence. He may want to audit more information and hence, increasing the test of details to be performed. Figuring out how to coordinate your audit techniques with risks is one of the most significant things an auditor will do.

Why are substantive tests of detail helpful sources of confirmation?

Substantive tests of detail are helpful sources of confirmation when a mix of dependence on controls and systematic techniques despite everything, doesn’t give the degree of affirmations which are thought to be significant, or in circumstances which are not usually where a controls-dependent methodology is either not do able or isn’t viewed as practical.

Test of Details Definition

Test of details is a substantive procedure used by Auditor as a response to the risk assessment performed. These procedures help Auditor to obtain sufficient and appropriate audit evidence that the financial information is free from material misstatements.

Chapter 1: How does Auditor deep dive into details?

The auditor validates these account balances, transactions, or disclosures with supports such as invoices, agreements, or company policy documents.

Chapter 2: How does the Test of details performed?

Auditors design these tests after considering the risk assessment results, underlying account balance tested, nature of risk, and previous year misstatements, if any. So, this testing procedure gives more reasonable assurance

Chapter 3: What are the ways of performing Tests of details?

All the Entries accounted in the books of accounts are verified for accuracy and occurrence with the underlying supports.

Test of details Conclusion

In Conclusion, the Test of details is a method of auditing financial information by digging deep into the details of transactions. To keep it simple, it is the process of obtaining comfort over the recorded transaction by checking with the underlying supports. Vouching, Confirmations and Subsequent receipts are the way to perform Tests of details.

What is audit test?

Audit test is a procedure adopted by an auditor to test a sample of a similar group of transactions to conclude the fairness with which the transactions are recorded. It involves undertaking tests in five ways to arrive at a wholesome picture about the level of effectiveness of internal controls and whether there are any errors, omissions, or any material misstatements while preparing financial statements of the organization.

What is the purpose of audit testing?

The main purpose of audit testing is to check and verify the level of effectiveness of controls followed by an organization while recording its financial transactions. It ensures that it tests and detects any error, omission, or material misstatements in the financial statements. Once an auditor.

What is an auditor?

Auditor An auditor is a professional appointed by an enterprise for an independent analysis of their accounting records and financial statements. An auditor issues a report about the accuracy and reliability of financial statements based on the country's local operating laws. read more.

What is the responsibility of an auditor?

The responsibility of the auditor increases, as he needs to be sure that the sample covers all the aspects of transactions being carried out by the organization, and he leaves no stone unturned to check on any undetected errors or frauds.

What is a BOD in accounting?

Samples are selected randomly, and thus, there is no control by management or board of directors Board Of Directors Board of Directors (BOD) refers to a corporate body comprising a group of elected people who represent the interest of a company’s stockholders. The board forms the top layer of the hierarchy and focuses on ensuring that the company efficiently achieves its goals. read more or accounting staff or any other person. Thus they remain alert and careful while posting financial transactions at each stage.

Why is it important to select a few samples from a large group of transactions?

It helps an auditor to select a few samples from a large group of transactions. Thus, it reduces the volume of work involved. Saves a lot of time; Eventually saves his workforce and labor to be employed. Saves on cost on account of lesser time involved and low workforce associated;

What is the purpose of risk assessment?

Undertaken to identify and understand risks the company entails considering the environment within which it operates.

What is audit test of controls?

Definition: Audit Test of controls is a type of audit examination on the internal control of an entity after they performed an understanding of internal control over financial reporting. Those internal controls mainly related to internal control over financial reporting. Quality of financial statements is significantly depending on internal control ...

What do auditors need to do after reviewing all the samples?

Once auditors complete the reviews all the samples that they are selecting, auditors need to make the conclusion on the internal control based on the result of their testing as well as conclude whether they could place the reliance on the internal control or not.

What are the procedures that use to perform the test of controls?

For example, auditors want to review capital expenditure authorization whether it is implemented based on the delegation that approves by the board of directors or not.

When to perform a test of controls?

Test of control is one of the important approaches that is used by auditors to reduce the workload or reduce the number of sampling that the auditor will select during the substantive test or dest of detail. The decision whether to test the control or not is after the auditor obtains their understanding of the client’s internal control and concludes that they might not be able to test the control.

What happens to the substantive test if the control is not?

But if the control is not, then the substantive test will be increased. The increase might be up to 100% (percent) based on auditors’ judgments.

Why is an auditor required during the planning stage?

So, during the planning stage auditor is required by the standard to obtain an understanding of client internal control over financial reporting. And then assess those control whether they are reliable or not.

What is the procedure used to perform the test of controls over financial reporting?

This kind of procedure is called inspection. So, the procedures that use to perform the test of controls over financial reporting are depending on the control that auditors want to review. The following are the procedures that normally use: