What is the maximum debt to income ratio for FHA?

FHA loans are mortgages backed by the U.S. Federal Housing Administration. FHA loans have more lenient credit score requirements. The maximum DTI for FHA loans is 57%, although it's decided on a case-by-case basis.

What is the qualifying ratio for FHA loans?

How much can that ratio be? According to the FHA official site, "The FHA allows you to use 31% of your income towards housing costs and 43% towards housing expenses and other long-term debt." Those percentages should be examined side-by-side with the debt-to-income requirements of a conventional home loan.

What are the two ratios used for FHA loans?

Lenders use a ratio called "debt to income" to determine the most you can pay monthly after your other monthly debts are paid. For the most part, underwriting for conventional loans needs a qualifying ratio of 33/45. FHA loans are less strict, requiring a 31/43 ratio.

What is the maximum debt to income ratio for buying a house?

As a general guideline, 43% is the highest DTI ratio a borrower can have and still get qualified for a mortgage. Ideally, lenders prefer a debt-to-income ratio lower than 36%, with no more than 28% of that debt going towards servicing a mortgage or rent payment.

Can you be denied an FHA loan?

There are three popular reasons you have been denied for an FHA loan–bad credit, high debt-to-income ratio, and overall insufficient money to cover the down payment and closing costs.

Does FHA use gross or net income?

It uses the adjusted gross income indicated on line 7 of IRS's new Form 1040. The Department of Housing and Urban Development, which sets FHA guidelines, defines gross income as the annual amount earned by the borrowers who will be responsible for the loan.

How can I lower my debt-to-income ratio?

How to lower your debt-to-income ratioIncrease the amount you pay monthly toward your debt. Extra payments can help lower your overall debt more quickly.Avoid taking on more debt. ... Postpone large purchases so you're using less credit. ... Recalculate your debt-to-income ratio monthly to see if you're making progress.

Do lenders look at front end DTI?

Lenders usually prefer a front-end DTI of no more than 28%. 1 In reality, depending on your credit score, savings, and down payment, lenders may accept higher ratios, although it depends on the type of mortgage loan.

Does FHA count 401k loans in DTI?

The FHA doesn't count any loan payments taken against retirement funds. So, for example, borrowing from your 401(k) for a down payment isn't included in the DTI calculation; however, your total assets will be lower. Always discuss borrowing from your retirement funds with your financial advisor first.

What is not included in debt-to-income ratio?

What payments should not be included in debt-to-income ratio? The following payments should not be included: Monthly utilities, like water, garbage, electricity or gas bills. Car Insurance expenses.

What is the average American debt-to-income ratio?

The St. Louis Federal Reserve tracks the nation's household debt payments as a percentage of household income. The most recent number, from the first quarter of 2022, is 9.5%. That means the average American spends more than 9% of their monthly income on debt payments.

What is acceptable debt-to-income ratio?

What do lenders consider a good debt-to-income ratio? A general rule of thumb is to keep your overall debt-to-income ratio at or below 43%.

What are the qualifying ratios for FHA loans quizlet?

FHA allows a maximum debt-to-income ratio of 43% so $1,033.30 / 0.43 = $2,403.02, the minimum monthly income needed. Remember, though, a borrower must qualify under both ratios so $2,582.74 is the minimum monthly income Mary would need to buy this home ($800.65 / 0.31).

What is included in debt-to-income ratio?

To calculate your debt-to-income ratio, add up all of your monthly debts – rent or mortgage payments, student loans, personal loans, auto loans, credit card payments, child support, alimony, etc. – and divide the sum by your monthly income.

What are the FHA underwriting guidelines?

FHA Loan RequirementsFICO® score at least 580 = 3.5% down payment.FICO® score between 500 and 579 = 10% down payment.MIP (Mortgage Insurance Premium ) is required.Debt-to-Income Ratio < 43%.The home must be the borrower's primary residence.Borrower must have steady income and proof of employment.

What is housing ratio formula?

To calculate the housing expense ratio, simply take the sum of all property expenses and divide it by a pretax income.

What Income Is Used to Calculate Debt to Income Ratio?

Debt to income ratios may be calculated using the following forms of income:

What Monthly Debt Is Used to Calculate Debt to Income Ratio?

Back-end DTI includes all your minimum required monthly debts; including the anticipated mortgage payment.

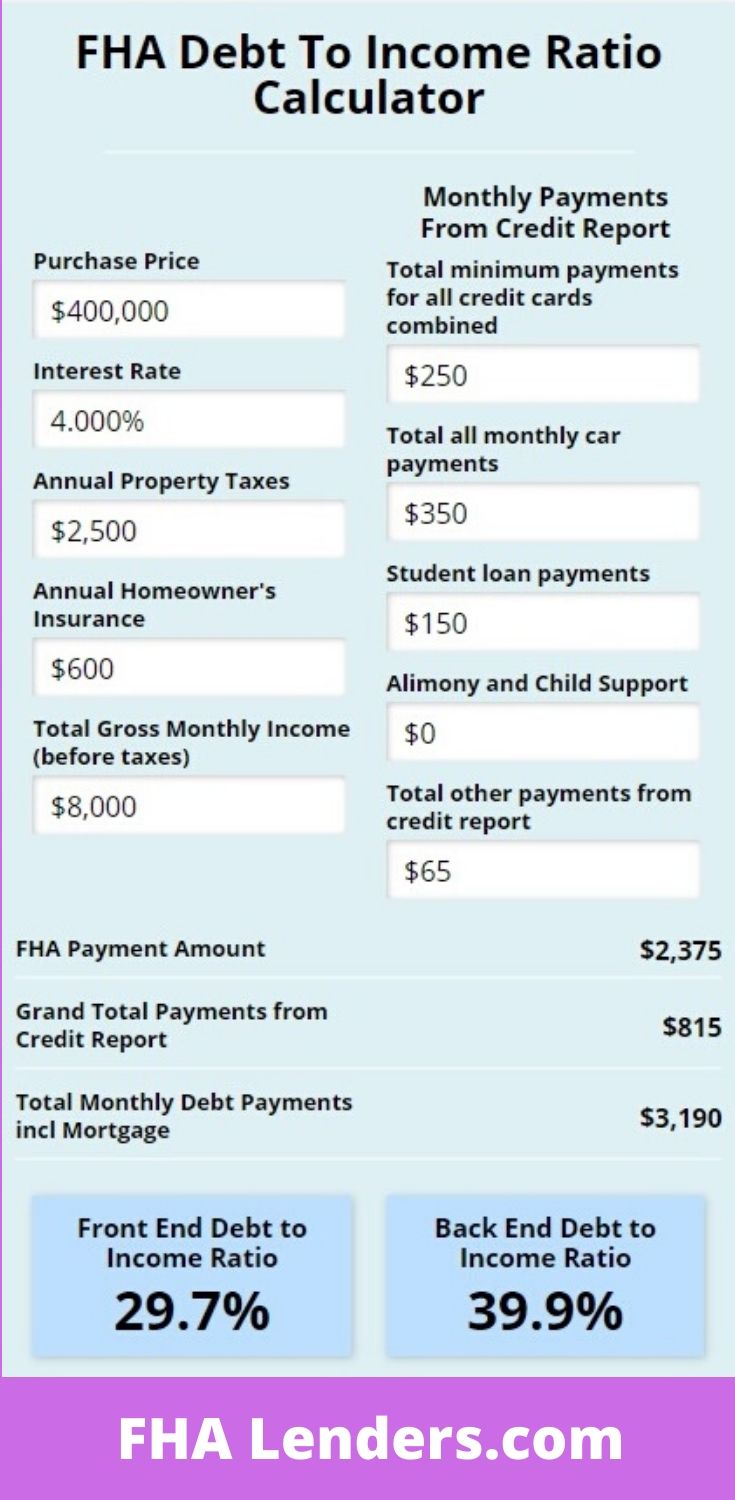

FHA Front End Debt to Income Ratio Calculation

The front end debt-to-income ratio is a calculation that takes the monthly gross income divided by the mortgage payment, including taxes, insurance, mortgage insurance fee, and any other expense paid monthly. According to the guidelines of the Federal Housing Administration (FHA), the maximum front end ratio can be up to 40% depending on the borrower's credit history..

FHA Back End Debt to Income Ratio Calculation

The Federal Housing Administration (FHA) takes into account all of the payments that you make on a monthly basis, such as credit card, student loan, and car payments. Besides these, other factors such as Social Security, taxes, and child support are also taken into account to arrive at a total debt-to-income ratio.

FHA Debt to Income Ratio Compensating Factors

In order to minimize the risk of getting stuck with higher DTI levels, the Federal Housing Administration (FHA) allows lenders to increase the DTI ratios for certain borrowers if they can meet certain compensation factors. These include meeting certain income and credit requirements.

What is the maximum FHA DTI ratio allowed?

The maximum DTI ratio that can be allowed by participating lenders under the Federal Housing Administration's (FHA) program is 56.9%. This is based on the various factors that help minimize the risk that the lender faces.

Best Way to Lower Your Debt to Income Ratio

There are many ways to lower your DTI, and the most obvious one is to increase your monthly income. However, there are also other strategies that can help lower your debt.

What is the FHA debt ratio?

To recap, FHA's maximum qualifying debt ratios for borrowers in 2019 are 31% and 43%. This means the monthly housing payments should not exceed 31% of gross monthly income, while the total debt burden should not exceed 43% of monthly income. But there are exceptions to these rules, as noted above. Disclaimer: HUD makes changes to their FHA ...

Who sets the FHA debt to income ratio?

The Department of Housing and Urban Development (HUD) has specific guidelines for FHA debt-to-income ratios. HUD is the government entity that establishes all of the rules and requirements for the FHA loan program, including the DTI limits.

What is the DTI for FHA loans?

2018 DTI Limits for FHA Loans: 31% / 43%. According to official FHA guidelines, borrowers are generally limited to having debt ratios of 31% on the front end, and 43% on the back end. But the back-end ratio can be as high as 50% for certain borrowers, particularly those with good credit and other "compensating factors.".

How long do you have to have cash reserves to get a mortgage?

In this context, "substantial" typically means that the borrower has at least one to three months worth of mortgage payments in the bank after closing. The exact requirement can vary depending on the loan parameters.

What does it mean when you apply for an FHA loan?

When you submit an application for an FHA-insured home loan, the mortgage lender will evaluate your debt-to-income ratio to see if you're qualified for a loan. If you have too much debt in relation to your monthly income, you might have trouble qualifying. On the other hand, if you have a manageable level of debt (as defined below), you have one less thing to worry about.

What is the FHA debt to income ratio for 2021?

The current (2021) limits for FHA debt-to-income ratios are 31% for housing-related debt, and 43% for total debt. But there are exceptions to these general rules. So don't be discouraged if you're slightly above those numbers.

What is residual income?

Residual income: The term "residual income" refers to money that's left over each month after all of your major expenses are paid (including housing, taxes, and debt payments).

What is the FHA debt ratio?

Being in line with FHA course of action, the loan borrowers can are limited to have the debt ratios of 31% when it comes to “front-end” ratio, and 43% for the “back-end” one.

What is the FHA debt qualifying ratio?

Accordingly, no matter what, the max. FHA debt qualifying ratio for all borrowers needs to be 31% and 43%. What we are trying to explain is that your once-a-month housing payments must not go beyond 31% of the gross monthly income and the overall debt burden must not be higher than 43% of the monthly income.

What is the FHA DTI?

An FHA Debt-to-Income (DTI) ratio is the percentage of the income of somebody that is used with an intention to cover his or her recurring debts. This is required when you are lent a loan by a loan lender. The loan lender sees if you are satisfying all of the criteria of the FHA DTI ratio or not.

What is back end ratio?

The back-end ratio is executed on the basis of all recurring monthly debts into account. So, whether it is your car loan, mortgage fee, or credit card, home insurance, HOA fee, student loan, everything will be taken into account for the calculation of this ratio.

What is the back end ratio for a mortgage?

Note: The basic rule is that your back-end ratio needs to be less than 43% or a reduced amount of it because if it is higher, I’m afraid that you won’t be able to qualify for the loan.

What is residual income?

It is the money that is available once all of the major expenses are paid, including debt payments, housing taxes, and others.

What is the rule of thumb when it comes to personal finance?

When it comes to personal finance, the rule of thumb is that you get to earn more than you have to spend. It is as simple as that. However, this is what you think, not the mortgage lender.

What Are Debt To Income Ratio?

Debt To Income Ratio is the ratio of your total monthly debt payments which includes your proposed new housing payment and dividing it by your monthly gross income. Debt to income ratios is how a mortgage lender determines whether or not you qualify for a particular loan program. Debt to income ratios also determines whether you can afford your new monthly mortgage payments along with all of your other monthly payments under the eyes of the lender. Borrowers should carefully evaluate their monthly debts and see how much house they can afford. When mortgage underwriters are determining debt to income ratios, they do not take into account the borrower’s personal debts that do not report to the credit bureaus. Debts like educational expenses, entertainment, utilities, child care, elderly care, and other personal expenses are not included when a mortgage underwriter is calculating the debt to income ratios of a borrower.

What is the front end debt to income ratio?

However, many lenders may have a front end debt to income ratio requirement of 31% DTI as part of their lender overlays if the borrower’s credit scores are under 620 FICO. The front end debt to ratio requirement is not an FHA Guidelines BUT an FHA Lender Overlay imposed by individual mortgage lenders.

What is the DTI for FHA?

This holds true even though FHA allows debt to income ratios up to 56.9% DTI for borrowers with credit scores of at least 620 or higher.

What is the maximum DTI for a 680 credit score?

Some lenders will cap DTI at 45% up to a 680 credit score and may cap DTI to 55% over 680 Credit Scores. Again, it is up to a mortgage lender to set their own debt to income ratio requirements and it can be higher requirements than those of FHA.

What is the down payment for a 580 loan?

However, anyone with under a 580 credit score needs a 10% down payment. If the borrower has credit scores under 620 credit scores, the borrower cannot have a debt to income ratio of greater than 43% DTI to get an approve/eligible per automated underwriting system (AUS)

What are not included in mortgage underwriting?

Debts like educational expenses, entertainment, utilities, child care, elderly care, and other personal expenses are not included when a mortgage underwriter is calculating debt to income ratios of a borrower. Debt to income ratio is one of the most important factors in the mortgage qualification process.

Do FHA loans have HUD overlays?

Lenders will require all borrowers meet the minimum HUD agency mortgage guidelines on FHA loans. Most Lenders will have Lender Overlays on debt to income ratios, which we will discuss on this blog. Lender overlays are additional lending requirements that is above and beyond the minimum HUD Agency Guidelines.

What is the minimum credit score for a mortgage in 2021?

June 29, 2021 - On paper, FHA loan minimums for credit scores start at 580 for the lowest down payment. Its true that the lender may require a higher score, but for FHA mortgages, 580 is the bare minimum FICO score you can have and still be considered for maximum financing.

What type of mortgage is used by first time home buyers?

The FHA Loan is the type of mortgage most commonly used by first time home buyers and there's plenty of good reasons why.

Is FHA a government agency?

FHA.com is a privately owned website, is not a government agency, and does not make loans.

Is the FHA loan good for first time homebuyers?

November 18, 2021 - FH A home loans aren’t restricted to first-time homebuyers, but the FHA mortgage program is a good option for those who have never owned a home before--there is a low down payment requirement and more flexible FICO score guidelines for FHA mortgages.

Does PMI go away on FHA?

Due to the 1989 Homeowners Protection Act, lenders have to cancel a conventional PMI when they reach a loan-to-value ratio of 78%. Many home buyers opt for a conventional loan because the PMI declines until the FHA MIP disappears on its own – unless you defer 10% or more. On the same subject : FHA Mortgages.

What are the two ratios used for FHA loans?

How big can that relationship be? According to the FHA’s official website, “FHA allows you to use 31% of your income for housing costs and 43% for housing costs and other long-term debts.

How can I lower my debt-to-income ratio for a mortgage?

Increase the amount you pay monthly according to your debt. Additional payments can help reduce total debt faster.

What is the average American debt-to-income ratio?

1. In 2020, the average debt repayments of Americans accounted for 8.69% of their income. To put this into perspective, the average American spends nearly 9% of their monthly income on debt repayment, down from 9.69% in Q2 2019.

What Is A Good Debt-To-Income Ratio To Get A Mortgage?

The lower your DTI, the better. In most cases, you’ll need a DTI of 50% or less, but the specific requirement depends on the type of mortgage you’re applying for.

What is the maximum DTI for FHA loans?

Federal Housing Administration. FHA loans have more lenient credit score requirements. The maximum DTI for FHA loans is 57%, although it’s lower in some cases.

How Can I Lower My Debt-To-Income Ratio?

If your DTI is high , there are some strategies you can use to lower it before you apply for a mortgage.

What is a DTI of 50%?

Your DTI helps lenders gauge how risky you’ll be as a borrower. A DTI of 50% or less will give you the most options when you’re trying to qualify for a mortgage. You can use Rocket Mortgage ® to see what purchase options you're eligible for based on your DTI, credit and other factors.

What is the DTI for a conventional loan?

However, you’ll generally need a DTI of 50% or less to qualify for a conventional loan.

What is a good DTI for a mortgage?

A DTI of 50% or less will give you the most options when you’re trying to qualify for a mortgage. You can use Rocket Mortgage ® to see what purchase options you're eligible for based on your DTI, credit and other factors.

How to find the DTI percentage?

The resulting quotient will be a decimal. To see your DTI percentage, multiply that by 100.In this example, let’s say that your monthly gross household income is $3,000. Divide $900 by $3,000 to get .30, then multiply that by 100 to get 30. This means your DTI is 30%.