What is Hamp’s history?

Knowing a little about what is HAMP’s history will help you understand some of the financial aspects of the program. Home Affordable Modification Program ( HAMP) was a division within the Making Home Affordable Program (MHA), which was set up by the Treasury Department and the Department of Housing and Urban Development in 2009.

What is'home affordable modification program (Hamp)'?

What is 'Home Affordable Modification Program (HAMP)'. The Home Affordable Modification Program (HAMP) was a federal government loan modification program introduced in 2009 to help struggling homeowners avoid foreclosure.

When did the Home Affordable modification program end?

The program expired at the end of 2016. The Home Affordable Modification Program (HAMP) was a federal program introduced in 2009 to help struggling homeowners avoid foreclosure. The HAMP allowed homeowners to reduce their mortgage principal and/or interest rates, temporarily postpone payments, or get loan extensions.

What is the FHA-HAMP program?

FHA-Home Affordable Modification Program (FHA-HAMP) Allows homeowners to modify their FHA-insured mortgages to reduce monthly mortgage payments and avoid foreclosure. Nature of Program: FHA-HAMP allows the use of a partial claim up to 30 percent of the unpaid principal balance as of the date of default combined with a loan modification. To...

When did HAMP program end?

2016The Home Affordable Modification Program (HAMP), created in 2009 by the federal government, made it possible for struggling homeowners to stay afloat by modifying the original terms of their mortgage loans. The program ended in 2016, but other mortgage modifications programs have cropped up.

What replaced the HAMP program?

Fannie Mae and Freddie Mac announced on Wednesday their replacement for the Home Affordable Modification Program.

When did loan modification start?

1930sLoan modifications have been practiced in the United States since the 1930s. During the Great Depression, loan modification programs took place at the state level in an effort to reduce levels of loan foreclosures.

What is the FHA HAMP program?

Allows homeowners to modify their FHA-insured mortgages to reduce monthly mortgage payments and avoid foreclosure. Nature of Program: FHA-HAMP allows the use of a partial claim up to 30 percent of the unpaid principal balance as of the date of default combined with a loan modification.

Can you refinance after a HAMP modification?

It's not theoretically impossible to refinance under HARP after a HAMP modification. However, it may depend upon the terms of the modification, such as whether or not the loan modification included principal forgiveness or deferment, and other factors.

Is HAMP expired?

The Home Affordable Modification Program (HAMP) was a loan modification program introduced in 2009 to help mitigate the impact of the 2008 subprime mortgage crisis. It expired in 2016.

Do you have to pay back a loan modification?

If your modification is temporary, you'll likely need to return to the original terms of your mortgage and repay the amount that was deferred before you can qualify for a new purchase or refinance loan.

How long does a loan modification stay on your credit report?

seven yearsMost other negative information, including foreclosures, short sales, and loan modifications (if they're reported negatively), will remain on your credit report for seven years.

What is the disadvantage of loan modification?

Some loan modifications are a debt settlement, and it can affect your credit depending on your the type of program in which you enroll. Debt settlement will hurt your credit score, even if there is an agreement with the lender.

What happens after HAMP trial period?

It is simply a test of your ability to make the payments. Once you have completed this trial period successfully, they will create and offer you a permanent loan modification. Once The Trial Payment Plan Payments Are Made, The Lender Will Send You A Permanent Loan Modification On Their Own Accord.

What is HARP mortgage program?

HARP is short for the Home Affordable Refinance Program, and it was created to help homeowners refinance underwater home loans after the 2008 housing crisis. A loan is considered underwater or “upside-down” when the balance is larger than the home's value.

What is a HUD loan modification?

A loan modification is a restructuring of your mortgage in which you and your lender agree to modify the terms of your home loan. In a loan modification, your lender may defer some of your payments, change your interest rate, extend the length the loan, or forgive or cancel a portion of the mortgage debt.

What is the Home Flex modification program?

The Flex Modification program helps borrowers who have a Fannie Mae- or Freddie Mac-owned loan. This program, which replaces the now-expired Home Affordable Modification Program (HAMP) program, is supposed to reduce an eligible borrower's mortgage payment by about 20%.

What is the disadvantage of loan modification?

One potential downside to a loan modification: It may be added to your credit report and could negatively impact your credit score. The resulting credit dip won't be nearly as negative as a foreclosure but could affect your ability to qualify for other loans for a time.

Why was the HAMP program created?

HAMP was created under the Troubled Asset Relief Program ( TARP) in response to the subprime mortgage crisis of 2008. During this period, many American homeowners found themselves unable to sell or refinance their homes after the market crashed because of tighter credit markets. Monthly payments became unaffordable when higher market rates kicked in ...

What Is the Home Affordable Modification Program (HAMP)?

The Home Affordable Modification Program (HAMP) was a loan modification program introduced by the federal government in 2009 to help struggling homeowners avoid foreclosure. The program's focus was to help homeowners who paid more than 31% of their gross income toward mortgage payments. The program expired at the end of 2016.

What was the most significant contribution of HAMP?

Although taxpayers subsidized some of the loan modifications, arguably the most significant contribution of HAMP was standardizing what had been a haphazard loan modification system. In order to qualify, mortgagors needed to make more than 31% of their gross income on their monthly payments.

When is the deadline for HARP?

The deadline for HARP was originally intended for Dec. 31, 2017.

When does the HARP expire?

The deadline for HARP was originally intended for Dec. 31, 2017. However, that date was extended, pushing the program's expiration date to December 2018.

Can you modify a HAMP loan?

In many cases, an already modified loan was eligible for HAMP modification, too, reducing a homeowner’s payment even further.

When did the HAMP loan program expire?

This program expired on December 31, 2016.

What is a HAMP?

The Home Affordable Modification Program (HAMP) is a government program introduced in 2009 to respond to the subprime mortgage crisis. HAMP is part of the Making Home Affordable program (MHA), established in concert with the Hardest Hit Fund program (HHF) under the Troubled Asset Relief Program ...

When does HAMP end?

HAMP (and the entire MHA Program) is set to expire December 31, 2016, the last day to submit applications, and the Modification Effective Date must be on or before September 30, 2017. HHF has been extended to 2020.

When did the Greenlining program end?

Sunset of the program. At the Greenlining Institute 22nd Annual Economic Summit on May 8th, 2015 Mel Watt announced that the program would cease end of year 2016. The Director of the FHFA had this to say regarding the program:

When was the MHA program launched?

The Making Home Affordable program of the United States Treasury was launched in 2009 as part of the Troubled Asset Relief Program. The main activity under MHA is the Home Affordable Modification Program.

What is the MHA Handbook?

The MHA Handbook is a consolidated reference guide outlining the requirements and guidelines for the Making Home Affordable (MHA) Program and particularly HAMP , its most popular component. A complex calculation called the net present value (NPV) test is the foundation of the HAMP program. Tier 1 and Tier 2 have their own NPV test. The NPV test predicates modification on whether the investor will make more money by modifying the mortgage rather than foreclosing.

When did the HAMP program end?

HAMP expired on December 31, 2016. It wasn’t entirely a surprise. The Director of the Federal Housing and Finance Agency (FHFA) had announced in May of 2015 that there would be no more extensions to the program.

What is a HAMP?

Knowing a little about what is HAMP’s history will help you understand some of the financial aspects of the program. Home Affordable Modification Program ( HAMP) was a division within the Making Home Affordable Program (MHA), which was set up by the Treasury Department and the Department of Housing and Urban Development in 2009.

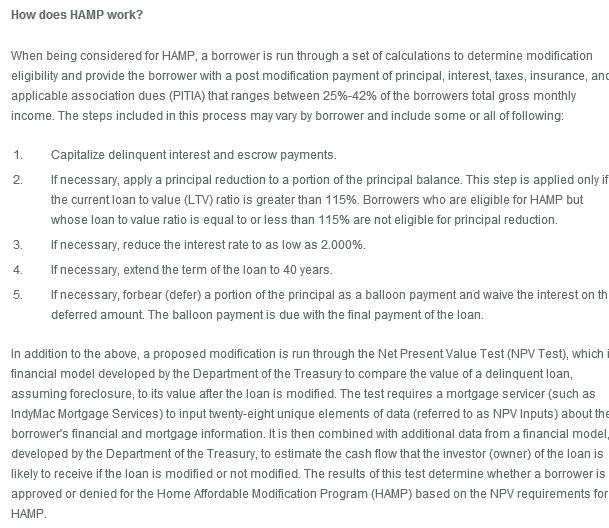

How does HAMP work?

HAMP worked with mortgage lenders by providing incentives to banks that reduced the debt-to-income ratios of home loans to less than 38%. The Department of Treasury then entered the equation to minimize the DTI ratio to less than 31% through payments of $1,000 for each modification mortgage servicers made and $1,000 for lenders each year for three years.

How long is a HAMP trial?

If a lender approved the application for HAMP, the borrower was often placed on a three-month trial plan. If payments were made promptly, then usually the mortgage company made an official modification agreement, lowering your mortgage payments through one of the above-mentioned manners.

When was the Affordable Modification Program revised?

Although the initial Home Affordable Modification Program was restricted to primary residences, in 2012, it was revised to include rental properties. Households with multiple mortgages and homeowners with a DTI that was higher or lower than 31% also became eligible.

Does HAMP help homeowners?

Although HAMP helped so many homeowners, it wasn’t an automatic get-out-of-debt-free card. Some homeowners ended up defaulting again or losing their homes in foreclosure. Still, others now have a more extended loan period with more interest accruing over the life-time of the loan.

Can you still apply for HAMP loan modification?

Even though HAMP is no longer available, homeowners in need can still apply for loan modification programs through their lender or mortgage servicer. These options can mean the difference between losing your home to foreclosure or finding a way to get through times of economic hardship with a roof over your head.

When was HAMP introduced?

Introduced in 2009, HAMP was specifically meant for those paying more than 31% of their gross income toward a mortgage. The program could extend loans, slash mortgage principal or interest and temporarily postpone payments.

Why did the HAMP program happen?

HAMP came about after the 2008 subprime mortgage crisis and recession. It was a part of the Troubled Asset Relief Program, a federal program meant to purchase difficult assets and equity from financial institutions. At the time, many homeowners found themselves in a bind because buying and selling homes became hard after credit standards tightened.

What is HAMP loan?

Before it expired in 2016, the Home Affordable Modification Program (HAMP) was a federal loan modification program designed to assist homeowners struggling with potential foreclosure.

Is HAMP no longer available?

Now that HAMP is no more, what options are available to the struggling U.S. homeowner? You still have choices, and we’ve collected a list of our top picks — and when you’re finished, don’t forget to read our mortgage guide.

What is the Home Affordable Modification Program (HAMP) ?

What is the Home Affordable Modification Program (HAMP) ? HAMP is a program (actually, half a program) developed by the Obama Administration as an attempted response to the foreclosure crisis in America.

How Does the Home Affordable Modification Program (HAMP) Work ?

How Does the Home Affordable Modification Program (HAMP) Work ? Your mortgage company is supposed to figure out whether it would do better economically to foreclose on you thant to give you any sort of slack. This is done by what is called the NPV test. NPV stands for Net Present Value.

What is a Trial Plan ?

What is a Trial Plan ? The original idea was that they get your information, put you on a "trial plan" if the number seem to favor a HAMP modification, and have you make that payment for up to three months, during which they can verify your information and their property value.

So If It Doesn't Reduce Principal at All, Why Do It ?

So If It Doesn't Reduce Principal at All, Why Do It ? Once consumers understand how this thing works, most say they are not interested, particulary if their mortgage is significantly more than their home is worth.

Why Do I Hear People Say that in HAMP Principal Gets Reduced ?

Why Do I Hear People Say that in HAMP Principal Gets Reduced ? This is an area of major misunderstanding. There is a three step process that gets applied to your mortgage debt if you appear to qualify for HAMP, in order to get the payment down to no more than 31% of your total household income. The third of these is called "principal forbearance".

What is HAFA ?

What is HAFA ? Recently the Federal Government added a new set of programs as part of HAMP called Home Affordable Foreclosure Alternatives (HAFA). The purpose of this was to try to get the mortgage companies to be more cooperative when borrowers ask them to approve a short sale or a deed in lieu of foreclosure.

Serious Legal Advice is Critical

Serious Legal Advice is Critical No matter what you are considering doing, it is impossible to navigate through the chaos alone. What's more, there are so many scams preying upon people's homes, promising them mortgage relief.

How much of the unpaid principal is used in a HAMP loan?

Nature of Program: FHA-HAMP allows the use of a partial claim up to 30 percent of the unpaid principal balance as of the date of default combined with a loan modification.

Can a mortgagor be FHA HAMP?

The Mortgagee must service the mortgage during the trial period in the same manner as it would service a mortgage in forbearance. If the mortgagor does not successfully complete the trial payment plan by making the three payments on time, the mortgagor is no longer eligible for FHA-HAMP.

What is a HAMP modification?

For HAMP modifications that include a PRA principal reduction, the unpaid principal balance of the modified loan is divided into an interest-bearing principal amount and a non-interest-bearing PRA Forbearance Amount. If the homeowner then achieves a payment history that is sufficiently timely over a three-year period, the entire PRA Forbearance Amount is eventually reduced to zero.

What is a HAMP loan?

Departments of the Treasury and of Housing and Urban Development established the Home Affordable Modification Program SM (HAMP SM) for mortgage loans that are not owned or guaranteed by Fannie Mae or Freddie Mac.#N#Under HAMP, a participating loan servicer must consider a sequence of modification steps for each eligible homeowner’s mortgage loan until the loan’s monthly payment is reduced to 31 percent of the homeowner’s verified monthly gross (pre-tax) income. Sometimes, a change in the mortgage loan’s interest rate is sufficient to reach the 31–percent target. Sometimes additional modification steps of term extension or forbearance are necessary as well. See the Home Affordable Modification Program (HAMP) page on the MakingHomeAffordable.gov website.#N#(For mortgage loans that are owned or guaranteed by Fannie Mae or Freddie Mac, eligible homeowners may be offered modifications under related programs also called “HAMP.” Because these related programs do not contain the principal reduction provision that these FAQs address, these FAQs use the term “HAMP” to refer only to the program for mortgage loans that are not owned or guaranteed by Fannie Mae or Freddie Mac.)

The Expiration of HAMP: What Options do Homeowners Have Now?

For years, the Home Affordable Modification Program (HAMP) provided a potential for relief for struggling homeowners to cure a default and to prevent the foreclosure of their home by their mortgage lender.

Homeowners Can Still Seek Assistance From the Government

While we said goodbye to HAMP along with 2016, not every government-facilitated mortgage modification program came to a close. The following is some information on two federal modification programs of interest:

Discuss Your Mortgage Modification Options with a Highly Experienced New York Foreclosure Defense Attorney

There continue to be many different options for homeowners to obtain a modification of their mortgage loan even after the expiration of HAMP. In addition, if you do not qualify for a loan modification, there may be other negotiable solutions to avoid losing your home to foreclosure, including filing for bankruptcy or a potential short sale.

When did the HAMP program end?

The HAMP program ended in 2016. Learn what options are generally available to homeowners now facing a foreclosure.

Who is replacing HAMP?

Fannie and Freddie Mac loans. To replace HAMP, Fannie Mae and Freddie Mac, the government-supported enterprises that own or back many mortgages, developed the Flex Modification program.

What are the two levels of HAMP?

The two levels or "tiers" under HAMP were: Tier 1 and Tier 2. Unfortunately, the HAMP program stopped accepting applications as of December 31, 2016. Still, if you want to learn the difference between Tier 1 and Tier 2, how HAMP worked—and some of the programs that are currently available to help homeowners—read on.

What is a tier 1 HAMP?

HAMP Tier 1. HAMP Tier 1 was a basic HAMP modification. Under Tier 1, a homeowner's monthly mortgage payment, including principal, interest, taxes, insurance, and association fees, was reduced through a series of successive steps (called a "waterfall") so that it equaled 31% of the homeowner's gross monthly income.

What Is The Home Affordable Modification Program (HAMP)?

Understanding The Home Affordable Modification Program

- HAMP was created under the Troubled Asset Relief Program (TARP) in response to the subprime mortgage crisis of 2008.2During this period, many American homeowners found themselves unable to sell or refinance their homes after the market crashed because of tighter credit markets. Monthly payments became unaffordable when higher market rates kicked in on adjustable-rate …

Special Considerations

- The government refers to the ratio of payments to gross income as the front-end debt-to-income ratio (DTI). The HAMP program, working in conjunction with mortgage lenders, helped provide incentives for banks to reduce the debt-to-income ratio to less than or equal to 38%. The Treasury would then step in to minimize the DTI ratio to 31% or less.8 HAMP incentivized private lenders …

The Home Affordable Modification Program

- HAMP was complemented by another initiative called the Home Affordable Refinance Program(HARP). Like HAMP, HARP was offered by the federal government. But there were a subtle few differences. While HAMP helped people who were on the verge of foreclosure, homeowners needed to be underwater or close to that point to qualify for HARP. The program al…

History of Hamp

Priorities of Hamp

The Home Affordable Modification Program (HAMP) is a government program introduced in 2009 to respond to the subprime mortgage crisis. HAMP is part of the Making Home Affordable program (MHA), established in concert with the Hardest Hit Fund program (HHF) under the Troubled Asset Relief Program (TARP), a part of the Emergency Economic Stabilization Act of 2008. HHF provides targeted aid to home owners in states hit hardest by the economic crisis a…

Application Process

Benefits of Hamp

Closing of Hamp